As per Intent Market Research, the Voltage Transformer Market was valued at USD 6.8 Billion in 2024-e and will surpass USD 11.2 Billion by 2030; growing at a CAGR of 8.9% during 2025-2030.

The voltage transformer market is experiencing steady growth, driven by the increasing need for efficient voltage regulation, power distribution, and electrical isolation across various industries. Voltage transformers are essential components in electrical systems, as they step up or step down the voltage to desired levels, ensuring safe and reliable energy distribution. These devices are widely used in power generation, electrical utilities, industrial automation, renewable energy systems, and residential & commercial buildings, making them crucial for the effective functioning of modern power grids and industrial applications.

As the demand for renewable energy, industrial automation, and reliable power supply systems rises, the voltage transformer market is expected to expand. Additionally, the growing focus on energy efficiency, system optimization, and grid modernization will drive further adoption of voltage transformers, particularly in power distribution and renewable energy integration applications.

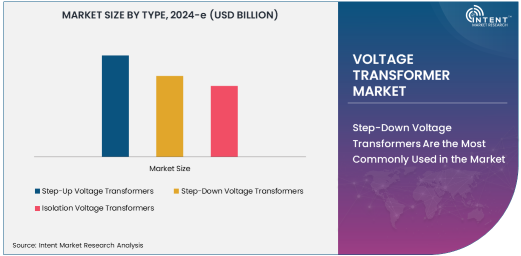

Step-Down Voltage Transformers Are the Most Commonly Used in the Market

Step-down voltage transformers dominate the market due to their widespread use in reducing high voltages to lower levels for safe use in residential, commercial, and industrial applications. These transformers are essential for providing appropriate voltage levels for electrical equipment and devices, ensuring optimal performance and safety. Step-down transformers are commonly used in power distribution networks, residential buildings, and industrial power supply systems, where voltage needs to be reduced for consumer usage.

The high demand for reliable, low-voltage systems in residential, commercial, and industrial sectors continues to drive the growth of step-down voltage transformers, making them the most commonly used type in the market.

Low Voltage Transformers Hold the Largest Market Share Due to Broad Applications in Residential and Commercial Sectors

Low voltage transformers are the largest segment in the voltage range category due to their widespread applications in residential, commercial, and light industrial sectors. These transformers are used to power appliances, lighting systems, and smaller electrical devices, making them essential for the operation of everyday electrical equipment in homes and businesses.

As the demand for energy-efficient and reliable power systems grows, low voltage transformers will continue to hold the largest market share, especially in urban areas where residential and commercial buildings require stable and safe power supply systems.

Power Generation and Electrical Utilities Are the Largest End-User Industries for Voltage Transformers

The power generation and electrical utilities sectors are the largest end-users of voltage transformers, as these industries require robust and reliable voltage regulation and power distribution systems. Voltage transformers are essential in power generation plants, where they help maintain consistent voltage levels to ensure the proper functioning of electrical systems. Similarly, electrical utilities rely on voltage transformers to manage voltage levels in power transmission and distribution networks.

With the increasing demand for renewable energy sources, voltage transformers are also being integrated into renewable energy systems, such as solar and wind power, to ensure seamless power conversion and grid integration. The growing focus on modernizing power grids and improving energy distribution efficiency will further contribute to the demand for voltage transformers in these industries.

Voltage Regulation Is the Leading Application for Voltage Transformers

Voltage regulation is the largest application for voltage transformers, as these devices are designed to maintain stable voltage levels in electrical systems, ensuring that equipment operates within safe limits. Voltage regulation is essential for preventing voltage fluctuations that could damage electrical components, reduce efficiency, or cause system failures.

In power generation, transmission, and distribution, voltage transformers play a vital role in maintaining consistent voltage levels across long distances, especially when energy is transmitted through high-voltage lines. Voltage regulation is also critical in industrial automation, renewable energy systems, and residential & commercial buildings, where voltage levels must be controlled for optimal performance.

North America and Europe Are the Leading Regions in the Voltage Transformer Market

North America and Europe dominate the voltage transformer market due to the high demand for advanced power distribution systems, renewable energy integration, and industrial automation. Both regions have well-established electrical infrastructure and significant investments in grid modernization, energy efficiency, and renewable energy projects.

In North America, the U.S. is the largest market for voltage transformers, driven by its robust power generation, transmission, and distribution infrastructure, as well as its focus on integrating renewable energy sources. Similarly, Europe is experiencing growth in the voltage transformer market due to the increasing demand for renewable energy integration, grid modernization, and energy-efficient solutions.

Competitive Landscape

The voltage transformer market is competitive, with several key players offering a range of products to meet the diverse needs of the power generation, electrical utilities, and industrial sectors. Leading companies in the market include ABB, Siemens, Schneider Electric, General Electric, and Eaton, all of which provide voltage transformers for various applications, including power regulation, distribution, and industrial power supply.

Competition in the market is driven by factors such as product performance, technological advancements, cost-efficiency, and the ability to cater to specific industry needs. As industries increasingly focus on energy efficiency, grid modernization, and renewable energy integration, players in the voltage transformer market are investing in innovative solutions that offer better performance, higher reliability, and greater adaptability to changing energy demands.

Strategic partnerships, mergers, acquisitions, and product innovations will play a critical role in shaping the competitive landscape in the voltage transformer market, as companies look to strengthen their market position and expand their offerings in the evolving energy landscape.

Recent Developments:

- In December 2024, Siemens AG launched a new range of medium-voltage transformers designed for industrial applications and smart grids.

- In November 2024, General Electric announced a strategic partnership with renewable energy companies to provide high-voltage transformers for wind and solar farms.

- In October 2024, ABB Ltd. introduced an innovative step-down transformer solution for residential buildings, enhancing energy efficiency.

- In September 2024, Schneider Electric unveiled a new isolation transformer aimed at improving power quality in sensitive industrial environments.

- In August 2024, Eaton Corporation launched a range of high-voltage transformers for use in power generation facilities

List of Leading Companies:

- Siemens AG

- General Electric Company

- Schneider Electric SE

- ABB Ltd.

- Eaton Corporation

- Mitsubishi Electric Corporation

- Toshiba Corporation

- Hitachi Ltd.

- Kirloskar Electric Company

- Emerson Electric Co.

- Fuji Electric Co., Ltd.

- CG Power and Industrial Solutions Ltd.

- SGB-Smit Group

- Weg SA

- RMG Group

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 6.8 Billion |

|

Forecasted Value (2030) |

USD 11.2 Billion |

|

CAGR (2025 – 2030) |

8.9% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Voltage Transformer Market by Type (Step-Up Voltage Transformers, Step-Down Voltage Transformers, Isolation Voltage Transformers), Voltage Range (Low Voltage Transformers, Medium Voltage Transformers, High Voltage Transformers), End-User Industry (Power Generation, Electrical Utilities, Industrial Automation, Residential & Commercial Buildings, Renewable Energy Systems), Application (Voltage Regulation, Power Distribution, Electrical Isolation, Renewable Energy Integration, Industrial Power Supply) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Siemens AG, General Electric Company, Schneider Electric SE, ABB Ltd., Eaton Corporation, Mitsubishi Electric Corporation, Toshiba Corporation, Hitachi Ltd., Kirloskar Electric Company, Emerson Electric Co., Fuji Electric Co., Ltd., CG Power and Industrial Solutions Ltd., SGB-Smit Group, Weg SA, RMG Group |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Voltage Transformer Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Step-Up Voltage Transformers |

|

4.2. Step-Down Voltage Transformers |

|

4.3. Isolation Voltage Transformers |

|

5. Voltage Transformer Market, by Voltage Range (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Low Voltage Transformers |

|

5.2. Medium Voltage Transformers |

|

5.3. High Voltage Transformers |

|

6. Voltage Transformer Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Power Generation |

|

6.2. Electrical Utilities |

|

6.3. Industrial Automation |

|

6.4. Residential & Commercial Buildings |

|

6.5. Renewable Energy Systems |

|

7. Voltage Transformer Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Voltage Regulation |

|

7.2. Power Distribution |

|

7.3. Electrical Isolation |

|

7.4. Renewable Energy Integration |

|

7.5. Industrial Power Supply |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Voltage Transformer Market, by Type |

|

8.2.7. North America Voltage Transformer Market, by Voltage Range |

|

8.2.8. North America Voltage Transformer Market, by End-User Industry |

|

8.2.9. North America Voltage Transformer Market, by Application |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Voltage Transformer Market, by Type |

|

8.2.10.1.2. US Voltage Transformer Market, by Voltage Range |

|

8.2.10.1.3. US Voltage Transformer Market, by End-User Industry |

|

8.2.10.1.4. US Voltage Transformer Market, by Application |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Siemens AG |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. General Electric Company |

|

10.3. Schneider Electric SE |

|

10.4. ABB Ltd. |

|

10.5. Eaton Corporation |

|

10.6. Mitsubishi Electric Corporation |

|

10.7. Toshiba Corporation |

|

10.8. Hitachi Ltd. |

|

10.9. Kirloskar Electric Company |

|

10.10. Emerson Electric Co. |

|

10.11. Fuji Electric Co., Ltd. |

|

10.12. CG Power and Industrial Solutions Ltd. |

|

10.13. SGB-Smit Group |

|

10.14. Weg SA |

|

10.15. RMG Group |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Voltage Transformer Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Voltage Transformer Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Voltage Transformer Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA