As per Intent Market Research, the Wind Turbine Pitch and Yaw Drive Market was valued at USD 3.0 billion in 2023 and will surpass USD 6.1 billion by 2030; growing at a CAGR of 11.0% during 2024 - 2030.

The wind turbine pitch and yaw drive market is a critical component of the growing wind energy sector. These drive systems are essential in controlling the positioning of wind turbine blades (pitch) and adjusting the direction of the nacelle (yaw) to ensure maximum energy efficiency. As the global demand for renewable energy rises, the need for advanced turbine technologies, including pitch and yaw drives, has become increasingly important to optimize turbine performance and reduce operational costs. The market is witnessing significant technological advancements, including the development of hybrid systems and integration of more efficient mechanical and electrical components, contributing to the growth of the market across various regions.

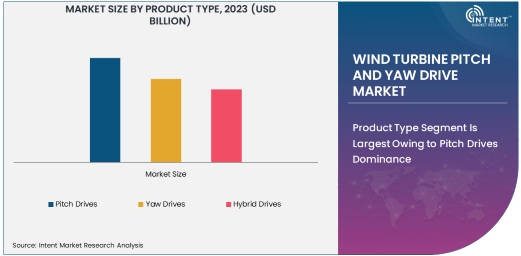

Product Type Segment Is Largest Owing to Pitch Drives Dominance

In the Product Type segment, Pitch Drives hold the largest share, driven by their crucial role in maximizing the performance and efficiency of wind turbines. Pitch drives adjust the angle of the turbine blades to capture the optimal amount of wind energy and protect the turbine from wind speeds that may be too high, preventing damage. The high demand for pitch drives is attributed to the increasing number of onshore and offshore wind farms and the push towards improving turbine efficiency and longevity. As the wind turbine market grows, so does the need for reliable and advanced pitch control systems to ensure turbines operate at peak performance.

Pitch drives are essential for wind turbines as they allow for precise control over blade angles, improving energy capture in fluctuating wind conditions. As technology advances, pitch drives are becoming more efficient, requiring less maintenance and offering longer operational lifespans. This trend is particularly evident in offshore wind turbines, where reliability and durability are paramount due to the harsh marine environment. Thus, the demand for advanced pitch drives is expected to remain strong, making them the dominant product type in the wind turbine pitch and yaw drive market.

Component Type Segment Is Fastest Growing Owing to Electrical Components

In the Component Type segment, Electrical Components are the fastest-growing subsegment, driven by the increasing adoption of more efficient, precise, and less maintenance-intensive technologies in wind turbines. Electrical pitch and yaw drives utilize electrical actuators and advanced control systems, offering greater precision and flexibility compared to mechanical alternatives. These electrical systems also contribute to the overall efficiency of wind turbines, helping to reduce energy consumption and improve performance. As wind turbine operators seek to minimize downtime and optimize their energy output, the shift towards electrical components is accelerating.

The demand for electrical components is further fueled by the ongoing development of smart wind turbines, which integrate IoT and AI technologies to enable real-time monitoring and performance optimization. Electrical drives, particularly those used in pitch and yaw systems, are a key enabler of these smart technologies, offering more control and adaptability. With the increasing focus on reducing the cost of energy generation and increasing turbine lifespan, electrical components are expected to continue their rapid growth in the wind turbine pitch and yaw drive market, especially in newer offshore and large-scale onshore installations.

End-User Industry Segment Is Largest Owing to Wind Power Generation

In the End-User Industry segment, Wind Power Generation is the largest subsegment, as it is directly linked to the demand for wind turbines and the related technologies. Wind power generation is the primary driver for the installation of pitch and yaw drive systems, as these components are essential for turbine functionality. The global push toward renewable energy and carbon reduction goals has led to an increased emphasis on wind power generation, which in turn drives the demand for more efficient and reliable wind turbines. As more wind farms are being established, both onshore and offshore, the need for effective turbine control systems becomes increasingly important.

Wind power generation’s dominance in this segment is underscored by the rapid expansion of wind farms worldwide, especially in regions like Europe, North America, and Asia. As countries invest heavily in renewable energy to meet sustainability goals, the demand for wind power generation systems, including pitch and yaw drives, continues to grow. The market for these components is therefore closely aligned with the ongoing global transition towards cleaner, more sustainable energy sources. The strong growth of wind power generation will continue to drive innovation in pitch and yaw drive technologies, ensuring their position as the largest subsegment in the end-user industry category.

Application Segment Is Fastest Growing Owing to Offshore Wind Turbines

In the Application segment, Offshore Wind Turbines represent the fastest-growing subsegment. Offshore wind energy has gained significant momentum due to the advantages of higher and more consistent wind speeds found at sea, which allow turbines to generate more power. As a result, offshore wind farms are being developed at an accelerated pace, and this growth is driving the demand for advanced pitch and yaw drive systems designed to withstand the unique challenges of the offshore environment. These turbines require highly reliable and durable drive systems that can perform efficiently in harsh marine conditions.

Offshore wind turbines are increasingly being deployed in deep-water locations, necessitating the development of more robust and sophisticated turbine systems, including pitch and yaw drives. The need for these advanced systems to optimize turbine operation and ensure long-term performance in challenging offshore conditions is fueling the market for pitch and yaw drive components. As offshore wind capacity continues to grow, particularly in Europe, Asia-Pacific, and North America, the demand for specialized pitch and yaw drives for offshore wind turbines is expected to rise significantly.

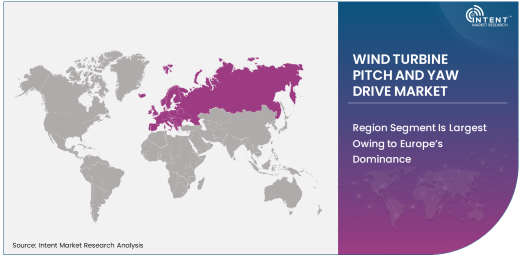

Region Segment Is Largest Owing to Europe’s Dominance

Europe is the largest region in the wind turbine pitch and yaw drive market, driven by its strong commitment to renewable energy and the widespread development of offshore wind farms. The European Union has set ambitious targets for wind energy generation as part of its Green Deal, and countries like the United Kingdom, Germany, and Denmark are leading the way in offshore wind installations. The high demand for advanced and reliable pitch and yaw drive systems for these offshore turbines has made Europe the dominant market for these components. Additionally, many of the world’s leading wind turbine manufacturers, including Siemens Gamesa and Vestas, are headquartered in Europe, further strengthening the region’s position in the global market.

The European market benefits from a well-established infrastructure for wind turbine manufacturing, research, and development, alongside supportive regulatory frameworks that incentivize the growth of renewable energy. As offshore wind farms become more prevalent and large-scale onshore wind projects continue to expand, the demand for efficient pitch and yaw drive systems in Europe will continue to drive the global market’s growth. Europe’s leadership in offshore wind energy is expected to sustain its position as the largest region in the pitch and yaw drive market for the foreseeable future.

Leading Companies and Competitive Landscape

The wind turbine pitch and yaw drive market is highly competitive, with several key players leading the charge in technology development and market share. Siemens Gamesa, Vestas Wind Systems, GE Renewable Energy, and Nordex SE are among the top companies in this sector, providing cutting-edge solutions for pitch and yaw drive systems. These companies have a significant presence across both onshore and offshore wind energy projects, offering a wide range of products and services designed to improve turbine efficiency, reduce operational costs, and increase the reliability of wind farms.

The competitive landscape is characterized by continuous innovation, with companies focusing on improving the durability, efficiency, and cost-effectiveness of pitch and yaw drive systems. In addition, partnerships, mergers, and acquisitions are common as companies seek to enhance their technological capabilities and expand their market reach. The market is also witnessing the emergence of specialized players focusing on hybrid drive systems and electrical components, which are gaining popularity due to their efficiency and reduced maintenance requirements. As the wind energy sector continues to grow, the competition among these companies will intensify, with a strong focus on technological advancements and global market expansion.

List of Leading Companies:

- Siemens Gamesa Renewable Energy

- Vestas Wind Systems

- GE Renewable Energy

- Nordex SE

- ZF Friedrichshafen AG

- Moventas (part of Sumitomo Drive Technologies)

- Nidec Corporation

- Emerson Electric Co.

- Svendborg Brakes

- SKF Group

- Torgeir Rødseth Wind Turbine Systems

- Liebherr Group

- Bachmann Electronic

- Ingeteam

- Winergy (Schaeffler Group)

Recent Developments:

- Siemens Gamesa Renewable Energy launched an advanced pitch control system designed to improve the efficiency and reliability of offshore wind turbines in harsh environments.

- Vestas Wind Systems announced a partnership with ZF Friedrichshafen AG to co-develop next-generation yaw drives aimed at enhancing turbine performance in offshore wind farms.

- GE Renewable Energy completed a significant upgrade to its pitch drive technology, focusing on reducing maintenance costs and extending the lifespan of turbine components.

- Nidec Corporation acquired a wind turbine drive system manufacturer to expand its presence in the global wind energy market and strengthen its portfolio of pitch and yaw drive solutions.

- Winergy (Schaeffler Group) received regulatory approval for a new hybrid yaw drive system that significantly reduces energy consumption in offshore wind turbine applications

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 3.0 Billion |

|

Forecasted Value (2030) |

USD 6.1 Billion |

|

CAGR (2024 – 2030) |

11.0% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Wind Turbine Pitch and Yaw Drive Market By Product Type (Pitch Drives, Yaw Drives, Hybrid Drives), By Component Type (Mechanical Components, Electrical Components), By End-User Industry (Wind Power Generation, Wind Farm Operators, Wind Turbine Manufacturers), By Application (Onshore Wind Turbines, Offshore Wind Turbines) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Siemens Gamesa Renewable Energy, Vestas Wind Systems, GE Renewable Energy, Nordex SE, ZF Friedrichshafen AG, Moventas (part of Sumitomo Drive Technologies), Nidec Corporation, Emerson Electric Co., Svendborg Brakes, SKF Group, Torgeir Rødseth Wind Turbine Systems, Liebherr Group, Bachmann Electronic, Ingeteam, Winergy (Schaeffler Group) |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Wind Turbine Pitch and Yaw Drive Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Pitch Drives |

|

4.2. Yaw Drives |

|

4.3. Hybrid Drives |

|

5. Wind Turbine Pitch and Yaw Drive Market, by Component Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Mechanical Components |

|

5.2. Electrical Components |

|

6. Wind Turbine Pitch and Yaw Drive Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Wind Power Generation |

|

6.2. Wind Farm Operators |

|

6.3. Wind Turbine Manufacturers |

|

7. Wind Turbine Pitch and Yaw Drive Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Onshore Wind Turbines |

|

7.2. Offshore Wind Turbines |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Wind Turbine Pitch and Yaw Drive Market, by Product Type |

|

8.2.7. North America Wind Turbine Pitch and Yaw Drive Market, by Component Type |

|

8.2.8. North America Wind Turbine Pitch and Yaw Drive Market, by End-User Industry |

|

8.2.9. North America Wind Turbine Pitch and Yaw Drive Market, by Application |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Wind Turbine Pitch and Yaw Drive Market, by Product Type |

|

8.2.10.1.2. US Wind Turbine Pitch and Yaw Drive Market, by Component Type |

|

8.2.10.1.3. US Wind Turbine Pitch and Yaw Drive Market, by End-User Industry |

|

8.2.10.1.4. US Wind Turbine Pitch and Yaw Drive Market, by Application |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Siemens Gamesa Renewable Energy |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Vestas Wind Systems |

|

10.3. GE Renewable Energy |

|

10.4. Nordex SE |

|

10.5. ZF Friedrichshafen AG |

|

10.6. Moventas (part of Sumitomo Drive Technologies) |

|

10.7. Nidec Corporation |

|

10.8. Emerson Electric Co. |

|

10.9. Svendborg Brakes |

|

10.10. SKF Group |

|

10.11. Torgeir Rødseth Wind Turbine Systems |

|

10.12. Liebherr Group |

|

10.13. Bachmann Electronic |

|

10.14. Ingeteam |

|

10.15. Winergy (Schaeffler Group) |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Wind Turbine Pitch and Yaw Drive Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Wind Turbine Pitch and Yaw Drive Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Wind Turbine Pitch and Yaw Drive Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA