As per Intent Market Research, the White Biotechnology Market was valued at USD 9.6 billion in 2024-e and will surpass USD 19.5 billion by 2030; growing at a CAGR of 12.6% during 2025 - 2030.

White biotechnology, also known as industrial biotechnology, is revolutionizing various industries by leveraging biological systems and organisms to produce valuable products and processes. This market is experiencing rapid growth due to the increasing demand for sustainable, environmentally friendly alternatives to traditional chemical processes. The rise of renewable bio-based products, particularly in industries such as biofuels, biochemicals, and bioplastics, is driving significant investment and research in this space. The increasing focus on reducing carbon footprints and promoting a circular economy is pushing industries toward adopting more sustainable methods, where white biotechnology plays a key role.

Technologies such as enzyme-based, microbial-based, and fermentation-based methods have gained prominence in this market due to their ability to produce high-efficiency, low-cost products. These biotechnologies enable the use of renewable feedstocks like plant-based resources, agricultural residues, and organic waste, contributing to a greener future. Furthermore, white biotechnology has wide applications across several sectors, including pharmaceuticals, food and feed additives, and agriculture, which further enhances its appeal in meeting the evolving needs of industries seeking sustainable solutions.

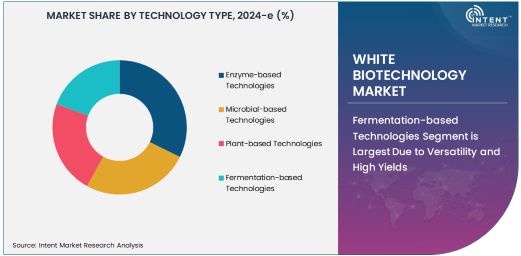

Fermentation-based Technologies Segment is Largest Due to Versatility and High Yields

Fermentation-based technologies are the largest segment in the white biotechnology market, primarily due to their versatility, scalability, and ability to produce high yields of bio-based products. This technology is widely used in the production of biofuels, biochemicals, pharmaceuticals, and food and feed additives. The fermentation process allows microorganisms, such as bacteria, yeast, and fungi, to convert raw materials like sugars, starches, or agricultural residues into valuable products. This technology offers a sustainable alternative to traditional chemical processes and is well-suited for large-scale production.

The widespread adoption of fermentation-based processes is driven by their ability to produce a wide variety of products efficiently and economically. Additionally, fermentation-based technologies can be used with various feedstocks, including renewable plant-based materials, waste products, and even carbon dioxide, making them a vital tool in addressing global sustainability challenges. As industries increasingly focus on reducing their environmental impact and improving resource efficiency, fermentation-based technologies are expected to continue driving growth in the white biotechnology market.

Bioplastics Application is Fastest Growing Due to Demand for Sustainable Materials

The bioplastics application segment is the fastest-growing within the white biotechnology market, driven by the increasing consumer demand for eco-friendly, sustainable materials. Traditional plastics derived from petroleum resources have raised environmental concerns due to their non-biodegradability and their contribution to plastic pollution. Bioplastics, which are produced from renewable sources such as plant starch, vegetable oils, or microorganisms, offer a viable alternative with a reduced environmental footprint. These materials can be used in packaging, textiles, automotive, and consumer goods, where they offer similar functionality to conventional plastics but with the advantage of being biodegradable or recyclable.

The rapid growth of the bioplastics segment is supported by stringent environmental regulations and growing awareness among consumers and businesses about sustainability. As companies strive to reduce their reliance on fossil fuels and improve their sustainability practices, the demand for bioplastics is expected to rise sharply. Additionally, advancements in bioplastic production technologies, including the use of microorganisms for bio-based polymer synthesis, are contributing to the affordability and scalability of bioplastics, further boosting their market potential.

North America Leads the White Biotechnology Market Due to Advanced Research and Industrial Adoption

North America holds the largest share of the white biotechnology market, largely due to its strong industrial base, advanced research and development capabilities, and supportive regulatory environment. The region is home to leading companies and research institutes focused on biotechnology innovations, and its well-established infrastructure supports the commercialization of biotechnological advancements. The United States, in particular, has made significant strides in promoting the adoption of sustainable technologies, including those within the white biotechnology sector, through policies and initiatives aimed at reducing environmental impacts and promoting renewable resources.

The growing emphasis on bio-based products and renewable energy, alongside the presence of several key players in sectors like biofuels, biochemicals, and bioplastics, positions North America as a leader in the white biotechnology market. Furthermore, the region's large-scale manufacturing capabilities and demand for sustainable solutions across various industries, including automotive, packaging, and agriculture, contribute to its continued dominance in the market.

Leading Companies and Competitive Landscape

The white biotechnology market is highly competitive, with numerous companies and research institutions focused on developing and commercializing advanced biotechnological solutions. Key players in the market include BASF SE, DowDuPont, Novozymes, DSM, and LanzaTech, among others. These companies are actively engaged in the development of enzyme-based, microbial-based, and fermentation-based technologies to produce biofuels, bioplastics, and other bio-based products.

The competitive landscape is marked by strong investments in research and development, strategic partnerships, and acquisitions aimed at expanding product portfolios and market reach. Companies are increasingly focusing on enhancing the efficiency and scalability of their biotechnological processes to reduce costs and meet the growing demand for sustainable solutions. As industries continue to prioritize sustainability and the shift toward a circular economy accelerates, the white biotechnology market is expected to see further innovation and increased competition among leading players, resulting in a more diversified and competitive market landscape.

Recent Developments:

- XXXXIn December 2024, Novozymes announced a breakthrough enzyme technology that enhances the production of biofuels, reducing energy consumption in the process.

- In November 2024, DSM launched a new bio-based solution for the textile industry, reducing the environmental footprint of fabric production.

- In October 2024, BASF SE partnered with a leading chemical company to develop sustainable bioplastics derived from plant-based raw materials.

- In September 2024, DuPont de Nemours, Inc. introduced an innovative biologic product aimed at increasing crop yield and sustainability in agriculture.

- In August 2024, Syngenta launched a new bio-pesticide product that provides an eco-friendly solution for pest management in crop production.

List of Leading Companies:

- Novozymes

- DSM

- BASF SE

- DuPont de Nemours, Inc.

- Evonik Industries

- Astellas Pharma Inc.

- Syngenta

- Biocatalysts Ltd.

- Lonza Group

- Genomatica

- Codexis, Inc.

- Amyris, Inc.

- Lallemand Inc.

- Fujifilm Diosynth Biotechnologies

- Ineos Bio

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 9.6 billion |

|

Forecasted Value (2030) |

USD 19.5 billion |

|

CAGR (2025 – 2030) |

12.6% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

White Biotechnology Market By Technology Type (Enzyme-based Technologies, Microbial-based Technologies, Plant-based Technologies, Fermentation-based Technologies), By Application (Biofuels, Biochemical Production, Bioplastics, Pharmaceuticals, Food and Feed Additives, Agriculture) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Novozymes, DSM, BASF SE, DuPont de Nemours, Inc., Evonik Industries, Astellas Pharma Inc., Syngenta, Biocatalysts Ltd., Lonza Group, Genomatica, Codexis, Inc., Amyris, Inc., Lallemand Inc., Fujifilm Diosynth Biotechnologies, Ineos Bio |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. White Biotechnology Market, by Technology Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Enzyme-based Technologies |

|

4.2. Microbial-based Technologies |

|

4.3. Plant-based Technologies |

|

4.4. Fermentation-based Technologies |

|

5. White Biotechnology Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Biofuels |

|

5.2. Biochemical Production |

|

5.3. Bioplastics |

|

5.4. Pharmaceuticals |

|

5.5. Food and Feed Additives |

|

5.6. Agriculture |

|

5.7. Others |

|

6. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Regional Overview |

|

6.2. North America |

|

6.2.1. Regional Trends & Growth Drivers |

|

6.2.2. Barriers & Challenges |

|

6.2.3. Opportunities |

|

6.2.4. Factor Impact Analysis |

|

6.2.5. Technology Trends |

|

6.2.6. North America White Biotechnology Market, by Technology Type |

|

6.2.7. North America White Biotechnology Market, by Application |

|

6.2.8. By Country |

|

6.2.8.1. US |

|

6.2.8.1.1. US White Biotechnology Market, by Technology Type |

|

6.2.8.1.2. US White Biotechnology Market, by Application |

|

6.2.8.2. Canada |

|

6.2.8.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

6.3. Europe |

|

6.4. Asia-Pacific |

|

6.5. Latin America |

|

6.6. Middle East & Africa |

|

7. Competitive Landscape |

|

7.1. Overview of the Key Players |

|

7.2. Competitive Ecosystem |

|

7.2.1. Level of Fragmentation |

|

7.2.2. Market Consolidation |

|

7.2.3. Product Innovation |

|

7.3. Company Share Analysis |

|

7.4. Company Benchmarking Matrix |

|

7.4.1. Strategic Overview |

|

7.4.2. Product Innovations |

|

7.5. Start-up Ecosystem |

|

7.6. Strategic Competitive Insights/ Customer Imperatives |

|

7.7. ESG Matrix/ Sustainability Matrix |

|

7.8. Manufacturing Network |

|

7.8.1. Locations |

|

7.8.2. Supply Chain and Logistics |

|

7.8.3. Product Flexibility/Customization |

|

7.8.4. Digital Transformation and Connectivity |

|

7.8.5. Environmental and Regulatory Compliance |

|

7.9. Technology Readiness Level Matrix |

|

7.10. Technology Maturity Curve |

|

7.11. Buying Criteria |

|

8. Company Profiles |

|

8.1. Novozymes |

|

8.1.1. Company Overview |

|

8.1.2. Company Financials |

|

8.1.3. Product/Service Portfolio |

|

8.1.4. Recent Developments |

|

8.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

8.2. DSM |

|

8.3. BASF SE |

|

8.4. DuPont de Nemours, Inc. |

|

8.5. Evonik Industries |

|

8.6. Astellas Pharma Inc. |

|

8.7. Syngenta |

|

8.8. Biocatalysts Ltd. |

|

8.9. Lonza Group |

|

8.10. Genomatica |

|

8.11. Codexis, Inc. |

|

8.12. Amyris, Inc. |

|

8.13. Lallemand Inc. |

|

8.14. Fujifilm Diosynth Biotechnologies |

|

8.15. Ineos Bio |

|

9. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the White Biotechnology Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the White Biotechnology Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the White Biotechnology Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA