As per Intent Market Research, the Wine Packaging Boxes Market was valued at USD 1.6 billion in 2023 and will surpass USD 2.7 billion by 2030; growing at a CAGR of 7.7% during 2024 - 2030.

The wine packaging boxes market plays a crucial role in the global wine industry, providing essential solutions to ensure product safety, quality preservation, and consumer appeal. As the demand for wine continues to grow worldwide, packaging needs have evolved to meet various consumer preferences, regulatory standards, and sustainability goals. Wine packaging not only protects the product during transit but also serves as a vital marketing tool, influencing consumer purchasing decisions. As a result, innovations in packaging materials, designs, and distribution channels are continuously driving the market forward, with increasing attention to eco-friendly solutions.

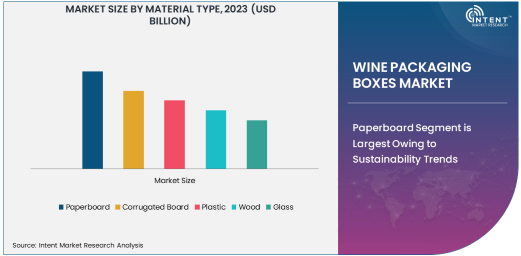

Paperboard Segment is Largest Owing to Sustainability Trends

Among the various material types used for wine packaging, paperboard is the largest segment, driven by its sustainability advantages and versatility. Paperboard is widely preferred for its ability to be easily recycled and molded into various shapes and sizes, making it ideal for both regular and custom wine packaging. The growing consumer demand for environmentally friendly packaging solutions has led wine producers to prioritize paperboard due to its biodegradability, recyclability, and lower carbon footprint compared to other materials like plastic. Additionally, paperboard offers excellent printability, enabling brands to use it for marketing purposes.

The versatility of paperboard allows manufacturers to produce both functional and aesthetically pleasing wine packaging, which has further contributed to its dominance. The eco-conscious shift in consumer behavior, along with increased regulatory pressure on reducing packaging waste, has bolstered the demand for paperboard packaging. As wine producers continue to cater to the sustainability-conscious market, the paperboard segment is poised for continuous growth in the coming years.

Bottle Packaging Segment is Largest Owing to Consumer Preferences

In the wine packaging boxes market, bottle packaging is the largest segment due to its widespread use and importance in preserving wine's integrity and enhancing consumer experience. Bottle packaging provides not only protection for the wine but also a visually appealing presentation, which is crucial in influencing consumer purchasing decisions. This type of packaging is commonly used by wine producers globally, as it ensures safe transportation and helps in maintaining the taste and quality of the product.

Bottle packaging is often paired with additional packaging solutions such as gift boxes or custom designs, further enhancing its appeal. The convenience of ready-to-sell packaging, combined with its ability to showcase the product, has made bottle packaging a preferred choice for wine producers. The consistent demand for quality wine, coupled with the growth in luxury wine markets, ensures that bottle packaging remains the dominant choice for packaging solutions in the wine industry.

Wine Producers Segment is Largest Owing to Market Demand

The wine producers segment is the largest subsegment within the end-user industry category, primarily due to the need for packaging solutions that meet the growing demand for wine globally. Wine producers require high-quality, durable packaging to preserve the wine during transportation and retail. As wine production and consumption increase globally, wine producers continue to seek packaging that ensures wine quality while reflecting their brand image. The push for sustainable, eco-friendly packaging has also led wine producers to adopt materials such as paperboard and glass, aligning with consumer preferences for environmentally conscious products.

This segment continues to experience growth as demand for both domestic and international wine production rises. The larger wineries, particularly in regions such as Europe and North America, are key drivers of this demand, as they require large volumes of packaging solutions to meet the global market's needs. Wine producers, therefore, remain the primary end-users of packaging materials, making this segment critical to the market's expansion.

Online Retail Segment is Fastest Growing Owing to E-Commerce Surge

The online retail segment is experiencing the fastest growth in the wine packaging boxes market, driven by the surge in e-commerce sales of wine. The convenience of purchasing wine online has become increasingly popular, especially with younger, tech-savvy consumers. The rise of online wine stores and direct-to-consumer sales platforms has significantly boosted the need for packaging solutions that ensure safe delivery while offering an appealing, sustainable product presentation. With the increasing popularity of wine subscription services and online wine retailers, the demand for specialized packaging that can withstand the shipping process and protect the product has escalated.

E-commerce platforms require packaging solutions that are both lightweight and robust, ensuring that wine bottles arrive in excellent condition. Furthermore, packaging needs to be customizable to create a personalized experience for consumers purchasing wine online. As online wine sales continue to grow, the demand for specialized packaging solutions is expected to increase, making the online retail segment the fastest-growing area of the market.

North America Region is Largest Owing to Wine Consumption

North America is the largest region in the wine packaging boxes market, driven by the high consumption of wine in the United States and Canada. The wine industry in North America is well-established, with a robust demand for wine packaging solutions that cater to both domestic markets and international exports. The increasing focus on sustainability and eco-friendly packaging further contributes to the region's dominance, as North American consumers are increasingly prioritizing environmentally responsible products.

Additionally, North America's strong wine production capabilities, particularly in states like California, have made it a key player in the global wine market. The region is home to some of the largest wine producers, who seek high-quality, innovative packaging solutions to meet consumer demand. As the wine packaging market in North America continues to grow, the region is expected to maintain its leadership position globally.

Leading Companies and Competitive Landscape

The wine packaging boxes market is competitive, with several key players dominating the industry. Companies such as Smurfit Kappa Group, Mondi Group, and DS Smith PLC are leading the market with their extensive product offerings and innovations in sustainable packaging solutions. These companies focus on providing eco-friendly, cost-effective packaging options that meet the evolving demands of the wine industry, from wineries to e-commerce platforms.

Smurfit Kappa, for example, offers a wide range of wine packaging solutions made from sustainable materials, while Mondi Group is known for its customized and flexible packaging offerings. The competitive landscape is characterized by a strong emphasis on innovation, sustainability, and customization, with companies continuously developing new packaging solutions that meet both functional and aesthetic needs. As consumer preferences shift toward sustainability, market leaders are investing heavily in research and development to provide environmentally friendly packaging materials that also deliver high performance.

List of Leading Companies:

- Smurfit Kappa Group

- International Paper Company

- DS Smith Plc

- Stora Enso Oyj

- Mondi Group

- Georgia-Pacific LLC

- WestRock Company

- Packaging Corporation of America (PCA)

- Sonoco Products Company

- Amcor PLC

- ULINE

- Pactiv Evergreen

- Tetra Pak International S.A.

- VinoPak Packaging

- GWP Group

Recent Developments:

- Smurfit Kappa strengthened its sustainability efforts with the acquisition of a new recycling facility, enabling the company to produce more eco-friendly wine packaging solutions.

- Amcor launched a new range of sustainable wine packaging that uses less plastic and is fully recyclable, catering to the growing demand for environmentally-friendly products.

- Mondi Group announced the opening of a new production facility dedicated to high-quality, custom wine packaging to support the luxury wine market.

- Tetra Pak introduced innovative packaging solutions for wine producers, focusing on preserving product quality and enhancing consumer convenience.

- WestRock entered into a partnership with a major wine exporter to create customized packaging solutions that improve brand recognition and shipping efficiency.

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 1.6 billion |

|

Forecasted Value (2030) |

USD 2.7 billion |

|

CAGR (2024 – 2030) |

7.7% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Wine Packaging Boxes Market By Material Type (Paperboard, Corrugated Board, Plastic, Wood, Glass), By Packaging Type (Bottle Packaging, Gift Packaging, Bulk Packaging, Custom Packaging), By End-User Industry (Wine Producers, Retailers & Wholesalers, E-commerce, Exporters), By Distribution Channel (Online Retail, Supermarkets/Hypermarkets, Wine Stores, Direct Sales) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Smurfit Kappa Group, International Paper Company, DS Smith Plc, Stora Enso Oyj, Mondi Group, Georgia-Pacific LLC, WestRock Company, Packaging Corporation of America (PCA), Sonoco Products Company, Amcor PLC, ULINE, Pactiv Evergreen, Tetra Pak International S.A., VinoPak Packaging, GWP Group |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Wine Packaging Boxes Market, by Material Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Paperboard |

|

4.2. Corrugated Board |

|

4.3. Plastic |

|

4.4. Wood |

|

4.5. Glass |

|

5. Wine Packaging Boxes Market, by Packaging Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Bottle Packaging |

|

5.2. Gift Packaging |

|

5.3. Bulk Packaging |

|

5.4. Custom Packaging |

|

6. Wine Packaging Boxes Market, by End-User Industry (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Wine Producers |

|

6.2. Retailers & Wholesalers |

|

6.3. E-commerce |

|

6.4. Exporters |

|

7. Wine Packaging Boxes Market, by Distribution Channel (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Online Retail |

|

7.2. Supermarkets/Hypermarkets |

|

7.3. Wine Stores |

|

7.4. Direct Sales |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Wine Packaging Boxes Market, by Material Type |

|

8.2.7. North America Wine Packaging Boxes Market, by Packaging Type |

|

8.2.8. North America Wine Packaging Boxes Market, by End-User Industry |

|

8.2.9. North America Wine Packaging Boxes Market, by Distribution Channel |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Wine Packaging Boxes Market, by Material Type |

|

8.2.10.1.2. US Wine Packaging Boxes Market, by Packaging Type |

|

8.2.10.1.3. US Wine Packaging Boxes Market, by End-User Industry |

|

8.2.10.1.4. US Wine Packaging Boxes Market, by Distribution Channel |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Smurfit Kappa Group |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. International Paper Company |

|

10.3. DS Smith Plc |

|

10.4. Stora Enso Oyj |

|

10.5. Mondi Group |

|

10.6. Georgia-Pacific LLC |

|

10.7. WestRock Company |

|

10.8. Packaging Corporation of America (PCA) |

|

10.9. Sonoco Products Company |

|

10.10. Amcor PLC |

|

10.11. ULINE |

|

10.12. Pactiv Evergreen |

|

10.13. Tetra Pak International S.A. |

|

10.14. VinoPak Packaging |

|

10.15. GWP Group |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Wine Packaging Boxes Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Wine Packaging Boxes Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Wine Packaging Boxes Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA