As per Intent Market Research, the Vision Impairment Market was valued at USD 11.6 billion in 2024-e and will surpass USD 17.0 billion by 2030; growing at a CAGR of 6.6% during 2025 - 2030.

The vision impairment market is witnessing substantial growth, driven by the increasing global prevalence of eye disorders such as nearsightedness (myopia), farsightedness (hyperopia), astigmatism, and age-related conditions like presbyopia. The market is also being influenced by rising awareness about the importance of eye health, advancements in treatment options, and an aging global population. As the demand for both corrective and therapeutic treatments continues to rise, there is a greater focus on improving vision correction technologies and innovative solutions for eye health management. From corrective lenses to advanced surgeries and retinal treatments, the market is evolving to address a wide range of vision impairments across diverse age groups.

The growing incidence of conditions such as myopia, diabetic retinopathy, and cataracts is also fueling the demand for specialized treatments. Furthermore, technological advancements in surgical treatments, including laser procedures and cataract surgery, are driving market growth. The market is also expanding due to the increased adoption of advanced diagnostic tools in ophthalmic clinics and rehabilitation centers. As awareness about early intervention and preventive care grows, more people are seeking professional treatments, contributing to the overall growth of the market.

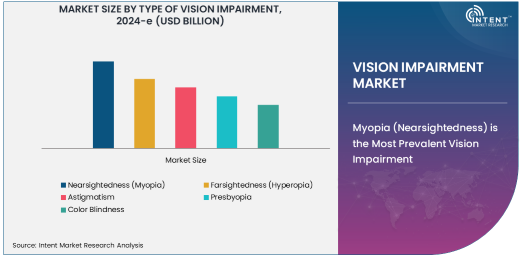

Myopia (Nearsightedness) is the Most Prevalent Vision Impairment

Nearsightedness (Myopia) is the largest segment in the vision impairment market due to its high prevalence worldwide. Myopia, which occurs when the eye is unable to focus on distant objects, is becoming increasingly common, particularly among children and young adults. This condition is largely attributed to lifestyle changes, such as increased screen time and a shift towards more indoor activities, which are associated with the rise in myopia cases. As a result, the demand for corrective treatments like eyeglasses, contact lenses, and refractive surgeries is rapidly increasing.

In response to the growing prevalence of myopia, new treatment options have emerged, including advanced laser surgeries like LASIK and PRK, which offer long-term solutions for vision correction. Additionally, the availability of myopia management therapies, such as specialized contact lenses and atropine eye drops, further boosts the demand for treatments in this segment. With the rising global burden of myopia, particularly in regions with a high proportion of young populations, this segment is expected to continue dominating the vision impairment market in the coming years.

Corrective Lenses Segment is the Largest Treatment Type Due to Widespread Usage

The corrective lenses segment is the largest within the treatment type category in the vision impairment market, owing to the widespread use of eyeglasses and contact lenses as the primary method for correcting refractive errors like myopia, hyperopia, and astigmatism. Eyeglasses are the most common and accessible solution for vision correction, with a vast number of individuals worldwide relying on them to improve their vision. Contact lenses, which offer greater convenience and aesthetic appeal, have also seen a rise in popularity, particularly among younger populations and individuals involved in active lifestyles.

Corrective lenses remain the go-to treatment for many individuals due to their simplicity, affordability, and ease of access. This treatment type has seen continuous innovation, with the development of specialized lenses, such as multifocal lenses for presbyopia and ortho-k lenses for myopia management. As the demand for vision correction rises with the global aging population and the increasing prevalence of refractive errors, the corrective lenses segment is poised for sustained growth, with ongoing improvements in design and material technology ensuring better comfort and vision quality.

Cataract Surgery is the Fastest Growing Treatment Segment

Cataract surgery is the fastest growing treatment segment in the vision impairment market, driven by the increasing global aging population. Cataracts, a condition where the eye's natural lens becomes cloudy and impairs vision, are highly prevalent in elderly individuals. As the global population ages, the number of people affected by cataracts is growing, leading to a higher demand for cataract surgery as the primary treatment option. Cataract surgery is a highly effective procedure, with millions of surgeries performed annually, offering significant improvements in vision and quality of life.

The growth of this segment is also supported by advancements in surgical techniques, such as the use of femtosecond lasers and intraocular lenses (IOLs), which enhance the precision, safety, and outcomes of cataract surgery. These innovations have made cataract surgery more accessible and less invasive, further fueling its adoption. With the increasing number of elderly individuals worldwide and the continuous improvements in surgical methods, cataract surgery is expected to remain a key driver of growth in the vision impairment market.

Pediatric Vision Impairment is a Key Application Area Due to Growing Awareness

Pediatric vision impairment is a significant application area in the vision impairment market, driven by rising awareness about the importance of early detection and treatment of vision problems in children. Conditions like nearsightedness, farsightedness, and astigmatism can have a profound impact on a child's development, education, and overall quality of life. Early intervention and corrective treatments can help prevent long-term complications and improve visual outcomes. As awareness increases among parents, schools, and healthcare providers, more children are being diagnosed and treated for vision impairment at an earlier age.

The increasing availability of pediatric-specific corrective lenses and advanced diagnostic tools, such as digital retinoscopy, has also contributed to the growth of this segment. Additionally, the rise in digital screen usage among children has led to an increased focus on myopia control, which is driving demand for specialized lenses and treatment options. As a result, pediatric vision impairment continues to be a key focus area for both healthcare professionals and manufacturers of vision correction products, ensuring steady growth in this segment.

Hospitals Segment is the Largest End-Use Industry Due to Comprehensive Treatment Services

The hospitals segment is the largest end-use industry in the vision impairment market, owing to hospitals' ability to provide comprehensive treatment for a wide range of vision impairments. Hospitals are equipped with advanced diagnostic tools, surgical facilities, and a team of ophthalmologists and optometrists who can treat patients with varying degrees of vision impairment. They offer a broad spectrum of services, including cataract surgery, retinal treatments, and specialized treatments for conditions like diabetic retinopathy and glaucoma.

Additionally, hospitals often serve as the primary destination for more complex treatments, such as surgical interventions for vision correction or retinal disorders. The growth of the hospital segment is also supported by the increasing prevalence of vision-related diseases, the aging population, and technological advancements in ophthalmic care. Hospitals remain a crucial component of the healthcare system, offering both preventative care and advanced treatment options for individuals with vision impairments.

North America is the Largest Region Due to Advanced Healthcare Infrastructure

North America is the largest region in the vision impairment market, primarily due to its advanced healthcare infrastructure, high healthcare spending, and the presence of leading healthcare providers and research institutions. The United States, in particular, has a large aging population that is increasingly affected by age-related vision impairments like cataracts and presbyopia, contributing to the demand for advanced treatments. Additionally, the growing awareness of eye health, along with the availability of cutting-edge diagnostic tools and treatments, makes North America the dominant market for vision impairment solutions.

The region also benefits from the high adoption of corrective lenses and surgical treatments, with access to a wide range of advanced vision care options. Moreover, the rising prevalence of conditions like diabetic retinopathy, which requires specialized retinal treatments, further contributes to the growth of the vision impairment market in North America. As the demand for both preventive and corrective treatments continues to rise, North America is expected to maintain its position as the largest regional market for vision impairment.

Competitive Landscape

The vision impairment market is highly competitive, with several key players involved in the development and distribution of corrective lenses, surgical treatments, and advanced retinal therapies. Prominent companies include EssilorLuxottica, Alcon, Johnson & Johnson Vision, Bausch & Lomb, and Carl Zeiss Vision. These companies are focusing on expanding their product offerings, improving treatment efficacy, and enhancing patient outcomes through innovative technologies.

Additionally, many players are investing in research and development to introduce new treatment options, such as advanced cataract surgery technologies, myopia control solutions, and gene therapies for retinal diseases. As the market grows, competition will intensify, with companies striving to improve the quality of care, reduce treatment costs, and increase accessibility to vision impairment treatments. Strategic partnerships, mergers, and acquisitions are also common as companies seek to expand their reach and consolidate their market positions.

Recent Developments:

- EssilorLuxottica launched an advanced line of smart glasses with built-in vision correction, targeting both corrective and convenience uses for vision-impaired individuals.

- Alcon Laboratories received approval for its innovative cataract surgery technology, improving recovery times and outcomes for patients with advanced cataracts.

- Johnson & Johnson Vision expanded its range of contact lenses, introducing a new lens designed specifically for individuals with presbyopia, enhancing comfort and clarity.

- Bausch + Lomb entered into a partnership with a tech company to develop digital tools for early detection and treatment of age-related macular degeneration.

- Novartis AG announced the launch of a new drug aimed at treating diabetic retinopathy, promising improved outcomes for patients with diabetic eye conditions.

List of Leading Companies:

- EssilorLuxottica

- Johnson & Johnson Vision

- Novartis AG

- Abbott Laboratories

- Alcon Laboratories, Inc.

- CooperVision, Inc.

- Bausch + Lomb

- Carl Zeiss AG

- Hoya Corporation

- Fielmann AG

- Ray-Ban

- Spectacle Hut

- Luxottica Group S.p.A.

- Visibly, Inc.

- Topcon Corporation

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 11.6 Billion |

|

Forecasted Value (2030) |

USD 17.0 Billion |

|

CAGR (2025 – 2030) |

6.6% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Global Vision Impairment Market by Type of Vision Impairment (Nearsightedness (Myopia), Farsightedness (Hyperopia), Astigmatism, Presbyopia, Color Blindness), by Treatment Type (Corrective Lenses, Surgical Treatments, Cataract Surgery, Retinal Treatments), by Application (Pediatric Vision Impairment, Geriatric Vision Impairment, Diabetic Retinopathy), by End-Use Industry (Hospitals, Ophthalmic Clinics, Rehabilitation Centers) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

EssilorLuxottica, Johnson & Johnson Vision, Novartis AG, Abbott Laboratories, Alcon Laboratories, Inc., CooperVision, Inc., Carl Zeiss AG, Hoya Corporation, Fielmann AG, Ray-Ban, Spectacle Hut, Luxottica Group S.p.A. and Topcon Corporation |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Vision Impairment Market, by Type of Vision Impairment (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Nearsightedness (Myopia) |

|

4.2. Farsightedness (Hyperopia) |

|

4.3. Astigmatism |

|

4.4. Presbyopia |

|

4.5. Color Blindness |

|

5. Vision Impairment Market, by Treatment Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Corrective Lenses |

|

5.2. Surgical Treatments |

|

5.3. Cataract Surgery |

|

5.4. Retinal Treatments |

|

6. Vision Impairment Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Pediatric Vision Impairment |

|

6.2. Geriatric Vision Impairment |

|

6.3. Diabetic Retinopathy |

|

6.4. Others |

|

7. Vision Impairment Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Hospitals |

|

7.2. Ophthalmic Clinics |

|

7.3. Rehabilitation Centers |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Vision Impairment Market, by Type of Vision Impairment |

|

8.2.7. North America Vision Impairment Market, by Treatment Type |

|

8.2.8. North America Vision Impairment Market, by Application |

|

8.2.9. North America Vision Impairment Market, by End-Use Industry |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Vision Impairment Market, by Type of Vision Impairment |

|

8.2.10.1.2. US Vision Impairment Market, by Treatment Type |

|

8.2.10.1.3. US Vision Impairment Market, by Application |

|

8.2.10.1.4. US Vision Impairment Market, by End-Use Industry |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. EssilorLuxottica |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Johnson & Johnson Vision |

|

10.3. Novartis AG |

|

10.4. Abbott Laboratories |

|

10.5. Alcon Laboratories, Inc. |

|

10.6. CooperVision, Inc. |

|

10.7. Bausch + Lomb |

|

10.8. Carl Zeiss AG |

|

10.9. Hoya Corporation |

|

10.10. Fielmann AG |

|

10.11. Ray-Ban |

|

10.12. Spectacle Hut |

|

10.13. Luxottica Group S.p.A. |

|

10.14. Visibly, Inc. |

|

10.15. Topcon Corporation |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Vision Impairment Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Vision Impairment Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Vision Impairment Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA