As per Intent Market Research, the Wireless Network Security Market was valued at USD 24.3 billion in 2023 and will surpass USD 56.4 billion by 2030; growing at a CAGR of 12.8% during 2024 - 2030.

The wireless network security market is witnessing robust growth due to the rising adoption of wireless networks across industries and the increasing prevalence of cyber threats. As organizations continue to embrace wireless communication technologies, ensuring the protection of sensitive data and network infrastructure has become paramount. The market is expanding rapidly as companies adopt advanced security solutions, including firewalls, encryption, and intrusion detection systems, to safeguard their networks from potential breaches. Additionally, the shift toward cloud-based deployments and the increasing integration of IoT devices are fueling the demand for effective wireless network security solutions.

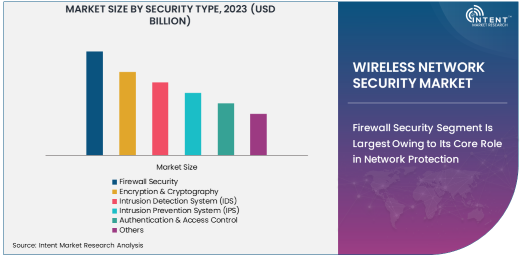

Firewall Security Segment Is Largest Owing to Its Core Role in Network Protection

Firewall security remains the largest segment within the wireless network security market due to its fundamental role in network defense. Firewalls are essential for monitoring and controlling incoming and outgoing network traffic based on predetermined security rules, forming the first line of defense against cyberattacks. They are widely deployed in both enterprise and consumer wireless networks for preventing unauthorized access and ensuring data integrity. The increasing frequency of cyberattacks and the need for regulatory compliance are driving the demand for firewall solutions, which offer a robust defense mechanism for both small enterprises and large enterprises across various industries.

The growing sophistication of cyber threats, coupled with the rise in the number of connected devices, has further reinforced the need for firewalls in protecting wireless networks. As organizations continue to migrate to digital platforms, the importance of firewall security in safeguarding sensitive data and maintaining trust with customers has never been more critical. Furthermore, firewall security technology is constantly evolving to address new vulnerabilities, ensuring that it remains the preferred solution for protecting wireless networks.

Cloud-Based Deployment Mode Is Fastest Growing Owing to Scalability and Flexibility

Cloud-based deployment is the fastest-growing segment in the wireless network security market, driven by the increasing adoption of cloud infrastructure across industries. Cloud security solutions offer scalability, flexibility, and cost-efficiency, enabling businesses to protect their networks without the need for extensive on-premises infrastructure. The growing demand for remote work solutions, cloud applications, and the Internet of Things (IoT) has significantly contributed to the rise of cloud-based security deployments. Businesses are increasingly opting for cloud-based solutions to streamline their security processes, ensure better management of security policies, and enhance their ability to respond to threats in real-time.

In addition, cloud-based security platforms provide a centralized approach to managing security across multiple locations, making them ideal for global organizations with distributed networks. As the market shifts toward more dynamic and agile operations, cloud-based wireless network security solutions are becoming essential for businesses that prioritize flexibility and scalability. With cloud deployments continuing to grow in the coming years, this segment is expected to remain a major driver of market expansion.

Telecommunications End-User Industry Is Largest Due to Critical Infrastructure Protection

The telecommunications industry is the largest end-user sector for wireless network security solutions, driven by the critical nature of communication infrastructure and the increasing volume of data transmitted over networks. Telecom operators manage vast amounts of sensitive customer data, including communication records, financial information, and personal details, making them prime targets for cybercriminals. As telecom networks evolve to support 5G and beyond, ensuring the security of wireless communication channels has become increasingly important. The need for robust security measures to protect against data breaches and service disruptions is fueling the demand for wireless network security solutions in this industry.

Telecommunications providers are investing heavily in securing their networks, particularly as they expand their service offerings to include IoT and cloud-based solutions. The industry’s reliance on a broad range of wireless technologies, including 4G, 5G, and Wi-Fi, further amplifies the need for comprehensive security solutions to mitigate risks associated with network vulnerabilities. As cybersecurity regulations become stricter and more advanced, telecommunications companies are prioritizing network security to maintain their competitive edge and preserve customer trust.

Network Security Application Is Largest Due to Increasing Cyber Threats

Network security is the largest application within the wireless network security market, driven by the rising frequency and sophistication of cyberattacks targeting wireless networks. Network security solutions focus on safeguarding the integrity of networks by preventing unauthorized access, data breaches, and attacks such as DDoS (Distributed Denial of Service). This application is integral to businesses of all sizes, ensuring that the critical infrastructure supporting operations, communications, and transactions remains protected from cybercriminals. The surge in remote work, the expansion of IoT devices, and increased reliance on cloud services have only heightened the need for robust network security measures.

Moreover, the rapid increase in network traffic, particularly with the rise of 5G and IoT, demands comprehensive network protection strategies. Network security solutions, including intrusion detection and prevention systems (IDS/IPS), firewalls, and encryption, are being integrated into wireless infrastructures to detect and mitigate potential threats proactively. As enterprises continue to expand their digital presence, network security will remain a key priority for organizations seeking to ensure business continuity and secure customer data.

Small & Medium Enterprises (SMEs) Are Fastest Growing Segment Due to Increased Cyber Threat Awareness

Small and medium-sized enterprises (SMEs) are the fastest-growing segment within the wireless network security market, as these businesses are increasingly recognizing the importance of network security in safeguarding their operations. Historically, SMEs have been less focused on cybersecurity due to budget constraints and a lack of resources. However, the growing threat of cyberattacks and heightened awareness of data breaches have prompted these organizations to invest in wireless network security solutions. SMEs are adopting affordable, cloud-based security tools that provide the necessary protection without the high costs typically associated with enterprise-level security systems.

As SMEs continue to digitize their operations and expand their online presence, they are becoming more vulnerable to cyber threats. The rise of cybercrime targeting smaller businesses is driving this segment's rapid growth, with network security solutions offering a vital safeguard against potential attacks. As a result, SMEs are increasingly seen as an attractive market for wireless network security providers looking to tap into this growing demand.

Asia-Pacific Region Is Fastest Growing Owing to Digital Transformation and Cybersecurity Awareness

The Asia-Pacific (APAC) region is the fastest-growing market for wireless network security, driven by rapid digital transformation and an increasing focus on cybersecurity. Countries in the region, including China, India, and Japan, are investing heavily in developing their digital infrastructures, which includes expanding wireless networks to support 5G, IoT, and cloud services. With this rapid growth comes an increased vulnerability to cyber threats, prompting both private and public sector organizations to adopt comprehensive security solutions. Governments in APAC are also enacting stricter cybersecurity regulations, further driving the demand for network security technologies.

The APAC region is home to a large number of small and medium-sized enterprises (SMEs), many of which are beginning to recognize the importance of securing their wireless networks. Additionally, the region's thriving telecommunications industry and increasing adoption of advanced technologies are contributing to the surge in demand for wireless network security solutions.

Competitive Landscape and Leading Companies

The wireless network security market is highly competitive, with a mix of established players and emerging companies offering a variety of security solutions. Leading companies such as Cisco Systems, Palo Alto Networks, and Fortinet continue to dominate the market, providing comprehensive security technologies that protect wireless networks from evolving threats. These companies offer a wide range of security solutions, including firewalls, intrusion prevention systems, and encryption technologies, to meet the diverse needs of organizations across various industries.

In addition to these giants, smaller, innovative firms are also making their mark in the market by offering specialized solutions targeting specific industries or use cases. As organizations face increasingly sophisticated cyber threats, the market for wireless network security will continue to grow, with providers focusing on delivering advanced, integrated security solutions that address the unique challenges of wireless environments. Competitive dynamics are also influenced by ongoing mergers and acquisitions, as companies look to expand their product portfolios and technological capabilities to stay ahead in the cybersecurity race.

List of Leading Companies:

- Cisco Systems Inc.

- Palo Alto Networks Inc.

- Fortinet, Inc.

- Check Point Software Technologies

- Juniper Networks, Inc.

- Huawei Technologies Co., Ltd.

- IBM Corporation

- Trend Micro Incorporated

- Symantec Corporation (Broadcom Inc.)

- McAfee Corp.

- Sophos Ltd.

- Barracuda Networks, Inc.

- FireEye, Inc.

- Zscaler, Inc.

- Radware Ltd.

Recent Developments:

- Cisco Systems launched a new AI-driven security platform aimed at enhancing the protection of wireless networks for enterprises.

- Palo Alto Networks acquired cloud security company "Cortex XSOAR" to expand its wireless network security offering.

- Fortinet announced the integration of 5G security features into its wireless network security solutions, focusing on enhanced threat prevention.

- McAfee introduced a new suite of end-to-end wireless security solutions designed for small and medium enterprises (SMEs).

- Check Point Software Technologies received regulatory approval for its acquisition of a cybersecurity firm specializing in wireless network threat detection.

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 24.3 Billion |

|

Forecasted Value (2030) |

USD 56.4 Billion |

|

CAGR (2024 – 2030) |

12.8% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Wireless Network Security Market By Security Type (Firewall Security, Encryption & Cryptography, Intrusion Detection System (IDS), Intrusion Prevention System (IPS), Authentication & Access Control), By Deployment Mode (On-Premises, Cloud-Based, Hybrid), By End-User Industry (Telecommunications, Healthcare, BFSI, Government & Defense, Retail, Energy & Utilities, Automotive, Manufacturing), By Application (Data Security, Network Security, Cloud Security, Endpoint Security, Application Security), By Organization Size (Small & Medium Enterprises (SMEs), Large Enterprises) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Cisco Systems Inc., Palo Alto Networks Inc., Fortinet, Inc., Check Point Software Technologies, Juniper Networks, Inc., Huawei Technologies Co., Ltd., IBM Corporation, Trend Micro Incorporated, Symantec Corporation (Broadcom Inc.), McAfee Corp., Sophos Ltd., Barracuda Networks, Inc., FireEye, Inc., Zscaler, Inc., Radware Ltd. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Wireless Network Security Market, by Security Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Firewall Security |

|

4.2. Encryption & Cryptography |

|

4.3. Intrusion Detection System (IDS) |

|

4.4. Intrusion Prevention System (IPS) |

|

4.5. Authentication & Access Control |

|

4.6. Others |

|

5. Wireless Network Security Market, by Deployment Mode (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. On-Premises |

|

5.2. Cloud-Based |

|

5.3. Hybrid |

|

6. Wireless Network Security Market, by End-User Industry (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Telecommunications |

|

6.2. Healthcare |

|

6.3. BFSI |

|

6.4. Government & Defense |

|

6.5. Retail |

|

6.6. Energy & Utilities |

|

6.7. Automotive |

|

6.8. Manufacturing |

|

7. Wireless Network Security Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Data Security |

|

7.2. Network Security |

|

7.3. Cloud Security |

|

7.4. Endpoint Security |

|

7.5. Application Security |

|

7.6. Others |

|

8. Wireless Network Security Market, by Organization Size (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Small & Medium Enterprises (SMEs) |

|

8.2. Large Enterprises |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Wireless Network Security Market, by Security Type |

|

9.2.7. North America Wireless Network Security Market, by Deployment Mode |

|

9.2.8. North America Wireless Network Security Market, by End-User Industry |

|

9.2.9. North America Wireless Network Security Market, by Application |

|

9.2.10. North America Wireless Network Security Market, by Organization Size |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Wireless Network Security Market, by Security Type |

|

9.2.11.1.2. US Wireless Network Security Market, by Deployment Mode |

|

9.2.11.1.3. US Wireless Network Security Market, by End-User Industry |

|

9.2.11.1.4. US Wireless Network Security Market, by Application |

|

9.2.11.1.5. US Wireless Network Security Market, by Organization Size |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. Cisco Systems Inc. |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Palo Alto Networks Inc. |

|

11.3. Fortinet, Inc. |

|

11.4. Check Point Software Technologies |

|

11.5. Juniper Networks, Inc. |

|

11.6. Huawei Technologies Co., Ltd. |

|

11.7. IBM Corporation |

|

11.8. Trend Micro Incorporated |

|

11.9. Symantec Corporation (Broadcom Inc.) |

|

11.10. McAfee Corp. |

|

11.11. Sophos Ltd. |

|

11.12. Barracuda Networks, Inc. |

|

11.13. FireEye, Inc. |

|

11.14. Zscaler, Inc. |

|

11.15. Radware Ltd. |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Wireless Network Security Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Wireless Network Security Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Wireless Network Security Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA