As per Intent Market Research, the Wind Turbine Protection Market was valued at USD 2.2 billion in 2023 and will surpass USD 4.8 billion by 2030; growing at a CAGR of 11.7% during 2024 - 2030.

The wind turbine protection market plays a vital role in ensuring the safe and efficient operation of wind turbines, which are subject to various environmental and operational stresses. Protection systems are designed to shield turbines from hazards such as electrical surges, lightning strikes, temperature fluctuations, overloads, and mechanical vibrations. These systems are integral to minimizing downtime, enhancing turbine lifespan, and maintaining operational efficiency, thus playing a significant part in the wind energy sector’s overall growth. The market for wind turbine protection solutions is driven by the increasing deployment of wind turbines worldwide, particularly in both onshore and offshore locations, which face unique and sometimes extreme conditions.

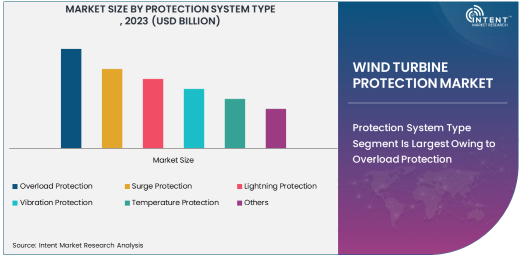

Protection System Type Segment Is Largest Owing to Overload Protection

In the Protection System Type segment, Overload Protection is the largest subsegment. Overload protection is essential for preventing damage to turbine components, especially the electrical and mechanical systems, when the turbine exceeds its capacity. Overloading can lead to significant failures and downtime, making this protection critical for ensuring the turbine continues to operate efficiently within its design parameters. Overload protection systems typically involve sophisticated sensors and controllers that detect abnormal conditions and take corrective action before serious damage occurs.

As wind turbines grow in size and capacity, particularly with the rise of offshore wind farms, the importance of overload protection has increased. Larger turbines require advanced systems to prevent failures caused by excessive power generation or extreme weather conditions. The continued development of more robust, real-time monitoring systems to detect overloads and other issues is driving the demand for advanced overload protection solutions. This trend is expected to continue, as maximizing energy output while minimizing downtime is critical for the economic viability of wind farms, particularly in regions with higher wind speeds or harsher operating conditions.

End-User Industry Segment Is Fastest Growing Owing to Wind Power Generation

The End-User Industry segment sees Wind Power Generation as the fastest-growing subsegment. Wind power generation, driven by the increasing global focus on renewable energy, is the primary sector utilizing advanced protection systems for wind turbines. The rising need for cleaner energy and the implementation of stricter regulations regarding energy efficiency and sustainability have created substantial growth in wind power generation. With an increasing number of wind farms being developed worldwide, both onshore and offshore, the demand for high-quality protection systems to ensure turbine reliability and reduce operational costs has soared.

Wind power generation companies are seeking advanced protection systems that can handle the unique challenges posed by both onshore and offshore wind farms, including high winds, lightning, and temperature extremes. As the global energy transition continues, the rapid expansion of wind power generation facilities, especially in Europe, North America, and Asia-Pacific, has directly contributed to the growth of protection systems designed for turbines. This growing demand for wind power generation protection solutions will drive continued innovation and expansion in the wind turbine protection market.

Application Segment Is Largest Owing to Offshore Wind Turbines

In the Application segment, Offshore Wind Turbines represent the largest subsegment. Offshore wind farms offer numerous advantages, including higher and more consistent wind speeds, which translate to higher energy generation. However, the harsh marine environment poses significant challenges, such as saltwater corrosion, extreme weather conditions, and the need for highly reliable protection systems. Offshore turbines are more vulnerable to mechanical stress and electrical surges, making protection systems an essential component of their design and operation.

Offshore wind farms are expanding rapidly, particularly in regions like Europe and the North Sea, where demand for clean energy is driving investments in large-scale offshore wind projects. The need for highly advanced protection systems in offshore turbines has contributed significantly to the market's expansion. As technology continues to evolve, offshore turbines are becoming more sophisticated, and so too are the protection systems designed to ensure their reliability. This trend of increasing offshore wind installations will likely remain the primary driver of the protection system market in the coming years, ensuring its dominant position in the application segment.

Technology Segment Is Fastest Growing Owing to Hybrid Protection

In the Technology segment, Hybrid Protection is the fastest-growing subsegment. Hybrid protection systems combine both mechanical and electrical protection mechanisms, offering enhanced reliability and flexibility in handling various turbine challenges. These systems leverage the strengths of both technologies, providing a multi-layered approach to protecting wind turbines from a broad range of risks, such as overloads, vibrations, lightning strikes, and temperature extremes. Hybrid systems are particularly valuable in improving turbine efficiency and reducing maintenance needs by offering a more comprehensive protection solution.

The growing interest in hybrid protection stems from the need for more robust and adaptable systems as wind turbines increase in size and complexity, especially in offshore applications. Hybrid protection systems are designed to address a wider array of potential threats, ensuring turbines continue to operate under varying environmental conditions. This trend is being driven by technological advancements in both electrical and mechanical protection components, making hybrid solutions more cost-effective and efficient. As the wind energy industry continues to evolve, the demand for hybrid protection systems is expected to increase, particularly in markets where offshore wind farms are becoming more prevalent.

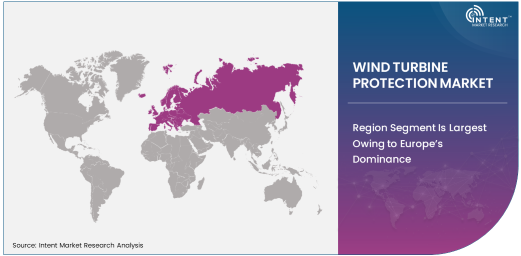

Region Segment Is Largest Owing to Europe’s Dominance

Europe is the largest region in the wind turbine protection market, accounting for the highest share of both onshore and offshore wind turbine installations. The region has been at the forefront of the wind energy transition, driven by strong governmental support for renewable energy and stringent sustainability targets. Countries like Denmark, the United Kingdom, Germany, and the Netherlands have extensive offshore wind farms that are a critical part of Europe’s energy strategy. As these countries continue to expand their wind power generation capacity, the demand for protection systems to ensure safe and reliable turbine operation will remain strong.

Europe’s dominance in the wind turbine protection market is also bolstered by the presence of several key players in the industry, including Siemens Gamesa, Vestas, and GE Renewable Energy, all of which are actively involved in developing advanced protection solutions for wind turbines. Moreover, the region’s regulatory frameworks require stringent safety standards, further driving the need for high-quality protection systems in wind turbines. As Europe continues to lead the global wind energy market, the region’s demand for protection systems will remain robust, solidifying its position as the largest market.

Leading Companies and Competitive Landscape

The wind turbine protection market is highly competitive, with several key players dominating the industry. Siemens Gamesa, Vestas Wind Systems, GE Renewable Energy, and Nordex SE are among the leading companies that provide advanced protection systems for wind turbines. These companies offer a wide range of protection solutions, including overload protection, surge suppression, lightning protection, and hybrid systems, designed to meet the growing demand for enhanced turbine safety and reliability.

The competitive landscape is also characterized by innovation, with companies continually investing in research and development to improve the efficiency, durability, and cost-effectiveness of protection systems. As the global market for wind energy continues to expand, particularly in offshore wind applications, the demand for more sophisticated protection systems will drive competition among these industry leaders. In addition to traditional players, newer entrants focusing on specific technological advancements, such as hybrid protection solutions, are also gaining traction in the market. The ongoing evolution of the wind turbine protection market is set to foster increased collaboration and partnerships among industry leaders, further driving the adoption of advanced protection technologies.

List of Leading Companies:

- Siemens Gamesa Renewable Energy

- Vestas Wind Systems

- GE Renewable Energy

- Nordex SE

- Schneider Electric

- ABB Ltd.

- Emerson Electric Co.

- Eaton Corporation

- Senvion

- TMEIC Corporation

- Mitsubishi Heavy Industries

- ZF Friedrichshafen AG

- Winergy (Schaeffler Group)

- SKF Group

- Nidec Corporation

Recent Developments:

- Siemens Gamesa Renewable Energy launched a new wind turbine protection solution designed to improve the safety and operational efficiency of offshore wind turbines in harsh marine environments.

- Vestas Wind Systems announced a partnership with a leading supplier of lightning protection systems, aiming to enhance the durability and reliability of their turbines in areas prone to thunderstorms.

- GE Renewable Energy received regulatory approval for its new surge protection system for wind turbines, which is set to be implemented in both onshore and offshore wind farms worldwide.

- Schneider Electric unveiled an upgraded wind turbine protection system featuring real-time monitoring and predictive analytics to identify potential faults before they lead to failures.

- Nidec Corporation acquired a leading manufacturer of vibration protection technology to expand its portfolio of wind turbine protection solutions, enhancing its competitive edge in the market

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 2.2 Billion |

|

Forecasted Value (2030) |

USD 4.8 Billion |

|

CAGR (2024 – 2030) |

11.7% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Wind Turbine Protection Market By Protection System Type (Overload Protection, Surge Protection, Lightning Protection, Vibration Protection, Temperature Protection), By End-User Industry (Wind Power Generation, Wind Farm Operators, Wind Turbine Manufacturers), By Application (Onshore Wind Turbines, Offshore Wind Turbines), By Technology (Mechanical Protection, Electrical Protection, Hybrid Protection) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Siemens Gamesa Renewable Energy, Vestas Wind Systems, GE Renewable Energy, Nordex SE, Schneider Electric, ABB Ltd., Emerson Electric Co., Eaton Corporation, Senvion, TMEIC Corporation, Mitsubishi Heavy Industries, ZF Friedrichshafen AG, Winergy (Schaeffler Group), SKF Group, Nidec Corporation |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Wind Turbine Protection Market, by Protection System Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Overload Protection |

|

4.2. Surge Protection |

|

4.3. Lightning Protection |

|

4.4. Vibration Protection |

|

4.5. Temperature Protection |

|

4.6. Others |

|

5. Wind Turbine Protection Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Wind Power Generation |

|

5.2. Wind Farm Operators |

|

5.3. Wind Turbine Manufacturers |

|

6. Wind Turbine Protection Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Onshore Wind Turbines |

|

6.2. Offshore Wind Turbines |

|

7. Wind Turbine Protection Market, by Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Mechanical Protection |

|

7.2. Electrical Protection |

|

7.3. Hybrid Protection |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Wind Turbine Protection Market, by Protection System Type |

|

8.2.7. North America Wind Turbine Protection Market, by End-User Industry |

|

8.2.8. North America Wind Turbine Protection Market, by Application |

|

8.2.9. North America Wind Turbine Protection Market, by Technology |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Wind Turbine Protection Market, by Protection System Type |

|

8.2.10.1.2. US Wind Turbine Protection Market, by End-User Industry |

|

8.2.10.1.3. US Wind Turbine Protection Market, by Application |

|

8.2.10.1.4. US Wind Turbine Protection Market, by Technology |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Siemens Gamesa Renewable Energy |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Vestas Wind Systems |

|

10.3. GE Renewable Energy |

|

10.4. Nordex SE |

|

10.5. Schneider Electric |

|

10.6. ABB Ltd. |

|

10.7. Emerson Electric Co. |

|

10.8. Eaton Corporation |

|

10.9. Senvion |

|

10.10. TMEIC Corporation |

|

10.11. Mitsubishi Heavy Industries |

|

10.12. ZF Friedrichshafen AG |

|

10.13. Winergy (Schaeffler Group) |

|

10.14. SKF Group |

|

10.15. Nidec Corporation |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Wind Turbine Protection Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Wind Turbine Protection Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Wind Turbine Protection Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA