As per Intent Market Research, the Wheeled Crane Market was valued at USD 15.6 billion in 2023 and will surpass USD 24.0 billion by 2030; growing at a CAGR of 6.3% during 2024 - 2030.

The wheeled crane market has seen significant growth, driven by the increasing demand for lifting and material handling solutions across various industries. These cranes are essential for heavy-duty operations, offering mobility, versatility, and high lifting capacity, making them indispensable in construction, oil & gas, and other industrial applications. As infrastructure development accelerates globally, wheeled cranes have gained traction due to their ability to navigate challenging terrains while providing efficient lifting solutions. This segment is characterized by several product types, applications, and distribution channels, each with its own set of growth drivers.

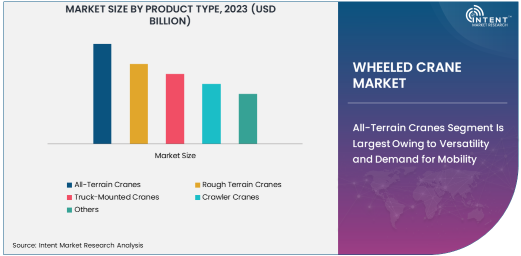

All-Terrain Cranes Segment Is Largest Owing to Versatility and Demand for Mobility

All-terrain cranes hold the largest share in the wheeled crane market, driven by their versatility and ability to perform in both rough and smooth terrains. These cranes are designed to operate efficiently on a wide range of surfaces, from urban streets to remote construction sites, providing crucial support in infrastructure development, industrial projects, and oil & gas operations. Their ability to travel on highways and rough terrains makes them an ideal choice for projects that require both mobility and heavy lifting capacity. The growing emphasis on infrastructure development, coupled with the need for cranes that can handle diverse site conditions, has propelled the demand for all-terrain cranes.

The increasing adoption of all-terrain cranes is also attributed to technological advancements, such as improved engines and lifting capabilities, making them more fuel-efficient and capable of handling larger loads. As construction projects become more complex and demanding, the role of these cranes becomes even more critical. The all-terrain crane segment’s growth is further fueled by expanding markets in emerging economies, where large-scale construction and infrastructure projects are prevalent.

Construction Application Is Fastest Growing Due to Expanding Infrastructure Projects

The construction sector is the fastest-growing application for wheeled cranes, driven by the increasing demand for infrastructure projects globally. Governments and private companies are investing heavily in urbanization, roadways, bridges, and commercial real estate, all of which require heavy lifting machinery. Wheeled cranes, particularly all-terrain and rough-terrain models, are vital for these large-scale projects due to their ability to handle heavy loads and operate in challenging environments. The construction sector’s growing demand for cranes is further supported by the rise in residential and commercial development, particularly in emerging markets.

This growth is also being fueled by the trend of constructing taller and more complex buildings, which require the use of advanced lifting equipment that can move large materials with precision. Additionally, the construction industry’s shift toward more sustainable and energy-efficient buildings has led to increased demand for cranes that can support green construction efforts, such as the use of eco-friendly materials and technologies.

Online Platforms Distribution Channel Is Growing Rapidly Due to E-Commerce Integration

Among various distribution channels, online platforms are experiencing the fastest growth in the wheeled crane market. As more industries move towards digital transformation, crane manufacturers are increasingly leveraging e-commerce platforms to reach a broader customer base. Online sales provide benefits such as greater convenience, transparent pricing, and easier comparison of different crane models, which is contributing to the rapid adoption of this distribution channel. The growing trend of online procurement in the construction and industrial sectors is a key driver of this growth, as companies seek more efficient ways to acquire heavy machinery.

Moreover, the integration of digital tools, such as virtual product demonstrations and real-time customer support, enhances the online purchasing experience, making it easier for buyers to make informed decisions. As e-commerce continues to expand globally, it is expected to play an increasingly important role in facilitating the purchase and delivery of wheeled cranes, particularly for small to medium-sized enterprises that require affordable, efficient equipment.

Oil & Gas End-User Industry Is Largest Due to Heavy Lifting Needs in Extraction and Exploration

The oil & gas industry remains the largest end-user sector for wheeled cranes, owing to the heavy lifting and material handling requirements in both extraction and exploration activities. Cranes are essential for lifting large equipment and machinery in oil fields, offshore platforms, and refineries. The need for cranes that can operate in harsh environments, such as offshore rigs and remote locations, positions all-terrain and rough-terrain cranes as the primary choice for these operations. Additionally, the oil & gas industry’s reliance on cranes for tasks such as transportation and installation of large components has cemented their status as a critical tool in the sector.

With oil prices fluctuating and exploration becoming more challenging, the industry’s demand for cranes that can support complex and large-scale operations continues to rise. This trend is expected to persist as the global oil and gas sector shifts toward more technologically advanced extraction methods, which will require specialized cranes capable of handling larger, more complex loads.

Asia Pacific Region Is Fastest Growing Owing to Robust Infrastructure Development

Asia Pacific is the fastest-growing region in the wheeled crane market, driven by substantial investments in infrastructure and construction projects. Countries like China, India, and Japan are witnessing rapid urbanization, with a sharp increase in the number of large-scale projects, such as residential complexes, highways, and bridges. The need for advanced cranes that can operate across diverse terrains is fueling market growth in the region. Moreover, the increased demand for renewable energy projects, such as wind farms and solar installations, is further boosting the need for wheeled cranes to handle the heavy lifting of turbines and other large equipment.

The region’s rapid industrialization and urbanization are expected to continue driving the demand for wheeled cranes, particularly in developing economies that are expanding their infrastructure to accommodate growing populations and economic development. As these markets continue to mature, the demand for cranes in sectors such as construction, oil & gas, and manufacturing will remain robust.

Leading Companies and Competitive Landscape

The competitive landscape of the wheeled crane market is marked by the presence of several key players, including Liebherr Group, Terex Corporation, Konecranes, SANY Group, and Manitowoc, among others. These companies dominate the market through continuous innovation, strategic partnerships, and geographic expansion. Liebherr, for instance, is known for its all-terrain cranes, which are widely used in construction, infrastructure, and industrial applications. Similarly, Terex has a strong presence in the rough terrain and truck-mounted crane segments, providing versatile solutions for various industries.

The market is also characterized by increasing mergers and acquisitions as companies seek to expand their product portfolios and enhance their technological capabilities. Manufacturers are focusing on developing more efficient cranes with advanced features, such as improved safety systems and fuel efficiency, to meet the rising demand for sustainable and high-performance lifting solutions. As the market continues to evolve, competition will intensify, with companies striving to maintain market leadership by offering innovative products and tailored solutions for a diverse customer base.

Recent Developments:

- Terex Corporation announced the launch of a new all-terrain crane, focusing on increasing lifting capacity and improving fuel efficiency, catering to the growing demand in the construction sector

- SANY Group expanded its global presence by acquiring a leading North American crane manufacturer, reinforcing its position in the mobile crane market

- Konecranes introduced a new line of electric wheeled cranes with reduced emissions, aligning with sustainability trends in the industrial lifting market

- Tadano Ltd. received regulatory approval for their new hybrid-powered truck-mounted cranes in Europe, marking a significant step in reducing carbon footprint in the crane market

- Zoomlion unveiled an advanced all-terrain crane with enhanced technology integration, providing better safety features and real-time load monitoring, aimed at the oil and gas industry

List of Leading Companies:

- Liebherr Group

- Terex Corporation

- Konecranes

- SANY Group

- XCMG Group

- Mitsubishi Heavy Industries

- Zoomlion Heavy Industry Science & Technology Co., Ltd.

- Manitowoc

- Cargotec Corporation

- Cranesmart Systems

- Doosan Infracore

- Link-Belt Cranes

- Tadano Ltd.

- Fassi Gru S.p.A.

- Palfinger AG

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 15.6 Billion |

|

Forecasted Value (2030) |

USD 24.0 Billion |

|

CAGR (2024 – 2030) |

6.3% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Wheeled Crane Market By Product Type (All-Terrain Cranes, Rough Terrain Cranes, Truck-Mounted Cranes, Crawler Cranes), By Application (Construction, Oil & Gas, Mining, Infrastructure, Industrial), By Distribution Channel (Direct Sales, Dealers and Distributors, Online Platforms), By End-User Industry (Construction, Oil & Gas, Manufacturing, Mining, Utilities) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Liebherr Group, Terex Corporation, Konecranes, SANY Group, XCMG Group, Mitsubishi Heavy Industries, Zoomlion Heavy Industry Science & Technology Co., Ltd., Manitowoc, Cargotec Corporation, Cranesmart Systems, Doosan Infracore, Link-Belt Cranes, Tadano Ltd., Fassi Gru S.p.A., Palfinger AG |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Wheeled Crane Market, by Product Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. All-Terrain Cranes |

|

4.2. Rough Terrain Cranes |

|

4.3. Truck-Mounted Cranes |

|

4.4. Crawler Cranes |

|

4.5. Others |

|

5. Wheeled Crane Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Construction |

|

5.2. Oil & Gas |

|

5.3. Mining |

|

5.4. Infrastructure |

|

5.5. Industrial |

|

6. Wheeled Crane Market, by Distribution Channel (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Direct Sales |

|

6.2. Dealers and Distributors |

|

6.3. Online Platforms |

|

7. Wheeled Crane Market, by End-User Industry (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Construction |

|

7.2. Oil & Gas |

|

7.3. Manufacturing |

|

7.4. Mining |

|

7.5. Utilities |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Wheeled Crane Market, by Product Type |

|

8.2.7. North America Wheeled Crane Market, by Application |

|

8.2.8. North America Wheeled Crane Market, by Distribution Channel |

|

8.2.9. North America Wheeled Crane Market, by End-User Industry |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Wheeled Crane Market, by Product Type |

|

8.2.10.1.2. US Wheeled Crane Market, by Application |

|

8.2.10.1.3. US Wheeled Crane Market, by Distribution Channel |

|

8.2.10.1.4. US Wheeled Crane Market, by End-User Industry |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Liebherr Group |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Terex Corporation |

|

10.3. Konecranes |

|

10.4. SANY Group |

|

10.5. XCMG Group |

|

10.6. Mitsubishi Heavy Industries |

|

10.7. Zoomlion Heavy Industry Science & Technology Co., Ltd. |

|

10.8. Manitowoc |

|

10.9. Cargotec Corporation |

|

10.10. Cranesmart Systems |

|

10.11. Doosan Infracore |

|

10.12. Link-Belt Cranes |

|

10.13. Tadano Ltd. |

|

10.14. Fassi Gru S.p.A. |

|

10.15. Palfinger AG |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Wheeled Crane Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Wheeled Crane Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Wheeled Crane Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA