As per Intent Market Research, the Vegan Food Market was valued at USD 20.2 billion in 2024-e and will surpass USD 39.8 billion by 2030; growing at a CAGR of 12.0% during 2025 - 2030.

The vegan food market is experiencing significant growth, driven by the rising awareness of health and environmental issues as well as the growing demand for plant-based products. Consumers are increasingly adopting plant-based diets, not only for health reasons but also due to ethical concerns related to animal welfare and the environmental impact of animal agriculture. As this trend accelerates, the vegan food market is expanding across various food categories, including dairy alternatives, meat substitutes, snacks, beverages, and desserts.

In addition to health and ethical motivations, innovations in food technology and the availability of a wider variety of vegan products are propelling the market forward. The development of plant-based alternatives that closely mimic the taste and texture of animal-derived products has also attracted a broader consumer base, including those who may not strictly follow a vegan diet but are exploring plant-based options. This is fueling the demand for vegan food products and further solidifying their place in the mainstream food industry.

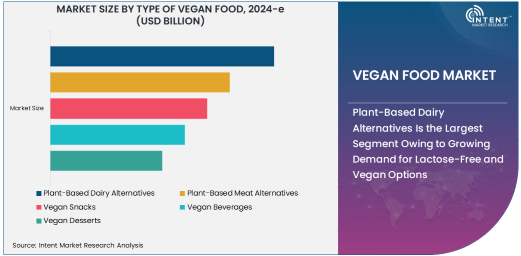

Plant-Based Dairy Alternatives Is the Largest Segment Owing to Growing Demand for Lactose-Free and Vegan Options

Plant-based dairy alternatives are the largest segment within the vegan food market, driven by the increasing demand for lactose-free and vegan alternatives to traditional dairy products. Products such as plant-based milk (soy, almond, oat), vegan cheeses, and yogurts are becoming staples in households, especially as consumers seek healthier and more sustainable dietary options.

The growth of this segment is supported by rising concerns about dairy consumption, including lactose intolerance and the environmental impact of dairy farming. Plant-based dairy products are not only viewed as more ethical and sustainable but also as a healthier choice for individuals looking to reduce their intake of saturated fats and animal-based ingredients. With innovations improving taste and texture, plant-based dairy alternatives are gaining a significant market share and are expected to continue to grow in popularity.

Nuts and Seeds Are the Fastest Growing Product Ingredients Owing to Their Nutritional Benefits and Versatility

Nuts and seeds are the fastest growing product ingredients in the vegan food market, driven by their nutritional benefits and versatility in plant-based formulations. Ingredients like almonds, cashews, chia seeds, flaxseeds, and sunflower seeds are increasingly used in vegan products such as snacks, dairy alternatives, and protein bars. These ingredients are rich in healthy fats, protein, and essential nutrients, making them a popular choice for consumers seeking both health benefits and taste.

The growth of nuts and seeds as key ingredients is also linked to the rising awareness of their ability to support plant-based diets with important micronutrients that are often lacking in vegan alternatives. With the demand for healthier, nutrient-dense foods on the rise, nuts and seeds are becoming integral to the formulation of vegan products that cater to a broad range of dietary preferences.

Supermarkets and Hypermarkets Are the Largest Distribution Channel Owing to Wide Consumer Reach and Convenience

Supermarkets and hypermarkets are the largest distribution channel within the vegan food market, owing to their wide consumer reach and convenience. These retail outlets offer a broad selection of vegan food products, from plant-based meats to dairy alternatives, in one location, making it easier for consumers to find and purchase vegan options.

The growth of supermarkets and hypermarkets as the primary distribution channel is also fueled by the increased shelf space dedicated to plant-based and vegan products in response to growing consumer demand. These stores are able to cater to a diverse range of consumers, including those who are fully vegan and those who are simply incorporating more plant-based items into their diets. As a result, supermarkets and hypermarkets play a crucial role in driving the expansion of the vegan food market.

E-Commerce Is the Fastest Growing End-Use Industry Owing to the Convenience of Online Shopping and Wider Product Range

E-commerce is the fastest growing end-use industry in the vegan food market, driven by the increasing convenience of online shopping and the wider range of products available on digital platforms. Consumers are increasingly purchasing vegan food products online, attracted by the convenience of home delivery and the ability to browse a vast selection of plant-based options.

The growth of e-commerce is also supported by the rise of specialized online retailers that focus solely on vegan and plant-based products, offering curated selections that cater to specific dietary needs. As consumers continue to embrace digital shopping for food and beverages, the e-commerce sector is poised to become a key driver of the vegan food market’s growth.

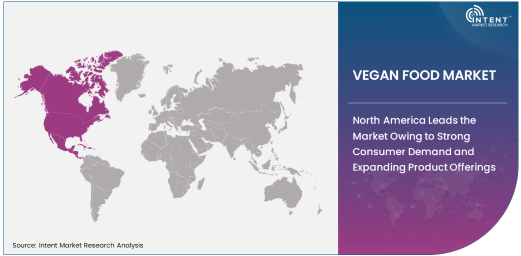

North America Leads the Market Owing to Strong Consumer Demand and Expanding Product Offerings

North America leads the vegan food market, driven by a strong consumer shift towards plant-based diets and the increasing availability of vegan food products across various retail channels. The United States and Canada have become key markets for plant-based dairy alternatives, meat substitutes, vegan snacks, and other vegan-friendly products. This surge in demand is propelled by growing health awareness, environmental concerns, and the rising number of consumers adopting vegan, vegetarian, or flexitarian diets. Major food manufacturers and retailers are capitalizing on this trend by expanding their vegan product offerings to cater to the evolving consumer preferences.

In addition, North America benefits from robust distribution channels, including supermarkets, specialty stores, and online platforms, making vegan food products more accessible to a broader audience. The increasing popularity of vegan food among not just vegans but also health-conscious and environmentally aware consumers positions North America as the dominant region in the global vegan food market, with further growth expected as the market continues to diversify.

Leading Companies and Competitive Landscape

The vegan food market is becoming highly competitive, with numerous established food companies and startups offering innovative plant-based products. Key players in the market include Beyond Meat, Impossible Foods, Oatly, and Daiya Foods, all of which are leaders in plant-based meat, dairy, and beverage alternatives. These companies are continually expanding their product portfolios and improving the taste and nutritional profiles of their offerings to meet consumer demand.

The competitive landscape is marked by intense innovation, with companies vying to capture a larger share of the market by developing new and improved vegan products. In addition to the large companies, smaller, specialized vegan food brands are also gaining traction, focusing on niche markets and offering artisanal or health-focused products. This diverse competitive environment ensures a dynamic market, with ongoing advancements in both product offerings and distribution channels.

Recent Developments:

- In December 2024, Beyond Meat expanded its partnership with McDonald's to introduce new plant-based burger options in select markets. This collaboration is expected to drive growth for both brands in the fast food industry.

- In November 2024, Impossible Foods launched a new vegan seafood line aimed at reducing the environmental impact of ocean overfishing. The product range includes plant-based shrimp and fish fillets, which are gaining traction in foodservice.

- In October 2024, Oatly announced the opening of a new production facility in Europe to meet the growing demand for its plant-based milk alternatives. This expansion will help the company address supply chain challenges and grow market share.

- In September 2024, Tofurky introduced a new line of plant-based ready-to-eat meals, designed to cater to busy consumers seeking convenient vegan options. This move aims to broaden its appeal to a wider audience.

- In August 2024, Violife expanded its product offerings with new vegan cheese varieties, including a dairy-free cream cheese and shredded cheese, which will be available in both supermarkets and online. This expansion positions Violife to capture growing consumer interest in vegan dairy alternatives.

List of Leading Companies:

- Beyond Meat

- Impossible Foods

- Oatly

- Tofurky

- Daiya Foods

- Violife

- Vitasoy

- Alpro

- Silk (WhiteWave)

- Garden of Life

- So Delicious Dairy Free

- Eat Just (formerly Hampton Creek)

- Miyoko’s Creamery

- Kite Hill

- Rebel Kitchen

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 20.2 billion |

|

Forecasted Value (2030) |

USD 39.8 billion |

|

CAGR (2025 – 2030) |

12.0% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Vegan Food Market By Type of Vegan Food (Plant-Based Dairy Alternatives, Plant-Based Meat Alternatives, Vegan Snacks, Vegan Beverages, Vegan Desserts), By Product Ingredients (Fruits and Vegetables, Legumes and Pulses, Nuts and Seeds, Cereals and Grains), By Distribution Channel (Supermarkets and Hypermarkets, Online Retail, Convenience Stores, Specialty Stores), By End-Use Industry (Retail, Food Service, E-commerce) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Beyond Meat, Impossible Foods, Oatly, Tofurky, Daiya Foods, Violife, Vitasoy, Alpro, Silk (WhiteWave), Garden of Life, So Delicious Dairy Free, Eat Just (formerly Hampton Creek), Miyoko’s Creamery, Kite Hill, Rebel Kitchen |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Vegan Food Market, by Type of Vegan Food (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Plant-Based Dairy Alternatives |

|

4.2. Plant-Based Meat Alternatives |

|

4.3. Vegan Snacks |

|

4.4. Vegan Beverages |

|

4.5. Vegan Desserts |

|

5. Vegan Food Market, by Product Ingredients (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Fruits and Vegetables |

|

5.2. Legumes and Pulses |

|

5.3. Nuts and Seeds |

|

5.4. Cereals and Grains |

|

6. Vegan Food Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Supermarkets and Hypermarkets |

|

6.2. Online Retail |

|

6.3. Convenience Stores |

|

6.4. Specialty Stores |

|

7. Vegan Food Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Retail |

|

7.2. Food Service |

|

7.3. E-commerce |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Vegan Food Market, by Type of Vegan Food |

|

8.2.7. North America Vegan Food Market, by Product Ingredients |

|

8.2.8. North America Vegan Food Market, by Distribution Channel |

|

8.2.9. North America Vegan Food Market, by End-Use Industry |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Vegan Food Market, by Type of Vegan Food |

|

8.2.10.1.2. US Vegan Food Market, by Product Ingredients |

|

8.2.10.1.3. US Vegan Food Market, by Distribution Channel |

|

8.2.10.1.4. US Vegan Food Market, by End-Use Industry |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Beyond Meat |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Impossible Foods |

|

10.3. Oatly |

|

10.4. Tofurky |

|

10.5. Daiya Foods |

|

10.6. Violife |

|

10.7. Vitasoy |

|

10.8. Alpro |

|

10.9. Silk (WhiteWave) |

|

10.10. Garden of Life |

|

10.11. So Delicious Dairy Free |

|

10.12. Eat Just (formerly Hampton Creek) |

|

10.13. Miyoko’s Creamery |

|

10.14. Kite Hill |

|

10.15. Rebel Kitchen |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Vegan Food Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Vegan Food Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Vegan Food Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA