According to Intent Market Research, the Space Militarization Market is expected to grow from USD 48.5 billion in 2023-e at a CAGR of 6.7% to touch USD 77.7 billion by 2030. The space militarization market is competitive, the prominent players in the global market include Airbus, BAE Systems, Boeing, CASC, General Dynamics, L3Harris, Lockheed Martin, Northrop Grumman, Raytheon, and Thales.

As per Intent Market Research, the Space Militarization Market was valued at USD 48.5 billion in 2023-e and will surpass USD 77.7 billion by 2030; growing at a CAGR of 6.7% during 2024 - 2030.

Technological advancements in space-based military systems and a growing need to defend national security from space-based threats drive the market growth. The rise in commercial space ventures and increasing focus on space situational awareness are anticipated to provide significant growth opportunities for the space militarization market.

Space Militarization Market Overview

Space militarization involves the development of weaponry and military technology for offensive and defensive capabilities from existing and future space-based threats. The countries increasingly rely on satellite technology for national security and to carry out military operations. Key countries are actively investing in space militarization technologies to establish global space dominance and thereby there are significant growth opportunities in the space militarization market.

Space militarization has become one of the major operational & national security applications in recent years. The defense budget spending on space militarization has been growing at a significant pace. For instance, the 2024 budget request from the US government allocated nearly USD 3 billion for 15 launch vehicles and range upgrades, along with USD 4.7 billion for protected and jam-resistant satellite communications. There has been an increasing concern about growing space-faring arsenals and rising geopolitical tensions among the countries in recent years. These factors are leading to an imperative need to defend national security from space-based threats, thereby driving the space militarization market growth.

Segment Analysis

Increasing Investment in Intelligence, Surveillance, and Reconnaissance Capabilities is Driving the Market Growth

Countries are increasingly utilizing satellite technology in advanced weapons systems aboard aircraft and warships to carry out precision-strike capabilities. In addition, infrared satellites provide key intelligence systems used as part of the early warning system to track and detect nuclear warheads and other threats to national security. In recent years, owing to the rise in space-based threats, there’s an increasing need for investments in intelligence, surveillance, and reconnaissance capabilities.

For instance, the US budget request for FY 2024 includes nearly USD 5 billion for missile warning and missile tracking, including USD 2.3 billion for new proliferated resilient architectures, and USD 2.6 billion for next-generation overhead persistent infrared. Thus, increasing investment in intelligence, surveillance, and reconnaissance capabilities is driving the market growth.

Source: Intent Market Research Analysis

Growing Need for Anti-Satellite Systems is Driving the Market Growth

The recent rise in reconnaissance satellites and intelligence satellites also referred to as spy satellites for military or intelligence applications is driving the demand for anti-satellite systems. Anti-satellite systems are capable to neutralize or destroy such satellite networks and have been tested in recent years to provide a deterrent against military action. Currently, only a limited number of countries including the US, Russia, China, and India possess the capability for anti-satellite systems. Although anti-satellite systems have not been used in warfare, there’s an increasing demand for anti-satellite system capabilities for national security purposes. Owing to this, several other countries are actively investing in the development of anti-satellite system capabilities.

North America Accounted for the Major Share in Space Militarization Market

The US is a leading country in defense expenditure, with a Department of Defense (DoD) budget for the fiscal year 2023 accounting for over USD 816.7 billion. The US also has an established Space Force since December 2019. For FY2024, the US Space Force requested a budget of USD 30 billion, an increase of about USD 3.9 billion in FY2023. In November 2023, the US Space Force announced that it aims to boost its National Security Space Launch (NSSL) program from 12 launches in 2023 to 21 missions in 2024, with United Launch Alliance (ULA) responsible for 11 missions and SpaceX handling 10. Thus, North America holds the largest market share in space militarization owing to the high government spending on the defense industry.

Competitive Analysis

The Space Militarization Market is Highly Competitive with the Presence of a High Number of Players

Companies operating within the space militarization market are primarily aerospace and defense equipment and infrastructure developers. Companies in the space militarization market often sign long-term contracts with government bodies across the world. The companies are actively expanding their product portfolios with the growing aerospace and defense industry. The space militarization market is dominated by a few key global market players having a significant market share. The market is also highly competitive with an increasing number of local and regional players entering into the market. The key companies in the market are Airbus, BAE Systems, Boeing, CASC, General Dynamics, L3Harris, Lockheed Martin, Northrop Grumman, Raytheon, and Thales, among others.

Following are some key developments in the space militarization market:

- In November 2022, the US Space Force announced that it ordered three GPS 3F satellites from Lockheed Martin for USD 744 million.

- In November 2022, the US Space Force announced that it ordered three GPS 3F satellites from Lockheed Martin for USD 744 million.

- In November 2021, L3Harris was awarded a multi-year contract of USD 125 million to produce space electronic warfare systems that safeguard US military operations and warfighters.

Space Militarization Market Coverage

The report provides key insights into the space militarization market, and it focuses on technological developments, trends, and initiatives taken by the government in this sector. The report delves into market drivers, restraints, and opportunities, and analyzes key players and the competitive landscape within the market.

Report Scope

|

Report Features |

Description |

|

Market Size (2023-e) |

USD 48.5 billion |

|

Forecast Revenue (2030) |

USD 77.7 billion |

|

CAGR (2024-2030) |

6.7% |

|

Base Year for Estimation |

2023-e |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

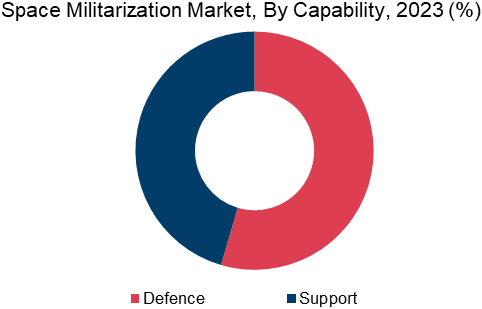

By Capability (Defense (Intelligence, Surveillance, and Reconnaissance, Electronic Warfare, Weapons), Support (Navigation, Communication, Others)), By Solution (Ground-Based Equipment (Ground-Based Space Surveillance Network, Ground Control Stations, Anti-Satellite Systems, Launch Facilities, Tracking & Surveillance Systems), Space-Based Equipment, Space Stations, Satellites (Low Earth Orbit (LEO), Medium Earth Orbit (MEO), Geostationary Earth Orbit (GEO), Beyond Geosynchronous Orbit)), Logistics & Services (Logistics, Space Launch Services, Space Situational Awareness)) |

|

Regional Analysis |

North America (US, Canada), Europe (Germany, France, UK, Spain, Italy), Asia-Pacific (China, Japan, South Korea, India), Latin America (Brazil, Mexico), Middle East and Africa (Saudi Arabia, UAE, South Africa) |

|

Competitive Landscape |

Airbus, BAE Systems, Boeing, CASC, General Dynamics, L3Harris, Lockheed Martin, Northrop Grumman, Raytheon, and Thales. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

|

Purchase Options |

We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

|

1.Introduction |

|

1.1. Study Assumptions and Market Definition |

|

1.2. Scope of the Study |

|

2.Research Methodology |

|

3.Executive Summary |

|

4.Market Dynamics |

|

4.1. Market Growth Drivers |

|

4.1.1.Growing need for defending national security from space-based threats |

|

4.1.2.Technological advancements in space-based military systems |

|

4.1.3.Growing reliance on space assets for national security |

|

4.2. Market Growth Restraints |

|

4.2.1.Space sustainability and environmental impacts |

|

4.2.2.International diplomatic relations |

|

4.3. Market Growth Opportunities |

|

4.3.1.Rise in commercial space ventures |

|

4.4. Porter’s Five Forces |

|

4.5. PESTLE Analysis |

|

5.Market Outlook |

|

5.1. Supply Chain Analysis |

|

5.2. Regulatory Framework |

|

5.3. Technology Analysis |

|

5.4. Patent Analysis |

|

5.5. Trade Analysis |

|

6.Market Segment Outlook (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

6.1. Segment Synopsis |

|

6.2. By Capability |

|

6.2.1.Defense |

|

6.2.1.1. Intelligence, Surveillance, and Reconnaissance |

|

6.2.1.2. Electronic Warfare |

|

6.2.1.3. Weapons |

|

6.2.2.Support |

|

6.2.2.1. Navigation |

|

6.2.2.2. Communication |

|

6.2.2.3. Others |

|

6.3. By Solution |

|

6.3.1.Ground-Based Equipment |

|

6.3.1.1. Ground-Based Space Surveillance Network |

|

6.3.1.2. Ground Control Stations |

|

6.3.1.3. Anti-Satellite Systems |

|

6.3.1.4. Launch Facilities |

|

6.3.1.5. Tracking & Surveillance Systems |

|

6.3.2.Space-Based Equipment |

|

6.3.2.1. Space Stations |

|

6.3.2.2. Satellites |

|

6.3.2.2.1. Low Earth Orbit (LEO) |

|

6.3.2.2.2. Medium Earth Orbit (MEO) |

|

6.3.2.2.3. Geostationary Earth Orbit (GEO) |

|

6.3.2.2.4. Beyond Geosynchronous Orbit |

|

6.3.3.Logistics & Services |

|

6.3.3.1. Logistics |

|

6.3.3.2. Space Launch Services |

|

6.3.3.3. Space Situational Awareness |

|

7.Regional Outlook (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

7.1. Global Market Synopsis |

|

7.2. North America |

|

7.2.1.North America Space Militarization Market Outlook |

|

7.2.2.US |

|

7.2.2.1. US Space Militarization Market, By Capability |

|

7.2.2.1.1. US Space Militarization Market for Defense |

|

7.2.2.1.2. US Space Militarization Market for Support |

|

7.2.2.2. US Space Militarization Market, By Solution |

|

7.2.2.2.1. US Space Militarization Market for Ground-Based Equipment |

|

7.2.2.2.2. US Space Militarization Market for Space-Based Equipment |

|

7.2.2.2.3. US Space Militarization Market for Logistics & Services |

|

*Note: Cross-segmentation by segments for each country will be covered as shown above. |

|

7.2.3.Canada |

|

7.3. Europe |

|

7.3.1.Europe Space Militarization Market Outlook |

|

7.3.2.Germany |

|

7.3.3.UK |

|

7.3.4.France |

|

7.3.5.Italy |

|

7.3.6.Spain |

|

7.4. Asia-Pacific |

|

7.4.1.Asia-Pacific Space Militarization Market Outlook |

|

7.4.2.China |

|

7.4.3.India |

|

7.4.4.Japan |

|

7.4.5.South Korea |

|

7.4.6.Australia |

|

7.5. Middle East & Africa |

|

7.5.1.Middle East & Africa Space Militarization Market Outlook |

|

7.5.2.Saudi Arabia |

|

7.5.3.UAE |

|

7.5.4.South Africa |

|

7.6. Latin America |

|

7.6.1.Latin America Space Militarization Market Outlook |

|

7.6.2.Brazil |

|

7.6.3.Mexico |

|

8.Competitive Landscape |

|

8.1. Market Share Analysis |

|

8.2. Company Strategy Analysis |

|

8.3. Competitive Matrix |

|

9.Company Profiles |

|

9.1. Airbus |

|

9.1.1.Company Synopsis |

|

9.1.2.Company Financials |

|

9.1.3.Product/Service Portfolio |

|

9.1.4.Recent Developments |

|

*Note: All the companies in section 9.1 will cover the same sub-chapters as above. |

|

9.2. BAE Systems |

|

9.3. Boeing |

|

9.4. CASC |

|

9.5. General Dynamics |

|

9.6. L3Harris |

|

9.7. Lockheed Martin |

|

9.8. Northrop |

|

9.9. Raytheon |

|

9.10. Thales |

Let us connect with you TOC

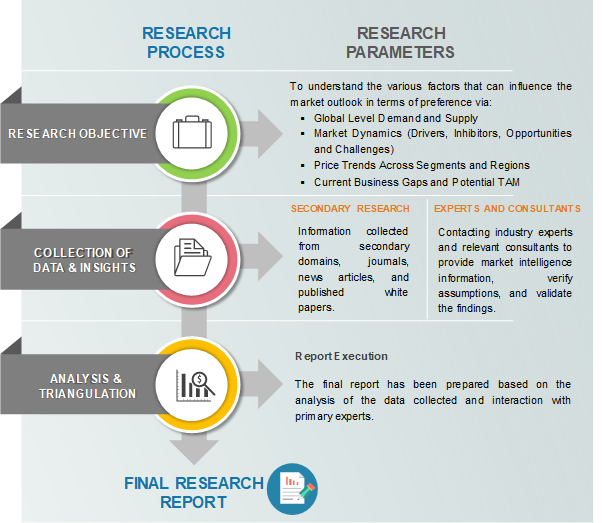

Intent Market Research employs a rigorous methodology to minimize residual errors by carefully defining the scope, validating findings through primary research, and consistently updating our in-house database. This dynamic approach allows us to capture ongoing market fluctuations and adapt to evolving market uncertainties.

The research factors used in our methodology vary depending on the specific market being analyzed. To begin with, we incorporate both demand and supply side information into our model to identify and address market gaps. Additionally, we also employ approaches such as Macro-Indicator Analysis, Factor Analysis, Value Chain-Based Sizing, and forecasting to further increase the accuracy of the numbers and validate the findings.

Research Approach

- Secondary Research Approach: During the initial phase of the research process, we acquire and accumulate extensive data continuously. This data is carefully filtered and validated through a variety of secondary sources.

- Primary Research Approach: Following the consolidation of data gathered through secondary research, we initiate a validation and verification process to verify all the market numbers and assumptions by engaging with the subject matter experts.

Data Collection, Analysis and Interpretation:

Research Methodology

Our market research methodology utilizes both top-down and bottom-up approaches to segment and estimate quantitative aspects of the market. We also employ multi-perspective analysis, examining the market from distinct viewpoints.

Available Formats