As per Intent Market Research, the Zigbee Home Automation Market was valued at USD 4.1 billion in 2023 and will surpass USD 7.1 billion by 2030; growing at a CAGR of 8.3% during 2024 - 2030.

The Zigbee Home Automation Market has emerged as a cornerstone of the Internet of Things (IoT) revolution, enabling seamless control of smart devices in homes, commercial spaces, and industries. Zigbee’s low-power, reliable communication protocol has positioned it as a preferred technology for integrating smart systems, addressing growing demands for energy efficiency, convenience, and security. With advancements in technology and increasing smart home adoption, the market is poised for substantial growth across various components, applications, and end-users.

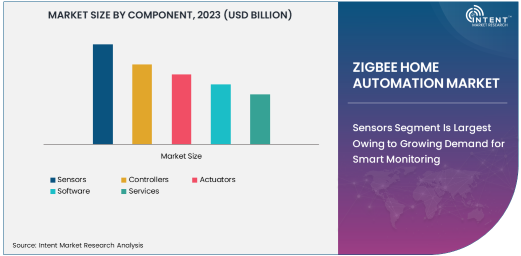

Sensors Segment Is Largest Owing to Growing Demand for Smart Monitoring

The sensors segment dominates the Zigbee home automation market, driven by the increasing need for real-time monitoring and data collection in smart homes. Sensors, ranging from motion and temperature to light and occupancy detectors, are critical for enabling automation, offering energy efficiency, and enhancing home security. Their ability to provide continuous feedback for adaptive systems has made them indispensable in modern automation solutions.

The proliferation of IoT devices has further spurred demand for sensors, particularly in residential and commercial spaces. With the integration of advanced AI and machine learning algorithms, sensors are now able to deliver predictive insights, transforming the way smart systems operate. This has cemented their role as a foundational component in Zigbee-enabled environments.

Security Systems Segment Is Fastest Owing to Rising Focus on Safety

Security systems represent the fastest-growing application in the Zigbee home automation market. The rising focus on home and commercial safety, coupled with an increasing number of smart surveillance solutions, has propelled the adoption of Zigbee-enabled security systems. These systems include smart cameras, alarm systems, door/window sensors, and motion detectors, all connected seamlessly for real-time alerts and remote monitoring.

The growth of this subsegment is supported by increasing urbanization and the adoption of smart cities, where security is paramount. Zigbee-based systems are particularly favored for their robust mesh networking, ensuring uninterrupted communication even in large properties. As concerns about privacy and asset protection continue to grow, the demand for innovative and reliable security solutions is expected to accelerate.

Software Segment Is Fastest Owing to Demand for Seamless Integration

The software segment is witnessing rapid growth, driven by the need for centralized control and seamless integration of smart devices. Zigbee software platforms enable users to manage and monitor various devices through a unified interface, providing enhanced convenience and operational efficiency. These platforms often feature user-friendly mobile applications and cloud-based solutions for remote access.

With the growing complexity of smart home ecosystems, the importance of intuitive and scalable software solutions has become paramount. Continuous innovations in AI and machine learning are further enhancing software capabilities, enabling personalized automation and predictive maintenance. This focus on innovation positions the software segment as a key driver in the market’s expansion.

Residential Segment Is Largest Owing to Rising Smart Home Adoption

The residential segment remains the largest end-user category, driven by increasing consumer interest in smart homes and energy-efficient solutions. Zigbee’s reliability and low power consumption make it an ideal choice for homeowners looking to integrate lighting, security, HVAC, and energy management systems.

The rising affordability of smart devices and growing awareness about energy conservation have further accelerated adoption in residential spaces. As more consumers prioritize convenience and sustainability, the demand for Zigbee-enabled home automation systems is expected to maintain its strong momentum in this segment.

Asia-Pacific Is Fastest Owing to Expanding Smart Cities

Asia-Pacific is the fastest-growing region in the Zigbee home automation market, fueled by rapid urbanization, rising disposable incomes, and government initiatives promoting smart cities. Countries like China, India, and South Korea are at the forefront, embracing IoT technologies to enhance quality of life and energy efficiency.

The region’s growing tech-savvy population and strong manufacturing base for electronic devices have further contributed to market growth. Additionally, supportive government policies and investments in smart infrastructure are expected to sustain Asia-Pacific’s leadership in the coming years.

Competitive Landscape

The Zigbee home automation market is highly competitive, with leading companies driving innovation and expanding their product portfolios to meet diverse consumer needs. Major players include Texas Instruments, Silicon Labs, NXP Semiconductors, and Philips Lighting (Signify N.V.), among others. These companies focus on strategic partnerships, mergers and acquisitions, and new product launches to strengthen their market presence.

The competitive landscape is characterized by advancements in technology and the development of interoperable solutions that ensure seamless device integration. As consumer expectations for smarter, more efficient systems continue to rise, companies are prioritizing research and development to stay ahead in this dynamic market.

List of Leading Companies:

- Texas Instruments Incorporated

- Silicon Labs

- NXP Semiconductors

- STMicroelectronics

- Renesas Electronics Corporation

- Microchip Technology Inc.

- Schneider Electric

- Honeywell International Inc.

- Legrand SA

- Samsung Electronics Co., Ltd.

- Belkin International, Inc.

- Philips Lighting (Signify N.V.)

- Acuity Brands, Inc.

- Johnson Controls International PLC

- ABB Ltd.

Recent Developments:

- In 2024, Silicon Labs launched a high-performance Zigbee module designed for energy-efficient smart home devices.

- Samsung announced enhanced Zigbee compatibility for its SmartThings ecosystem, allowing seamless integration of third-party devices.

- Philips Lighting (Signify) acquired a leading smart lighting startup to bolster its Zigbee-enabled product portfolio in 2023.

- Honeywell launched a new Zigbee-based security solution featuring AI integration for enhanced home surveillance.

- Texas Instruments partnered with a global IoT consortium in 2023 to advance open standards for Zigbee-based home automation systems.

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 4.1 Billion |

|

Forecasted Value (2030) |

USD 7.1 Billion |

|

CAGR (2024 – 2030) |

8.3% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Zigbee Home Automation Market By Component (Sensors, Controllers, Actuators, Software, Services), By Application (Lighting Control, Security Systems, HVAC Control, Energy Management, Smart Appliances), By End-User (Residential, Commercial, Industrial) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Texas Instruments Incorporated, Silicon Labs, NXP Semiconductors, STMicroelectronics, Renesas Electronics Corporation, Microchip Technology Inc., Schneider Electric, Honeywell International Inc., Legrand SA, Samsung Electronics Co., Ltd., Belkin International, Inc., Philips Lighting (Signify N.V.), Acuity Brands, Inc., Johnson Controls International PLC, ABB Ltd. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Zigbee Home Automation Market, by Component (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Sensors |

|

4.2. Controllers |

|

4.3. Actuators |

|

4.4. Software |

|

4.5. Services |

|

5. Zigbee Home Automation Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Lighting Control |

|

5.2. Security Systems |

|

5.3. HVAC Control |

|

5.4. Energy Management |

|

5.5. Smart Appliances |

|

6. Zigbee Home Automation Market, by End-User (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Residential |

|

6.2. Commercial |

|

6.3. Industrial |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Zigbee Home Automation Market, by Component |

|

7.2.7. North America Zigbee Home Automation Market, by Application |

|

7.2.8. North America Zigbee Home Automation Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Zigbee Home Automation Market, by Component |

|

7.2.9.1.2. US Zigbee Home Automation Market, by Application |

|

7.2.9.1.3. US Zigbee Home Automation Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Texas Instruments Incorporated |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Silicon Labs |

|

9.3. NXP Semiconductors |

|

9.4. STMicroelectronics |

|

9.5. Renesas Electronics Corporation |

|

9.6. Microchip Technology Inc. |

|

9.7. Schneider Electric |

|

9.8. Honeywell International Inc. |

|

9.9. Legrand SA |

|

9.10. Samsung Electronics Co., Ltd. |

|

9.11. Belkin International, Inc. |

|

9.12. Philips Lighting (Signify N.V.) |

|

9.13. Acuity Brands, Inc. |

|

9.14. Johnson Controls International PLC |

|

9.15. ABB Ltd. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Zigbee Home Automation Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Zigbee Home Automation Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Zigbee Home Automation Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA