As per Intent Market Research, the Wheelchair and Components Market was valued at USD 11.1 billion in 2023 and will surpass USD 14.8 billion by 2030; growing at a CAGR of 4.2% during 2024 - 2030.

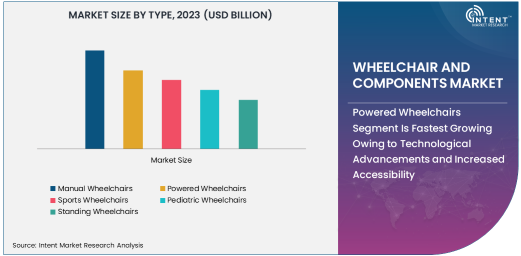

The wheelchair market is witnessing significant growth, driven by technological advancements and the rising demand for mobility solutions. Among the various types of wheelchairs, powered wheelchairs are growing at the fastest rate. Powered wheelchairs, also known as electric wheelchairs, provide users with enhanced mobility, convenience, and independence. These wheelchairs are equipped with motors and batteries, allowing individuals with limited strength or mobility to move with ease. The increasing adoption of powered wheelchairs is largely attributed to the aging population, the growing prevalence of disabilities, and the demand for innovative, user-friendly mobility aids.

Powered Wheelchairs Segment Is Fastest Growing Owing to Technological Advancements and Increased Accessibility

The growth of the powered wheelchair segment is fueled by advances in battery technology, lightweight designs, and enhanced user interfaces. These innovations have made powered wheelchairs more affordable, durable, and functional. As a result, consumers are increasingly opting for powered solutions over manual alternatives, especially in developed markets with high healthcare accessibility. Additionally, the rise of smart technologies integrated into powered wheelchairs, such as joystick controllers, remote diagnostics, and navigational assistance, has bolstered their appeal, contributing to their expanding market share.

Batteries for Powered Wheelchairs Are Key to Growth in Component Market

The wheelchair components market is seeing rapid innovations, especially in the realm of powered wheelchairs, where batteries play a pivotal role. Batteries are essential for powered wheelchairs as they supply the energy needed for mobility and functionality. With the continuous improvement in battery efficiency, charging times, and longevity, batteries have become a crucial factor in the performance and adoption of powered wheelchairs. This subsegment is experiencing significant demand as more consumers look for longer-lasting, higher-capacity batteries to improve the usability of their powered wheelchairs.

The increasing reliance on powered wheelchairs, particularly in regions with aging populations, has driven the demand for advanced battery solutions. Lithium-ion batteries, in particular, are gaining traction due to their light weight, longer lifespan, and fast-charging capabilities. As technology continues to evolve, the development of even more efficient and sustainable batteries is expected to further propel growth in this subsegment, making it one of the most critical components in the wheelchair market.

Home Care Segment Is Largest Due to Growing Demand for In-Home Healthcare

The demand for wheelchairs in the home care segment is surging as more individuals opt for in-home healthcare solutions. With the increasing aging population and the rising prevalence of chronic diseases, patients are seeking more personalized care options that allow them to live independently. Home care services are becoming a preferred choice for many, as they offer a more comfortable and cost-effective alternative to hospital stays or nursing home care. This shift in healthcare dynamics has led to a significant rise in the demand for mobility aids, including wheelchairs, to enhance the quality of life for individuals receiving care at home.

The home care segment is the largest because it encompasses a wide range of users, from the elderly to those with long-term disabilities, who require mobility aids for daily activities. Furthermore, the increasing availability of home healthcare services and the growing trend toward aging-in-place initiatives are expected to sustain and accelerate the demand for home care wheelchairs. As a result, this subsegment is expected to maintain its dominance in the coming years, further driving the overall growth of the wheelchair market.

North America Leads the Wheelchair Market Due to High Healthcare Spending and Advanced Infrastructure

North America holds the largest share of the global wheelchair market, driven by high healthcare spending, advanced infrastructure, and the increasing prevalence of mobility impairments among the aging population. The region’s robust healthcare system, combined with the high awareness of assistive technologies, has led to the widespread adoption of mobility aids, including wheelchairs. Additionally, government initiatives and insurance coverage for assistive devices have made wheelchairs more accessible to those in need, further driving market growth.

In North America, the United States stands out as the primary growth driver, with a large number of elderly individuals requiring mobility solutions and increasing healthcare investments supporting the adoption of advanced wheelchair technologies. The growing demand for powered wheelchairs and the rise in home care services have contributed to the expansion of the wheelchair market in this region. As the aging population continues to grow, North America is expected to maintain its dominance in the global wheelchair market.

Competitive Landscape: Leading Companies and Market Dynamics

The wheelchair and components market is highly competitive, with both global and regional players vying for market share. Leading companies such as Invacare Corporation, Ottobock, Drive DeVilbiss Healthcare, and Sunrise Medical are at the forefront of innovation, offering a wide range of manual and powered wheelchairs, along with key components such as tires, frames, and batteries. These companies invest heavily in research and development to improve the functionality, comfort, and durability of their products, catering to the diverse needs of wheelchair users.

The competitive landscape is characterized by strategic partnerships, mergers, and acquisitions as companies seek to expand their product portfolios and reach new markets. Additionally, the development of smart wheelchair technologies and the integration of IoT-enabled devices are reshaping the market, with companies increasingly focusing on offering high-tech solutions. The growing trend of customizations for specific patient needs, along with an emphasis on sustainability in manufacturing processes, is expected to shape the future dynamics of the wheelchair market. As the market continues to evolve, companies that can deliver innovative, cost-effective, and user-centric solutions will likely dominate the competitive landscape.

Recent Developments:

- Invacare Corporation announced the launch of a new line of lightweight manual wheelchairs designed for easier portability and comfort in late 2023.

- Permobil expanded its product portfolio with the introduction of an advanced powered wheelchair featuring cutting-edge joystick control and battery technology in early 2024.

- Drive DeVilbiss Healthcare acquired a smaller competitor in the mobility aids sector, strengthening its market position in Europe in mid-2023.

- Ottobock received regulatory approval for a new smart wheelchair that integrates IoT technology to track user mobility and health metrics in late 2023.

- Sunrise Medical launched a new range of sports wheelchairs in 2024, targeting athletes with disabilities and integrating enhanced ergonomics and durability features.

List of Leading Companies:

- Invacare Corporation

- Ottobock

- Drive DeVilbiss Healthcare

- Sunrise Medical

- Permobil

- Karman Healthcare

- Medline Industries

- Pride Mobility Products

- Nissin Medical Industries

- GF Health Products

- Mobilis

- Van Os Medical

- Handicare

- Rehacare

- Apex Medical

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 11.1 Billion |

|

Forecasted Value (2030) |

USD 14.8 Billion |

|

CAGR (2024 – 2030) |

4.2% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Wheelchair and Components Market By Product Type (Manual Wheelchairs, Powered Wheelchairs, Sports Wheelchairs, Pediatric Wheelchairs, Standing Wheelchairs), By Component (Tires and Wheels, Frame, Upholstery, Armrests, Footrests, Batteries, Joysticks and Controllers), By End-User Industry (Hospitals, Home Care, Rehabilitation Centers, Nursing Homes) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Invacare Corporation, Ottobock, Drive DeVilbiss Healthcare, Sunrise Medical, Permobil, Karman Healthcare, Medline Industries, Pride Mobility Products, Nissin Medical Industries, GF Health Products, Mobilis, Van Os Medical, Handicare, Rehacare, Apex Medical |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Wheelchair and Components Market, by Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Manual Wheelchairs |

|

4.2. Powered Wheelchairs |

|

4.3. Sports Wheelchairs |

|

4.4. Pediatric Wheelchairs |

|

4.5. Standing Wheelchairs |

|

5. Wheelchair and Components Market, by Component (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Tires and Wheels |

|

5.2. Frame |

|

5.3. Upholstery |

|

5.4. Armrests |

|

5.5. Footrests |

|

5.6. Batteries |

|

5.7. Joysticks and Controllers |

|

6. Wheelchair and Components Market, by End User (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Hospitals |

|

6.2. Home Care |

|

6.3. Rehabilitation Centers |

|

6.4. Nursing Homes |

|

6.5. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Wheelchair and Components Market, by Type |

|

7.2.7. North America Wheelchair and Components Market, by Component |

|

7.2.8. North America Wheelchair and Components Market, by End User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Wheelchair and Components Market, by Type |

|

7.2.9.1.2. US Wheelchair and Components Market, by Component |

|

7.2.9.1.3. US Wheelchair and Components Market, by End User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Invacare Corporation |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Ottobock |

|

9.3. Drive DeVilbiss Healthcare |

|

9.4. Sunrise Medical |

|

9.5. Permobil |

|

9.6. Karman Healthcare |

|

9.7. Medline Industries |

|

9.8. Pride Mobility Products |

|

9.9. Nissin Medical Industries |

|

9.10. GF Health Products |

|

9.11. Mobilis |

|

9.12. Van Os Medical |

|

9.13. Handicare |

|

9.14. Rehacare |

|

9.15. Apex Medical |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Wheelchair and Components Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Wheelchair and Components Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Wheelchair and Components Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA