As per Intent Market Research, the Input was valued at USD 1.3 Billion in 2024-e and will surpass USD 2.2 Billion by 2030; growing at a CAGR of 9.0% during 2025-2030.

The Voltage Detection System market is growing rapidly, driven by increasing safety concerns and the need for efficient power management across various sectors. These systems play a crucial role in detecting voltage presence or absence, ensuring safe electrical operations in utilities, industrial plants, and residential settings. With advancements in technology and the growing adoption of smart electrical systems, the market is witnessing an upward trend.

The demand for voltage detection systems is bolstered by stringent regulations regarding electrical safety, the rise of renewable energy systems, and the need to modernize aging electrical infrastructure. Innovations in wireless and portable voltage detection technologies are also contributing to the market's growth by offering more flexibility and ease of use for end-users across diverse applications.

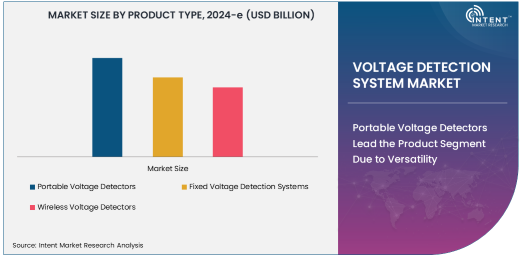

Portable Voltage Detectors Lead the Product Segment Due to Versatility

Portable voltage detectors dominate the product segment due to their versatility, ease of use, and affordability. These devices are widely used by electricians, maintenance personnel, and utility workers for quick and reliable voltage detection. Portable detectors are particularly valued for their compact design, enabling easy transportation and on-the-spot voltage testing in various settings.

The widespread adoption of portable voltage detectors in industrial, commercial, and residential applications is driving growth in this segment. Continuous technological improvements, such as enhanced sensitivity and ergonomic designs, are expected to sustain their dominance in the market.

Capacitive Voltage Detection is the Leading Technology Due to High Accuracy

Capacitive voltage detection is the most commonly used technology in the market due to its high accuracy and non-contact operation. This technology is widely employed in portable and fixed voltage detection systems, offering reliable performance across low, medium, and high voltage ranges. Its ability to detect voltage without direct contact with live wires makes it a safer choice for users in utilities, industrial plants, and residential applications.

The increasing focus on electrical safety and the need for advanced detection capabilities are driving the adoption of capacitive voltage detection technology. Innovations in this field, such as improved sensitivity and integration with IoT-enabled systems, are expected to further enhance its market position.

High Voltage Detection Systems Hold Significant Market Share Due to Utilities and Industrial Demand

High voltage detection systems account for a significant share of the market, driven by their critical role in ensuring safety and efficiency in utilities and industrial operations. These systems are essential for maintaining the safety of personnel working on high-voltage lines, substations, and equipment.

As the demand for electricity continues to rise globally, and as utilities modernize their infrastructure, the need for reliable high-voltage detection systems is expected to grow. Furthermore, the integration of renewable energy sources into power grids is driving additional demand for high voltage detection systems to ensure safe and seamless operations.

Utilities Lead the End-User Industry Segment Due to Extensive Usage

The utilities sector is the largest end-user of voltage detection systems, as these devices are essential for ensuring the safety and reliability of power distribution networks. Utilities rely on voltage detection systems to identify faults, prevent accidents, and maintain uninterrupted power supply.

With the increasing adoption of smart grid technologies and the integration of renewable energy sources, utilities are investing in advanced voltage detection systems to enhance monitoring and control capabilities. The industrial sector also represents a significant share of the market, driven by the need for voltage detection systems in manufacturing plants, oil & gas facilities, and other industrial operations.

Direct Sales Dominate the Distribution Channel Segment

Direct sales dominate the distribution channel segment, as manufacturers prioritize direct engagement with utilities, industrial customers, and large-scale projects. This approach allows manufacturers to offer customized solutions, provide technical support, and build strong customer relationships.

However, online retailers and distributors are gaining traction, especially for portable and residential voltage detection devices. The convenience of online purchasing, coupled with the availability of a wide range of products, is driving growth in this channel, particularly in residential and small-scale industrial applications.

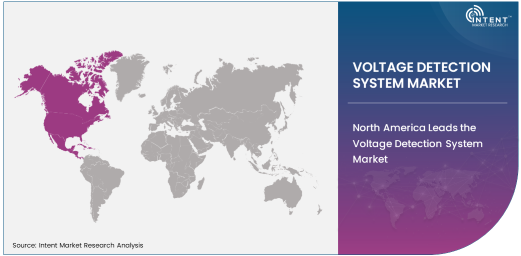

North America Leads the Voltage Detection System Market

North America holds the largest share of the voltage detection system market, driven by the region's advanced utility infrastructure, stringent safety regulations, and high adoption of smart grid technologies. The U.S., in particular, is a major market for voltage detection systems due to ongoing investments in electrical grid modernization and the integration of renewable energy sources.

The Asia-Pacific region is emerging as a high-growth market, fueled by rapid industrialization, urbanization, and increasing energy demands in countries like China, India, and Japan. Expanding infrastructure projects and growing awareness about electrical safety are further driving demand in the region.

Competitive Landscape

The voltage detection system market is highly competitive, with numerous global and regional players offering a wide range of products. Key players focus on innovation, technological advancements, and strategic partnerships to strengthen their market presence. Companies such as Fluke Corporation, Schneider Electric, ABB, and Eaton are investing in research and development to introduce advanced detection systems with enhanced safety features and IoT integration.

The market is also witnessing the entry of new players, particularly in the wireless and portable voltage detection segments, where demand is rapidly growing. Strategic collaborations between manufacturers and utility companies are shaping the competitive landscape, ensuring the development of tailored solutions for diverse applications. As the market evolves, the ability to offer reliable, cost-effective, and technologically advanced products will be crucial for sustaining a competitive edge.

Recent Developments:

- In December 2024, ABB Ltd. launched a new wireless voltage detection system with enhanced range and accuracy.

- In November 2024, Siemens AG introduced a smart voltage detection device integrated with IoT capabilities for real-time monitoring.

- In October 2024, Fluke Corporation unveiled a portable voltage detector designed for high-voltage utility applications.

- In September 2024, Schneider Electric announced the development of a fixed voltage detection system for industrial safety compliance.

- In August 2024, Honeywell International Inc. expanded its product portfolio with a capacitive voltage detector for residential and commercial use.

List of Leading Companies:

- ABB Ltd.

- General Electric Company

- Schneider Electric SE

- Siemens AG

- Eaton Corporation

- Fluke Corporation

- Megger Group Limited

- Hioki E.E. Corporation

- SebaKMT

- Honeywell International Inc.

- Kyoritsu Electric India Pvt. Ltd.

- Amprobe

- Chauvin Arnoux

- OMICRON Electronics GmbH

- Doble Engineering Company

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.3 Billion |

|

Forecasted Value (2030) |

USD 2.2 Billion |

|

CAGR (2025 – 2030) |

9.0% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Voltage Detection System Market by Product Type (Portable Voltage Detectors, Fixed Voltage Detection Systems, Wireless Voltage Detectors), Technology (Capacitive Voltage Detection, Resistive Voltage Detection, Inductive Voltage Detection), Voltage Range (Low Voltage, Medium Voltage, High Voltage), End-User Industry (Utilities, Industrial, Commercial, Residential), Distribution Channel (Direct Sales, Online Retailers, Distributors) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

ABB Ltd., General Electric Company, Schneider Electric SE, Siemens AG, Eaton Corporation, Fluke Corporation, Megger Group Limited, Hioki E.E. Corporation, SebaKMT, Honeywell International Inc., Kyoritsu Electric India Pvt. Ltd., Amprobe, Chauvin Arnoux, OMICRON Electronics GmbH, Doble Engineering Company |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Voltage Detection System Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Portable Voltage Detectors |

|

4.2. Fixed Voltage Detection Systems |

|

4.3. Wireless Voltage Detectors |

|

5. Voltage Detection System Market, by Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Capacitive Voltage Detection |

|

5.2. Resistive Voltage Detection |

|

5.3. Inductive Voltage Detection |

|

6. Voltage Detection System Market, by Voltage Range (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Low Voltage |

|

6.2. Medium Voltage |

|

6.3. High Voltage |

|

7. Voltage Detection System Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Utilities |

|

7.2. Industrial |

|

7.3. Commercial |

|

7.4. Residential |

|

8. Voltage Detection System Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Direct Sales |

|

8.2. Online Retailers |

|

8.3. Distributors |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Voltage Detection System Market, by Product Type |

|

9.2.7. North America Voltage Detection System Market, by Technology |

|

9.2.8. North America Voltage Detection System Market, by Voltage Range |

|

9.2.9. North America Voltage Detection System Market, by End-User Industry |

|

9.2.10. North America Voltage Detection System Market, by Distribution Channel |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Voltage Detection System Market, by Product Type |

|

9.2.11.1.2. US Voltage Detection System Market, by Technology |

|

9.2.11.1.3. US Voltage Detection System Market, by Voltage Range |

|

9.2.11.1.4. US Voltage Detection System Market, by End-User Industry |

|

9.2.11.1.5. US Voltage Detection System Market, by Distribution Channel |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. ABB Ltd. |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. General Electric Company |

|

11.3. Schneider Electric SE |

|

11.4. Siemens AG |

|

11.5. Eaton Corporation |

|

11.6. Fluke Corporation |

|

11.7. Megger Group Limited |

|

11.8. Hioki E.E. Corporation |

|

11.9. SebaKMT |

|

11.10. Honeywell International Inc. |

|

11.11. Kyoritsu Electric India Pvt. Ltd. |

|

11.12. Amprobe |

|

11.13. Chauvin Arnoux |

|

11.14. OMICRON Electronics GmbH |

|

11.15. Doble Engineering Company |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Voltage Detection System Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Voltage Detection System Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Voltage Detection System Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA