As per Intent Market Research, the Vehicle Control Unit Market was valued at USD 5.3 billion in 2023 and will surpass USD 12.1 billion by 2030; growing at a CAGR of 12.6% during 2024 - 2030.

The Vehicle Control Unit (VCU) market is a pivotal segment within the automotive industry, playing a crucial role in managing various vehicle functions such as engine control, safety features, and performance enhancements. As vehicles evolve towards greater automation and connectivity, the demand for advanced VCU systems is expected to surge. The market is driven by the increasing need for sophisticated vehicle management systems, rising consumer expectations for safety and comfort, and stringent regulations aimed at reducing emissions and enhancing vehicle efficiency.

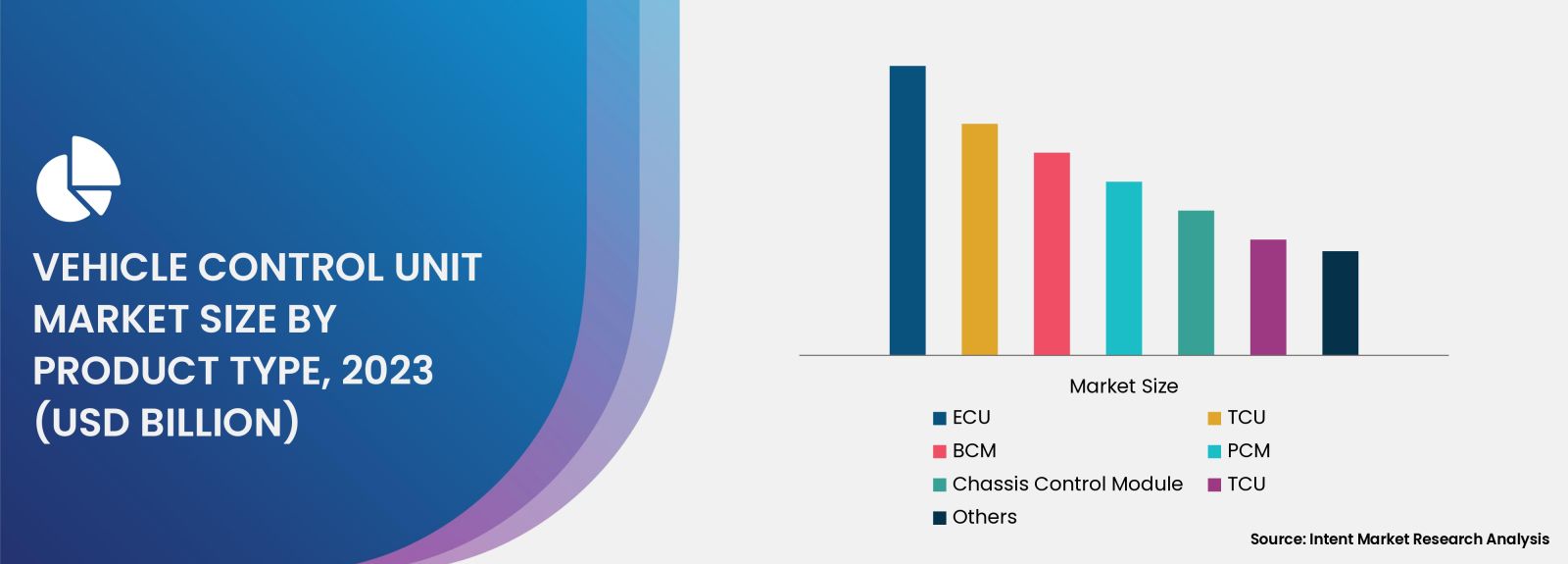

Powertrain Control Unit Segment is Largest Owing to Its Essential Role in Engine Efficiency

The Powertrain Control Unit (PCU) is the largest subsegment of the Vehicle Control Unit market, primarily due to its fundamental role in optimizing engine performance and fuel efficiency. The increasing focus on reducing carbon emissions and enhancing fuel economy is driving the adoption of sophisticated powertrain systems. PCUs manage various parameters such as air-fuel mixture, ignition timing, and exhaust gas recirculation, thereby significantly influencing the overall performance of internal combustion engines. As automotive manufacturers integrate more advanced technologies into their vehicles, the demand for PCUs will continue to grow, reinforcing their dominance in the VCU market.

Additionally, the shift towards hybrid and electric vehicles is propelling the growth of the PCU segment. These vehicles require highly efficient power management systems to ensure optimal performance and battery life. With advancements in technologies such as dual-clutch transmissions and variable valve timing, PCUs are becoming increasingly complex and capable of delivering superior performance. Consequently, this subsegment is expected to maintain its leading position, accounting for a significant share of the overall Vehicle Control Unit market.

Body Control Module Segment is Fastest Growing Owing to Enhanced Vehicle Comfort Features

The Body Control Module (BCM) segment is the fastest-growing component within the Vehicle Control Unit market, driven by the rising demand for enhanced vehicle comfort and convenience features. BCMs oversee a range of functionalities, including lighting control, window operation, and climate control, which significantly improve the driving experience. As consumers increasingly prioritize comfort and convenience, automotive manufacturers are integrating advanced BCMs into their vehicles, thereby fueling market growth.

Furthermore, the proliferation of connected vehicles and smart technology is contributing to the rapid expansion of the BCM segment. With the advent of features such as keyless entry, automatic lighting, and personalized settings, BCMs are evolving into essential components that enhance the overall user experience. The integration of Internet of Things (IoT) technology into BCMs is expected to further accelerate growth, as these systems become more sophisticated and capable of communicating with other vehicle systems. This trend positions the BCM segment for substantial growth in the coming years.

Advanced Driver Assistance Systems Segment is Largest Owing to Growing Safety Regulations

The Advanced Driver Assistance Systems (ADAS) segment is the largest subsegment in the Vehicle Control Unit market, largely driven by increasing consumer demand for enhanced safety features and stringent government regulations. ADAS technologies such as lane departure warning, adaptive cruise control, and automatic emergency braking are becoming standard in new vehicle models. As a result, automotive manufacturers are investing heavily in integrating these systems, thus expanding the ADAS market and, consequently, the VCU market.

The rising number of road accidents and fatalities has prompted governments worldwide to implement stricter safety regulations, which further propels the growth of the ADAS segment. With advancements in sensor technologies and machine learning algorithms, ADAS systems are becoming increasingly sophisticated, capable of making real-time decisions to improve road safety. As this trend continues, the ADAS segment is expected to remain a significant contributor to the overall Vehicle Control Unit market.

Electric Power Steering Segment is Fastest Growing Owing to Electrification Trends

The Electric Power Steering (EPS) segment is the fastest-growing area within the Vehicle Control Unit market, driven by the ongoing electrification of vehicles. EPS systems offer significant advantages over traditional hydraulic steering, including improved fuel efficiency, reduced weight, and enhanced vehicle performance. As electric vehicles (EVs) gain traction in the automotive landscape, the demand for EPS systems is expected to soar, positioning this segment for rapid growth.

Moreover, advancements in EPS technology, such as integration with ADAS features and enhanced driver feedback, are further contributing to its appeal. As consumers increasingly prefer vehicles equipped with advanced steering technologies, automotive manufacturers are compelled to adopt EPS systems to meet market expectations. This growing trend towards electrification is set to propel the EPS segment to new heights in the Vehicle Control Unit market.

Central Gateway Module Segment is Largest Owing to Vehicle Connectivity

The Central Gateway Module (CGM) segment is the largest within the Vehicle Control Unit market, primarily due to its critical role in facilitating communication between various vehicle systems. As vehicles become increasingly connected, the need for a centralized communication hub is paramount. CGMs manage data exchange between subsystems, ensuring seamless operation and enhancing overall vehicle functionality.

The rise of connected vehicles, equipped with advanced telematics and infotainment systems, has bolstered the demand for CGMs. These modules enable real-time data sharing, enhancing user experiences and allowing for features such as remote diagnostics and over-the-air updates. As automotive technology continues to advance, the CGM segment is expected to maintain its leading position, driving significant growth in the Vehicle Control Unit market.

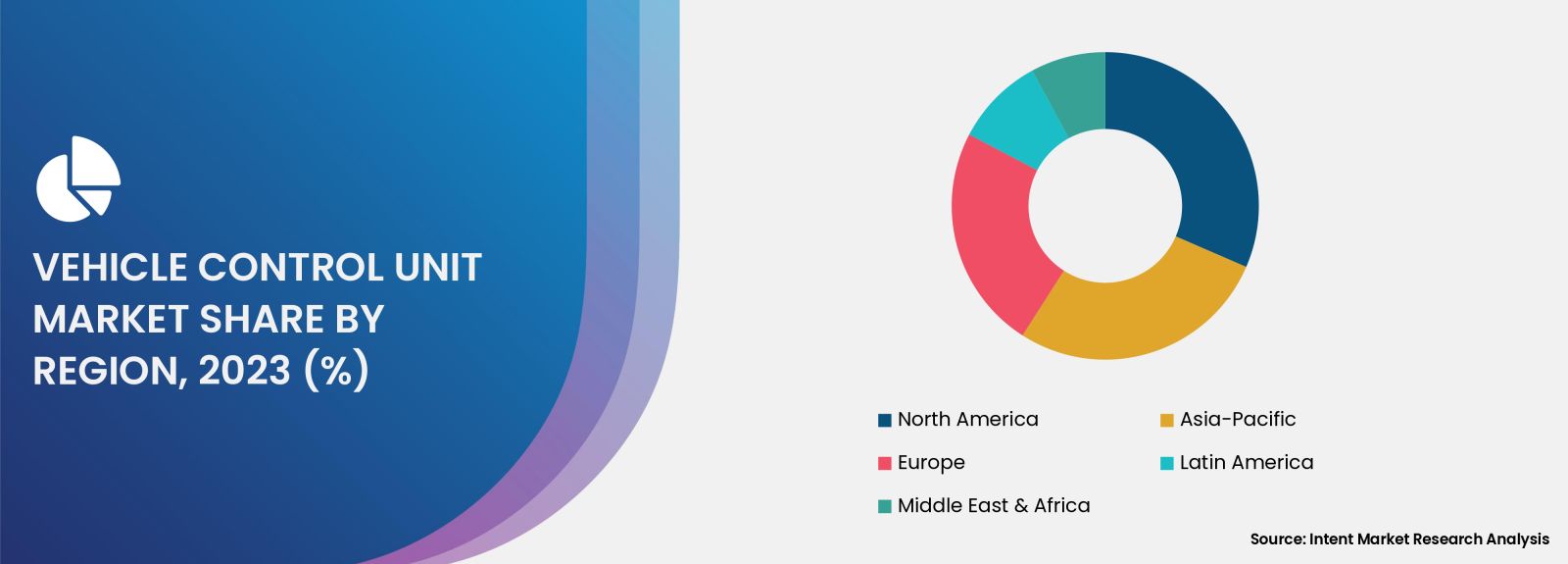

Asia-Pacific Region is Fastest Growing Owing to Rapid Automotive Development

The Asia-Pacific region is poised to be the fastest-growing market for Vehicle Control Units, driven by rapid automotive development and increasing consumer demand for advanced vehicle technologies. Countries such as China, India, and Japan are witnessing significant growth in their automotive sectors, fueled by rising disposable incomes and a growing middle class. The increasing adoption of electric vehicles in this region further accelerates the demand for advanced VCUs, as manufacturers seek to enhance performance and comply with environmental regulations.

Additionally, the Asia-Pacific region is home to several leading automotive manufacturers and suppliers, creating a robust ecosystem for innovation and development. The rise of smart manufacturing and advancements in automotive technologies are positioning this region as a key player in the global VCU market. As the demand for connected and electrified vehicles continues to rise, the Asia-Pacific region is expected to witness substantial growth, contributing significantly to the overall Vehicle Control Unit market.

Competitive Landscape

The Vehicle Control Unit market is characterized by intense competition, with several key players leading the industry. Prominent companies such as Bosch, Continental AG, Denso Corporation, and ZF Friedrichshafen AG are at the forefront of VCU development, continually innovating to meet the growing demands for advanced vehicle technologies. These companies invest heavily in research and development to enhance their product offerings, focusing on integrating cutting-edge technologies such as artificial intelligence, machine learning, and IoT into their VCUs.

Moreover, strategic partnerships and collaborations are becoming increasingly common in the VCU market, as companies seek to leverage each other’s strengths to develop advanced solutions. The competitive landscape is also influenced by the growing trend of electrification and automation in the automotive sector, prompting companies to expand their portfolios to include electric and hybrid vehicle technologies. As the market evolves, leading players will need to adapt to changing consumer preferences and regulatory requirements to maintain their competitive edge in the Vehicle Control Unit market.

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 5.3 billion |

|

Forecasted Value (2030) |

USD 12.1 billion |

|

CAGR (2024 – 2030) |

12.6% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Vehicle Control Unit Market By Product Type (ECU, TCU, BCM, PCM, Chassis Control Module, TCU), By Vehicle Type (Passenger Cars, LCVs, HCVs, 2 & 3 Wheelers), By Propulsion Type (ICE, EV, Hybrid Vehicles), and By Technology (Embedded Control Units, Distributed Control Units, Networked Control Units) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Vehicle Control Unit Market, by Product Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Engine Control Unit (ECU) |

|

4.2. Transmission Control Unit (TCU) |

|

4.3. Body Control Module (BCM) |

|

4.4. Powertrain Control Module (PCM) |

|

4.5. Chassis Control Module |

|

4.6. Telematics Control Unit (TCU) |

|

4.7. Others |

|

5. Vehicle Control Unit Market, by Vehicle Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Passenger Cars |

|

5.2. Light Commercial Vehicles (LCVs) |

|

5.3. Heavy Commercial Vehicles (HCVs) |

|

5.4. 2 & 3 Wheelers |

|

6. Vehicle Control Unit Market, by Propulsion (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Internal Combustion Engine (ICE) |

|

6.2. Electric Vehicles (EVs) |

|

6.3. Hybrid Vehicles |

|

7. Vehicle Control Unit Market, by Technology (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Embedded Control Units |

|

7.2. Distributed Control Units |

|

7.3. Networked Control Units |

|

7.4. Others |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Vehicle Control Unit Market, by Product Type |

|

8.2.7. North America Vehicle Control Unit Market, by Vehicle Type |

|

8.2.8. North America Vehicle Control Unit Market, by Propulsion |

|

8.2.9. North America Vehicle Control Unit Market, by Technology |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Vehicle Control Unit Market, by Product Type |

|

8.2.10.1.2. US Vehicle Control Unit Market, by Vehicle Type |

|

8.2.10.1.3. US Vehicle Control Unit Market, by Propulsion |

|

8.2.10.1.4. US Vehicle Control Unit Market, by Technology |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Aptiv |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Bosch |

|

10.3. Continental |

|

10.4. Delphi Technologies |

|

10.5. Denso Products and Services Americas, Inc. |

|

10.6. Eaton |

|

10.7. Hitachi |

|

10.8. Infineon Technologies |

|

10.9. Magna International |

|

10.10. NXP Semiconductors |

|

10.11. Renesas Electronics Corporation |

|

10.12. Siemens |

|

10.13. Texas Instruments |

|

10.14. Valeo |

|

10.15. ZF Friedrichshafen |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Vehicle Control Unit Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Vehicle Control Unit Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the Vehicle Control Unit ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Vehicle Control Unit Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA