As per Intent Market Research, the Wine Market was valued at USD 391.3 billion in 2023 and will surpass USD 505.6 billion by 2030; growing at a CAGR of 3.7% during 2024 - 2030.

The global wine market continues to grow, fueled by rising consumer interest in premium products, a diversification of wine offerings, and an increased demand from emerging markets. The industry is segmented by product type, grape variety, price range, packaging type, distribution channel, and end-user industries, each of which presents unique trends. As consumer preferences shift towards high-quality, sustainable options, producers are innovating in packaging and distribution methods to cater to new markets and tastes. Additionally, the growth of e-commerce and changing demographic trends are driving transformations in how wine is sold and consumed.

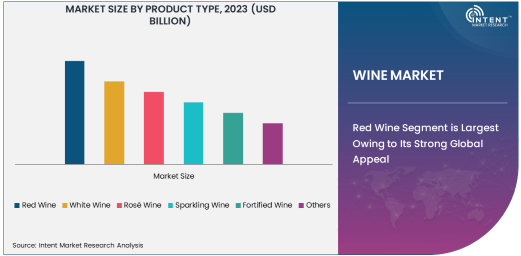

Red Wine Segment is Largest Owing to Its Strong Global Appeal

Among all product types, red wine holds the largest share of the market, thanks to its widespread popularity and deep cultural integration, particularly in regions such as Europe and the Americas. The rich flavors and versatility of red wine, which pair well with a variety of cuisines, have made it the go-to choice for wine lovers worldwide. Red wines, including varietals such as Cabernet Sauvignon and Merlot, benefit from long-established consumer demand and high production volumes. Additionally, red wine’s higher price point and mature market presence enable it to dominate in both volume and value in the wine industry.

The ongoing trend of health-conscious consumers also contributes to red wine’s dominance, as numerous studies highlight its potential cardiovascular benefits when consumed in moderation. Red wine’s status is further cemented by its role in various cultural and festive occasions, making it a staple in many households and restaurants globally. As a result, the demand for red wine continues to outpace other types, maintaining its position as the largest segment in the wine market.

Cabernet Sauvignon Grape Type is Largest Owing to Its Popularity

Cabernet Sauvignon is the largest and most cultivated grape variety in the wine industry, attributed to its versatility, rich flavor profile, and ability to thrive in a wide range of climates. This grape produces wines that are well-regarded for their deep color, bold tannins, and complex aromas, making it a favorite among both casual drinkers and connoisseurs alike. The global dominance of Cabernet Sauvignon has been driven by its use in some of the world’s most iconic wines, such as those from Bordeaux and Napa Valley, solidifying its status in both premium and mass-market segments.

The grape’s adaptability across different growing regions—ranging from the renowned wine regions of France, Chile, and the United States to emerging areas—has further fueled its popularity. As a result, Cabernet Sauvignon continues to be the dominant grape variety in the global wine market, with consistent growth in demand, especially in the premium wine category. This dominance has cemented the variety’s place at the forefront of wine production, ensuring its continued success for years to come.

Premium Price Range is Fastest Growing Owing to Increased Affluence

The premium price range segment is experiencing the fastest growth, driven by increasing disposable incomes, shifting consumer preferences, and a growing desire for luxury and high-quality products. Consumers, particularly in emerging markets, are becoming more willing to pay a higher price for exceptional wine experiences, including rare and aged wines. This growing interest in premium wines has been bolstered by a rising awareness of terroir, wine production methods, and the status that premium wines confer.

The premium wine market’s expansion is also fueled by the increasing interest in wine tourism and education. High-net-worth individuals and millennials, in particular, are seeking out wines that are not only rare but also carry a story or a unique production process. As a result, wineries are focusing on delivering superior quality and exclusive offerings to cater to the affluent market segment. This has led to a steady increase in the demand for premium wines, which is expected to continue as more consumers shift toward luxury and artisanal beverages.

Glass Bottles Segment is Largest Owing to Tradition and Consumer Preference

Glass bottles continue to dominate the wine packaging segment, holding the largest share due to their traditional appeal, ability to preserve wine quality, and global consumer preference. Glass is the preferred material for packaging wine as it maintains the integrity of the product, offering excellent protection against light and air, which can degrade the wine over time. Additionally, the classic image of wine in a glass bottle is deeply ingrained in consumer culture, enhancing the perception of quality.

Glass bottles also offer versatility in terms of design and branding, allowing wineries to create distinctive packaging that appeals to premium customers. Although alternative packaging options like cans and Tetra Paks are emerging, glass bottles remain the preferred choice for both red and white wines due to their ability to deliver both function and aesthetic value. This packaging format continues to thrive in both the luxury and mass-market wine categories, sustaining its position as the largest segment within wine packaging.

Supermarkets & Hypermarkets Segment is Largest Owing to Convenience

Supermarkets and hypermarkets are the largest distribution channels for wine, accounting for a significant share of global wine sales. The convenience of purchasing wine at large retail outlets, combined with wide product selection and competitive pricing, has made this distribution channel the go-to for many consumers. In addition to traditional wine, these retail giants offer a variety of options catering to all price ranges and preferences, from economy to premium wines, making it easy for consumers to find what they are looking for.

The dominance of supermarkets and hypermarkets is supported by their global presence and established consumer trust. As more consumers shift towards purchasing everyday items in these stores, the demand for wine in these settings continues to rise. With the convenience of one-stop shopping, including online options for home delivery, supermarkets and hypermarkets are expected to maintain their large market share, ensuring their continued leadership in the distribution of wine worldwide.

Alcoholic Beverage Industry is Largest End-User Owing to High Consumption of Wine

The alcoholic beverage industry remains the largest end-user for wine, driven by its significant role in the global beverage market. Wine is a key component of the alcoholic beverage sector, both as a standalone product and in mixed drinks. Its consumption is widespread across various cultures and regions, especially in Europe, North America, and emerging markets in Asia. The increasing adoption of wine in social, celebratory, and gastronomic settings has solidified its position within the alcoholic beverage industry.

The rise in consumer awareness about the different types of wine, production methods, and the health benefits of moderate consumption further boosts its popularity. The wine industry’s strong performance in the alcoholic beverage sector is also supported by an increase in wine tourism, which contributes to greater global consumption. As a result, the alcoholic beverage industry remains the primary sector for wine consumption, with continuous growth in both emerging and developed markets.

Europe Remains the Largest Region in the Wine Market

Europe remains the largest region in the wine market, with countries like France, Italy, and Spain leading the world in both wine production and consumption. The European wine market is deeply rooted in centuries-old traditions, and the region continues to be a global powerhouse in wine culture. Europe accounts for a significant share of both wine exports and imports, with a large portion of the wine consumed locally.

Wine tourism in countries like France and Italy also plays a major role in sustaining the region’s dominance in the market. Additionally, the rising interest in premium and organic wines in Europe is driving further growth, as consumers increasingly seek out higher-quality options. As a result, Europe remains the largest and most influential region in the global wine market, and its leadership is expected to continue in the foreseeable future.

Competitive Landscape and Leading Companies

The global wine market is highly competitive, with numerous players vying for market share across various segments. Leading companies such as E & J Gallo Winery, Constellation Brands, Pernod Ricard, and Treasury Wine Estates dominate the market, each with extensive portfolios of premium and mass-market wines. These companies are focused on product innovation, marketing strategies, and expanding their distribution networks to maintain their competitive edge.

In addition, several boutique wineries and smaller regional producers are capitalizing on the growing demand for niche and artisanal wines, catering to a more discerning consumer base. The competitive landscape is evolving as players also adapt to trends like sustainability, organic wine production, and e-commerce-driven sales. As consumer preferences continue to shift, the companies that can innovate while maintaining high standards of quality will lead the charge in the global wine market.

List of Leading Companies:

- E & J Gallo Winery

- Constellation Brands, Inc.

- The Wine Group

- Treasury Wine Estates

- Pernod Ricard

- Diageo

- Castel Group

- Bacardi Limited

- Moët Hennessy Louis Vuitton (LVMH)

- Bronco Wine Company

- Concha y Toro

- Accolade Wines

- Viña Concha y Toro S.A.

- Allied Domecq

- Carlsberg Group

Recent Developments:

- E & J Gallo Winery launched a new line of organic wines targeting environmentally conscious consumers.

- Constellation Brands acquired a major stake in a premium craft wine brand to diversify its portfolio.

- Treasury Wine Estates expanded its operations in Europe with new distribution agreements to increase market reach.

- Pernod Ricard announced the introduction of a new sustainable packaging initiative for its wine brands.

- Moët Hennessy Louis Vuitton (LVMH) completed the acquisition of a luxury wine estate in Bordeaux to enhance its wine portfolio.

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 391.3 Million |

|

Forecasted Value (2030) |

USD 505.6 Million |

|

CAGR (2024 – 2030) |

3.7% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Wine Market By Product Type (Red Wine, White Wine, Rosé Wine, Sparkling Wine, Fortified Wine), By Grape Type (Cabernet Sauvignon, Merlot, Chardonnay, Pinot Noir, Shiraz), By Price Range (Premium, Economy, Super Premium, Luxury), By Packaging Type (Glass Bottles, Cans, Tetra Pak), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online Retailers, Wine Clubs), and By End-User Industry (Alcoholic Beverage Industry, Food & Beverage Industry, Retail, Hospitality) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

E & J Gallo Winery, Constellation Brands, Inc., The Wine Group, Treasury Wine Estates, Pernod Ricard, Diageo, Castel Group, Bacardi Limited, Moët Hennessy Louis Vuitton (LVMH), Bronco Wine Company, Concha y Toro, Accolade Wines, Viña Concha y Toro S.A., Allied Domecq, Carlsberg Group |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Wine Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Red Wine |

|

4.2. White Wine |

|

4.3. Rosé Wine |

|

4.4. Sparkling Wine |

|

4.5. Fortified Wine |

|

4.6. Others |

|

5. Wine Market, by Grape Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Cabernet Sauvignon |

|

5.2. Merlot |

|

5.3. Chardonnay |

|

5.4. Pinot Noir |

|

5.5. Shiraz |

|

5.6. Others |

|

6. Wine Market, by Price Range (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Premium |

|

6.2. Economy |

|

6.3. Super Premium |

|

6.4. Luxury |

|

7. Wine Market, by Packaging Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Glass Bottles |

|

7.2. Cans |

|

7.3. Tetra Pak |

|

7.4. Others |

|

8. Wine Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Supermarkets & Hypermarkets |

|

8.2. Specialty Stores |

|

8.3. Online Retailers |

|

8.4. Wine Clubs |

|

8.5. Others |

|

9. Wine Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

9.1. Alcoholic Beverage Industry |

|

9.2. Food & Beverage Industry |

|

9.3. Retail |

|

9.4. Hospitality |

|

9.5. Others |

|

10. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

10.1. Regional Overview |

|

10.2. North America |

|

10.2.1. Regional Trends & Growth Drivers |

|

10.2.2. Barriers & Challenges |

|

10.2.3. Opportunities |

|

10.2.4. Factor Impact Analysis |

|

10.2.5. Technology Trends |

|

10.2.6. North America Wine Market, by Product Type |

|

10.2.7. North America Wine Market, by Grape Type |

|

10.2.8. North America Wine Market, by Packaging Type |

|

10.2.9. North America Wine Market, by Distribution Channel |

|

10.2.10. North America Wine Market, by End-User Industry |

|

10.2.11. By Country |

|

10.2.11.1. US |

|

10.2.11.1.1. US Wine Market, by Product Type |

|

10.2.11.1.2. US Wine Market, by Grape Type |

|

10.2.11.1.3. US Wine Market, by Packaging Type |

|

10.2.11.1.4. US Wine Market, by Distribution Channel |

|

10.2.11.1.5. US Wine Market, by End-User Industry |

|

10.2.11.2. Canada |

|

10.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

10.3. Europe |

|

10.4. Asia-Pacific |

|

10.5. Latin America |

|

10.6. Middle East & Africa |

|

11. Competitive Landscape |

|

11.1. Overview of the Key Players |

|

11.2. Competitive Ecosystem |

|

11.2.1. Level of Fragmentation |

|

11.2.2. Market Consolidation |

|

11.2.3. Product Innovation |

|

11.3. Company Share Analysis |

|

11.4. Company Benchmarking Matrix |

|

11.4.1. Strategic Overview |

|

11.4.2. Product Innovations |

|

11.5. Start-up Ecosystem |

|

11.6. Strategic Competitive Insights/ Customer Imperatives |

|

11.7. ESG Matrix/ Sustainability Matrix |

|

11.8. Manufacturing Network |

|

11.8.1. Locations |

|

11.8.2. Supply Chain and Logistics |

|

11.8.3. Product Flexibility/Customization |

|

11.8.4. Digital Transformation and Connectivity |

|

11.8.5. Environmental and Regulatory Compliance |

|

11.9. Technology Readiness Level Matrix |

|

11.10. Technology Maturity Curve |

|

11.11. Buying Criteria |

|

12. Company Profiles |

|

12.1. E & J Gallo Winery |

|

12.1.1. Company Overview |

|

12.1.2. Company Financials |

|

12.1.3. Product/Service Portfolio |

|

12.1.4. Recent Developments |

|

12.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

12.2. Constellation Brands, Inc. |

|

12.3. The Wine Group |

|

12.4. Treasury Wine Estates |

|

12.5. Pernod Ricard |

|

12.6. Diageo |

|

12.7. Castel Group |

|

12.8. Bacardi Limited |

|

12.9. Moët Hennessy Louis Vuitton (LVMH) |

|

12.10. Bronco Wine Company |

|

12.11. Concha y Toro |

|

12.12. Accolade Wines |

|

12.13. Viña Concha y Toro S.A. |

|

12.14. Allied Domecq |

|

12.15. Carlsberg Group |

|

13. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Wine Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Wine Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Wine Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA