As per Intent Market Research, the Veterinary Dermatology Drugs Market was valued at USD 1.8 Billion in 2024-e and will surpass USD 3.1 Billion by 2030; growing at a CAGR of 9.3% during 2025-2030.

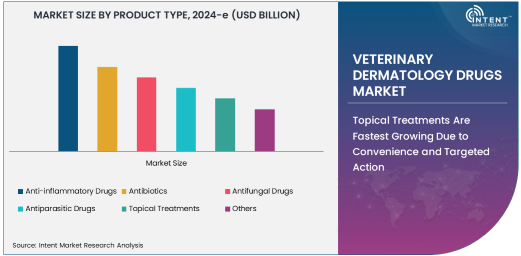

The veterinary dermatology drugs market is a vital segment of the overall veterinary healthcare market, providing treatments for a wide range of skin disorders in animals. Among the various product types, anti-inflammatory drugs are the largest category due to their essential role in managing conditions such as dermatitis, eczema, and other inflammatory skin diseases. These medications help reduce inflammation, pain, and discomfort, promoting faster recovery for animals suffering from allergic reactions, infections, or other dermatological issues.

Anti-inflammatory drugs, such as corticosteroids and non-steroidal anti-inflammatory drugs (NSAIDs), are commonly prescribed by veterinarians for treating various dermatological conditions in companion animals, including dogs and cats. Their ability to effectively reduce inflammation and control symptoms has led to their widespread use, making them a key driver of growth in the veterinary dermatology drugs market. As the prevalence of skin disorders in pets continues to rise, the demand for anti-inflammatory drugs is expected to maintain its dominant position in the market.

Topical Treatments Are Fastest Growing Due to Convenience and Targeted Action

Topical treatments are the fastest-growing product type in the veterinary dermatology drugs market, driven by their convenience, ease of application, and targeted action. These treatments, which include creams, ointments, and sprays, are particularly effective for localized skin conditions, such as wounds, burns, fungal infections, and hotspots in companion animals. Topical treatments are preferred because they directly target the affected areas, minimizing the risk of systemic side effects.

Advancements in topical formulations, such as improved delivery systems and the inclusion of healing agents like aloe vera or antimicrobial compounds, have also contributed to their rapid growth. With rising awareness among pet owners about the effectiveness of topical solutions for managing dermatological issues, this segment is expected to continue expanding. As more veterinarians recommend topical treatments for common skin ailments in pets, the demand for these products is likely to increase.

Companion Animals Are Largest Animal Type Due to High Incidence of Skin Disorders

Companion animals, especially dogs and cats, represent the largest animal type segment in the veterinary dermatology drugs market. These animals are particularly prone to a wide variety of skin conditions, ranging from allergies to infections, making them the primary beneficiaries of dermatological treatments. The increasing incidence of skin disorders, such as atopic dermatitis, flea allergy dermatitis, and bacterial infections, has led to a greater demand for veterinary dermatology drugs in this segment.

Companion animals also benefit from increased attention to their healthcare needs, as pet owners are becoming more proactive in seeking treatments for their pets' skin issues. The growing humanization of pets and the willingness of owners to invest in specialized care further contribute to the demand for veterinary dermatology drugs. As the pet population grows and the awareness of skin conditions in pets rises, the companion animal segment is expected to continue dominating the market.

Veterinary Clinics Are Largest End-User Due to Frequent Visits for Dermatological Concerns

Veterinary clinics are the largest end-user segment in the veterinary dermatology drugs market due to their accessibility and the frequency with which pet owners visit for dermatological concerns. These clinics are often the first point of contact for pet owners seeking treatment for their animals' skin conditions. Veterinary clinics are equipped to diagnose and treat a wide variety of skin diseases, from common allergies to more serious infections, and they provide the necessary medications, including anti-inflammatory drugs, antibiotics, antifungal treatments, and topical solutions.

The increasing number of pet owners seeking professional treatment for dermatological conditions further supports the growth of veterinary clinics as a primary end-user of these drugs. As dermatology is a frequently requested service at veterinary clinics, this segment is expected to continue growing in response to the rising demand for specialized skin care for pets.

Oral Administration Is Largest Route of Administration Due to Ease of Use for Pet Owners

Oral administration is the largest route of administration in the veterinary dermatology drugs market, as it is one of the most convenient methods for both veterinarians and pet owners. Oral drugs are typically used to treat systemic conditions, such as infections, allergies, and inflammatory disorders, and they are easy to administer, particularly in companion animals. Oral medications, such as tablets and capsules, allow for straightforward dosing, which contributes to their widespread use.

The growing availability of flavored oral medications, which improve compliance in pets, has further enhanced the popularity of oral administration. Oral drugs are also effective for managing chronic skin conditions, such as atopic dermatitis, that require long-term treatment. As the focus on convenience and ease of administration remains a priority, oral administration is expected to maintain its dominance in the veterinary dermatology drugs market.

North America Is Largest Region Due to Advanced Veterinary Care and High Pet Ownership

North America is the largest region in the veterinary dermatology drugs market, driven by advanced veterinary care standards, high levels of pet ownership, and a strong focus on pet health and well-being. The United States, in particular, is a leading market due to the prevalence of skin conditions in pets, the availability of specialized veterinary dermatology services, and the high demand for effective treatments.

Pet owners in North America are increasingly willing to invest in veterinary care, including dermatological treatments, which has led to the growth of the market. Additionally, the region benefits from a strong regulatory framework for veterinary pharmaceuticals, ensuring the availability of safe and effective products. With the continued focus on pet healthcare and increasing awareness of dermatological issues, North America is expected to remain the largest market for veterinary dermatology drugs.

Leading Companies and Competitive Landscape

The veterinary dermatology drugs market is highly competitive, with key players such as Zoetis, Merck Animal Health, Elanco, Boehringer Ingelheim, and Bayer Animal Health leading the industry. These companies focus on developing innovative dermatological drugs, including anti-inflammatory medications, antibiotics, antifungal treatments, and topical solutions, to address the growing need for effective skin care in animals.

The competitive landscape is characterized by continuous research and development efforts, aimed at creating new treatments that are more effective, safe, and easy to administer. Companies are also expanding their portfolios to include a broader range of dermatological treatments for both companion animals and livestock. As the veterinary dermatology drugs market continues to evolve, innovation, along with strategic collaborations with veterinary clinics and hospitals, will drive the growth of leading companies in the sector.

Recent Developments:

- Zoetis Inc. launched a new topical dermatology product for treating allergic skin diseases in dogs.

- Boehringer Ingelheim Animal Health introduced a new oral treatment for managing canine atopic dermatitis.

- Merck Animal Health expanded its dermatology portfolio with a new antifungal treatment for horses.

- Virbac S.A. developed an injectable anti-inflammatory drug specifically for livestock dermatology issues.

- Vetoquinol S.A. launched a new line of dermatology products designed for small animal clinics focusing on skin infections

List of Leading Companies:

- Zoetis Inc.

- Merck Animal Health

- Bayer Animal Health

- Boehringer Ingelheim Animal Health

- Elanco Animal Health

- Virbac S.A.

- Vetoquinol S.A.

- IDEXX Laboratories, Inc.

- Dechra Pharmaceuticals PLC

- Ceva Santé Animale

- PetIQ, Inc.

- Aratana Therapeutics

- VetriScience Laboratories

- Astellas Pharma Inc.

- Innovacyn, Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.8 Billion |

|

Forecasted Value (2030) |

USD 3.1 Billion |

|

CAGR (2025 – 2030) |

9.3% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Veterinary Dermatology Drugs Market By Product Type (Anti-inflammatory Drugs, Antibiotics, Antifungal Drugs, Antiparasitic Drugs, Topical Treatments), By Animal Type (Companion Animals, Livestock, Equine), By End-User (Veterinary Clinics, Veterinary Hospitals, Research Institutions, Pet Care Centers), and By Route of Administration (Oral, Topical, Injectable) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Zoetis Inc., Merck Animal Health, Bayer Animal Health, Boehringer Ingelheim Animal Health, Elanco Animal Health, Virbac S.A., Vetoquinol S.A., IDEXX Laboratories, Inc., Dechra Pharmaceuticals PLC, Ceva Santé Animale, PetIQ, Inc., Aratana Therapeutics, VetriScience Laboratories, Astellas Pharma Inc., Innovacyn, Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Veterinary Dermatology Drugs Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Anti-inflammatory Drugs |

|

4.2. Antibiotics |

|

4.3. Antifungal Drugs |

|

4.4. Antiparasitic Drugs |

|

4.5. Topical Treatments |

|

4.6. Others |

|

5. Veterinary Dermatology Drugs Market, by Animal Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Companion Animals |

|

5.2. Livestock |

|

5.3. Equine |

|

5.4. Others |

|

6. Veterinary Dermatology Drugs Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Veterinary Clinics |

|

6.2. Veterinary Hospitals |

|

6.3. Research Institutions |

|

6.4. Pet Care Centers |

|

6.5. Others |

|

7. Veterinary Dermatology Drugs Market, by Route of Administration (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Oral |

|

7.2. Topical |

|

7.3. Injectable |

|

7.4. Others |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Veterinary Dermatology Drugs Market, by Product Type |

|

8.2.7. North America Veterinary Dermatology Drugs Market, by Animal Type |

|

8.2.8. North America Veterinary Dermatology Drugs Market, by End-User |

|

8.2.9. North America Veterinary Dermatology Drugs Market, by Route of Administration |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Veterinary Dermatology Drugs Market, by Product Type |

|

8.2.10.1.2. US Veterinary Dermatology Drugs Market, by Animal Type |

|

8.2.10.1.3. US Veterinary Dermatology Drugs Market, by End-User |

|

8.2.10.1.4. US Veterinary Dermatology Drugs Market, by Route of Administration |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Zoetis Inc. |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Merck Animal Health |

|

10.3. Bayer Animal Health |

|

10.4. Boehringer Ingelheim Animal Health |

|

10.5. Elanco Animal Health |

|

10.6. Virbac S.A. |

|

10.7. Vetoquinol S.A. |

|

10.8. IDEXX Laboratories, Inc. |

|

10.9. Dechra Pharmaceuticals PLC |

|

10.10. Ceva Santé Animale |

|

10.11. PetIQ, Inc. |

|

10.12. Aratana Therapeutics |

|

10.13. VetriScience Laboratories |

|

10.14. Astellas Pharma Inc. |

|

10.15. Innovacyn, Inc. |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Veterinary Dermatology Drugs Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Veterinary Dermatology Drugs Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Veterinary Dermatology Drugs Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA