As per Intent Market Research, the Zero-Emission Aircraft Market was valued at USD 3.7 billion in 2023 and will surpass USD 19.8 billion by 2030; growing at a CAGR of 27.1% during 2024 - 2030.

The zero-emission aircraft market is a rapidly evolving sector aimed at revolutionizing the aviation industry by significantly reducing carbon emissions. With growing concerns over climate change and increased regulatory pressure on the aviation sector to reduce its carbon footprint, zero-emission aircraft powered by hydrogen fuel cells, battery-electric systems, and hybrid technologies are gaining significant attention. This market includes technologies, aircraft types, end users, and power sources, all contributing to the shift towards more sustainable air travel. Governments, airlines, and aviation companies are investing heavily in the development of these technologies, making zero-emission aircraft a promising solution for the future of aviation.

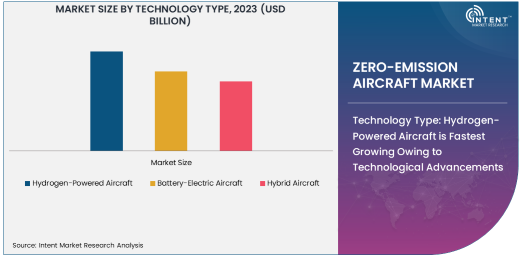

Technology Type: Hydrogen-Powered Aircraft is Fastest Growing Owing to Technological Advancements

Hydrogen-powered aircraft have emerged as one of the fastest-growing technologies in the zero-emission aircraft market. As the aviation industry seeks alternatives to fossil fuels, hydrogen offers a promising solution due to its high energy density and ability to produce zero emissions when burned or used in fuel cells. Leading aviation companies and governments are investing significantly in hydrogen technology, which is expected to play a crucial role in long-range, commercial air travel. With advancements in hydrogen storage, fuel cell efficiency, and aircraft design, hydrogen-powered aircraft are poised to become a key player in the transition to sustainable aviation. Hydrogen fuel cells are particularly advantageous in long-range flights where electric battery power may not provide sufficient energy capacity.

The increasing focus on hydrogen is driven by its potential to decarbonize both commercial and regional aviation. Additionally, the development of hydrogen refueling infrastructure, coupled with favorable policies and green technology incentives from governments worldwide, is further accelerating its growth. As a result, hydrogen-powered aircraft are expected to dominate the technological landscape in the coming years, especially for larger aircraft and intercontinental flights, where battery-electric solutions may fall short in terms of range and efficiency.

Range of Aircraft: Long-Range Aircraft is Largest Due to High Demand for Sustainable Travel

Among the different range segments, long-range aircraft are emerging as the largest subsegment within the zero-emission aircraft market. As global travel demand continues to recover and grow, airlines and manufacturers are focusing on developing sustainable long-range solutions that can cater to the increasing demand for international flights while minimizing environmental impact. These aircraft, powered by hydrogen or hybrid systems, offer the ability to cover longer distances without sacrificing efficiency or performance, making them ideal for high-capacity routes such as transcontinental and intercontinental flights.

The long-range segment is further driven by significant investments from aviation giants like Airbus and Boeing, who are developing hydrogen-powered long-range aircraft to meet both environmental targets and market demand for sustainable aviation. Additionally, as governments push for net-zero emissions by 2050, long-range aircraft equipped with zero-emission technologies are seen as a pivotal component in meeting these ambitious goals. The market for long-range zero-emission aircraft is expected to continue expanding as the aviation industry seeks to integrate sustainable solutions across its entire fleet.

End User: Commercial Aviation Dominates Owing to Largest Fleet and Market Potential

In the zero-emission aircraft market, commercial aviation represents the largest end-user segment. With the global aviation industry generating substantial carbon emissions, commercial airlines are under immense pressure to adopt sustainable technologies and reduce their environmental footprint. Commercial aviation accounts for a significant portion of the market due to the large number of aircraft in operation and the high demand for air travel. Airlines are increasingly exploring electric and hydrogen-powered solutions to meet regulatory requirements and consumer demand for eco-friendly travel options.

The growth of commercial aviation in the zero-emission market is fueled by several factors, including the development of lightweight, energy-efficient technologies and the substantial investment in green aviation by both airlines and governments. Key players in the sector are aiming to introduce zero-emission aircraft to their fleets in the coming years, with a particular focus on regional and short-haul flights as a first step toward broader integration. As airlines strive to achieve carbon neutrality, the commercial aviation sector is expected to remain the largest contributor to the growth of the zero-emission aircraft market.

Aircraft Type: Fixed-Wing Aircraft is Largest Due to Operational Versatility

Fixed-wing aircraft are the largest subsegment in the zero-emission aircraft market due to their operational versatility and scalability. These aircraft are already widely used in both commercial and private aviation and offer a proven design that can be adapted to new, sustainable propulsion technologies, including electric and hydrogen-powered systems. Fixed-wing aircraft are particularly well-suited for long-distance travel and can carry larger payloads compared to other types of aircraft, making them ideal candidates for the introduction of zero-emission technologies.

The demand for fixed-wing zero-emission aircraft is driven by the increasing need for efficient and environmentally friendly air travel across both short and long distances. Innovations in electric propulsion and hydrogen fuel cells are enabling manufacturers to design fixed-wing aircraft that are both energy-efficient and capable of serving high-demand routes. As the industry shifts toward sustainability, fixed-wing aircraft will continue to be the dominant aircraft type in the zero-emission segment, catering to both commercial airlines and private customers.

Power Source: Hydrogen Fuel Cells Lead the Way in Long-Term Sustainability

Hydrogen fuel cells are the leading power source in the zero-emission aircraft market due to their potential to provide high energy output with zero emissions. Hydrogen is increasingly seen as a viable alternative to traditional jet fuel because of its high energy density and the ability to produce only water vapor as a byproduct when used in fuel cells. This makes hydrogen a particularly attractive solution for long-range aircraft, where battery-electric technology may struggle with energy storage limitations.

The growth of hydrogen as a power source is supported by technological advancements in fuel cell efficiency and hydrogen storage systems. As more manufacturers and governments prioritize carbon-neutral aviation, hydrogen fuel cells are expected to play a crucial role in the development of zero-emission aircraft for commercial, military, and general aviation. In addition, hydrogen offers the advantage of being compatible with existing airport refueling infrastructure, further enhancing its potential for widespread adoption.

Regional Landscape: North America Leads the Zero-Emission Aircraft Market

North America is the largest region in the zero-emission aircraft market, driven by robust investments in research and development, favorable government policies, and strong demand for sustainable aviation solutions. The United States, in particular, is at the forefront of zero-emission aircraft development, with key players such as Boeing, ZeroAvia, and Joby Aviation leading the charge. The region’s strong regulatory push for emission reductions, along with its established aviation infrastructure, provides a fertile ground for the adoption of clean aircraft technologies.

North America’s dominance in the market is also fueled by collaborations between private companies and government agencies, such as NASA and the U.S. Department of Energy, which are working on advancing hydrogen fuel cell and electric propulsion systems. As North America continues to invest in green technologies, it is expected to maintain its leadership position in the zero-emission aircraft market for the foreseeable future.

Competitive Landscape and Leading Companies

The zero-emission aircraft market is highly competitive, with several key players driving innovation and technological development. Leading companies such as Airbus, Boeing, Rolls-Royce, and Honeywell are at the forefront, working on hydrogen-powered and electric aircraft solutions for commercial, military, and general aviation. In addition, emerging startups like ZeroAvia, Joby Aviation, and Lilium are pioneering the development of electric vertical take-off and landing (EVTOL) aircraft and hydrogen fuel cell technology.

These companies are competing not only on the basis of technological advancements but also in securing partnerships and funding to scale their innovations. Collaborations between aviation giants and governments are common, aiming to meet strict environmental regulations and target net-zero emissions. As the market continues to evolve, the competitive landscape will be defined by the ability to deliver efficient, reliable, and cost-effective zero-emission aircraft solutions.

Recent Developments:

- Airbus Launches New Hydrogen Aircraft Concept Airbus introduced a new hydrogen-powered aircraft concept aiming for commercial use by 2035, pushing the envelope for sustainable aviation.

- ZeroAvia Secures Funding for Hydrogen Aircraft Development ZeroAvia raised $50 million in funding to develop its hydrogen-powered aircraft, targeting regional air travel markets.

- Boeing Partners with Airlines for Electric Aircraft Trials Boeing has partnered with various airlines to test its electric aircraft prototypes, focusing on reducing emissions in short-haul flights.

- Rolls-Royce Completes Successful Test of All-Electric Aircraft Engine Rolls-Royce successfully tested an all-electric propulsion system for aircraft, marking a significant milestone in its clean aviation strategy.

- Joby Aviation Acquires Urban Aeronautics for EVTOL Expansion Joby Aviation acquired Urban Aeronautics, further expanding its electric vertical take-off and landing (EVTOL) capabilities to transform urban air mobility

List of Leading Companies:

- Airbus

- Boeing

- ZeroAvia

- Rolls-Royce

- Honeywell

- Electric Aircraft Corporation

- Magnix

- Universal Hydrogen

- Pipistrel

- Joby Aviation

- Vertical Aerospace

- Lilium

- AeroVironment

- Embraer

- Wright Electric

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 3.7 Billion |

|

Forecasted Value (2030) |

USD 19.8 Billion |

|

CAGR (2024 – 2030) |

27.1% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Zero-Emission Aircraft Market By Technology Type (Hydrogen-Powered Aircraft, Battery-Electric Aircraft, Hybrid Aircraft), By Range of Aircraft (Short-Range Aircraft, Medium-Range Aircraft, Long-Range Aircraft), By End-User Industry (Commercial Aviation, Military Aviation, General Aviation), By Aircraft Type (Fixed-Wing Aircraft, Rotorcraft, Unmanned Aerial Vehicles), By Power Source (Hydrogen Fuel Cells, Lithium-Ion Batteries, Hybrid Systems) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Airbus, Boeing, ZeroAvia, Rolls-Royce, Honeywell, Electric Aircraft Corporation, Magnix, Universal Hydrogen, Pipistrel, Joby Aviation, Vertical Aerospace, Lilium, AeroVironment, Embraer, Wright Electric |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Zero-Emission Aircraft Market, by Technology Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Hydrogen-Powered Aircraft |

|

4.2. Battery-Electric Aircraft |

|

4.3. Hybrid Aircraft |

|

5. Zero-Emission Aircraft Market, by Range of Aircraft (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Short-Range Aircraft |

|

5.2. Medium-Range Aircraft |

|

5.3. Long-Range Aircraft |

|

6. Zero-Emission Aircraft Market, by End User (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Commercial Aviation |

|

6.2. Military Aviation |

|

6.3. General Aviation |

|

7. Zero-Emission Aircraft Market, by Aircraft Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Fixed-Wing Aircraft |

|

7.2. Rotorcraft (Vertical Take-Off and Landing) |

|

7.3. Unmanned Aerial Vehicles (UAVs) |

|

8. Zero-Emission Aircraft Market, by Power Source (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Hydrogen Fuel Cells |

|

8.2. Lithium-Ion Batteries |

|

8.3. Hybrid Systems |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Zero-Emission Aircraft Market, by Technology Type |

|

9.2.7. North America Zero-Emission Aircraft Market, by Range of Aircraft |

|

9.2.8. North America Zero-Emission Aircraft Market, by End User |

|

9.2.9. North America Zero-Emission Aircraft Market, by Aircraft Type |

|

9.2.10. North America Zero-Emission Aircraft Market, by |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Zero-Emission Aircraft Market, by Technology Type |

|

9.2.11.1.2. US Zero-Emission Aircraft Market, by Range of Aircraft |

|

9.2.11.1.3. US Zero-Emission Aircraft Market, by End User |

|

9.2.11.1.4. US Zero-Emission Aircraft Market, by Aircraft Type |

|

9.2.11.1.5. US Zero-Emission Aircraft Market, by |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. Airbus |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Boeing |

|

11.3. ZeroAvia |

|

11.4. Rolls-Royce |

|

11.5. Honeywell |

|

11.6. Electric Aircraft Corporation |

|

11.7. Magnix |

|

11.8. Universal Hydrogen |

|

11.9. Pipistrel |

|

11.10. Joby Aviation |

|

11.11. Vertical Aerospace |

|

11.12. Lilium |

|

11.13. AeroVironment |

|

11.14. Embraer |

|

11.15. Wright Electric |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Zero-Emission Aircraft Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Zero-Emission Aircraft Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Zero-Emission Aircraft Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA