As per Intent Market Research, the Vascular Patches Market was valued at USD 1.8 billion in 2024-e and will surpass USD 3.2 billion by 2030; growing at a CAGR of 10.0% during 2025 - 2030.

The vascular patches market is witnessing significant growth due to the increasing prevalence of vascular diseases, such as atherosclerosis, aneurysms, and other arterial conditions that require surgical intervention. Vascular patches are used in vascular surgeries to repair or reinforce blood vessels, particularly when an artery is damaged or when a bypass is necessary. These patches are designed to support the repair of arterial walls, prevent complications, and promote faster healing.

As advancements in biomaterials and surgical techniques continue to evolve, the vascular patches market is benefiting from innovations that improve the durability and biocompatibility of these products. The growing focus on minimally invasive procedures and improved surgical outcomes is driving the demand for vascular patches, especially in critical surgeries such as aortic and carotid artery repair.

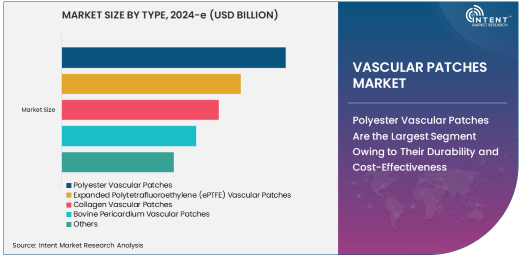

Polyester Vascular Patches Are the Largest Segment Owing to Their Durability and Cost-Effectiveness

Polyester vascular patches are the largest segment in the vascular patches market, primarily due to their durability and cost-effectiveness. Made from synthetic polyester material, these patches are widely used in vascular surgeries for both arterial and venous repairs. Polyester patches offer excellent strength, resistance to degradation, and are relatively easy to handle during surgery, making them the preferred choice for many vascular procedures.

Polyester patches are particularly favored for aortic repair surgeries, where their mechanical properties are essential for supporting large blood vessels under high pressure. The availability of polyester vascular patches at a competitive price point also contributes to their widespread use in hospitals and clinics, solidifying their position as the largest segment in the market.

Aortic Repair Is the Largest Application Segment Owing to the High Incidence of Aortic Diseases

Aortic repair is the largest application segment in the vascular patches market, driven by the high incidence of aortic diseases, including aneurysms and dissections. Aortic repair often requires the use of vascular patches to reinforce the weakened sections of the aorta and restore blood flow. Aortic aneurysms, in particular, are a leading cause of death globally, making early intervention and effective repair critical.

The growing number of surgeries aimed at repairing or replacing damaged aortic segments, coupled with advancements in surgical techniques and the development of better graft materials, has fueled the demand for aortic repair applications. As awareness of aortic disease increases and diagnostic tools improve, the need for vascular patches in aortic repairs is expected to remain high, further driving the market.

Hospitals Are the Largest End-Use Industry Owing to the Complexity of Vascular Surgeries

Hospitals are the largest end-use industry for vascular patches due to the complexity and specialization required in vascular surgeries. The need for advanced medical technologies, surgical expertise, and the ability to handle critical cases make hospitals the preferred setting for the majority of vascular patch procedures. Hospitals are equipped with specialized vascular units, operating theaters, and intensive care units to provide comprehensive care for patients undergoing complex procedures like aortic and carotid artery repair.

The high volume of vascular surgeries performed in hospitals, along with their capacity to treat severe cases, ensures that they will continue to be the dominant end-use sector in the vascular patches market. As surgical procedures become more sophisticated and minimally invasive, hospitals will remain at the forefront of using vascular patches in critical repairs.

North America Leads the Market Owing to High Surgical Volume and Advancements in Medical Devices

North America holds the largest share in the vascular patches market, primarily driven by the high volume of vascular surgeries and the continuous advancements in medical devices. The United States is a key contributor, with a significant demand for vascular patches used in procedures such as aortic repair, carotid artery repair, and femoral artery repair. The region's well-established healthcare infrastructure, along with the increasing prevalence of cardiovascular diseases, has led to a rising need for effective vascular repair solutions.

Moreover, North America benefits from strong regulatory frameworks, including FDA approvals, which ensure the availability of high-quality and innovative vascular patch technologies. The continuous development of bioabsorbable and synthetic materials has enhanced the performance and safety of vascular patches, further boosting their adoption in the region. With ongoing innovations in surgical techniques and materials, North America is poised to maintain its leadership in the vascular patches market.

Leading Companies and Competitive Landscape

The vascular patches market is competitive, with major players such as Medtronic, Gore Medical, and Cook Medical dominating the market. These companies are focusing on developing innovative vascular patch materials and improving the biocompatibility of their products. Polyester and expanded polytetrafluoroethylene (ePTFE) patches are the primary offerings from these players, and ongoing research into bioengineered patches is expected to drive further advancements.

The competitive landscape also includes smaller companies that specialize in developing niche vascular patch solutions, such as collagen or bovine pericardium patches, which are gaining traction due to their natural composition and enhanced tissue integration properties. As the demand for effective and reliable vascular repair solutions grows, competition in the vascular patches market will intensify, with companies investing in research and development to stay ahead of the curve.

Recent Developments:

- In December 2024, Medtronic announced a breakthrough in collagen-based vascular patches, offering superior flexibility and durability for artery repair surgeries. This development is set to enhance the company’s market position in vascular repair solutions.

- In November 2024, W.L. Gore & Associates launched an expanded range of ePTFE vascular patches that offer improved biocompatibility and reduced infection risks. The new product line aims to meet the growing demand for safe and efficient vascular surgery materials.

- In October 2024, LeMaitre Vascular received FDA clearance for its advanced polyester vascular patches designed for complex aortic repair procedures. The clearance is expected to boost the company’s presence in the vascular patch market.

- In September 2024, Abbott Laboratories introduced a new series of hemostatic vascular patches, which significantly reduce bleeding risks during surgery. The innovation is set to transform surgical approaches for arterial and venous repairs.

- In August 2024, Biomerics acquired a leading manufacturer of bovine pericardium vascular patches to strengthen its portfolio in the cardiovascular segment. This acquisition will broaden the company’s offerings in high-demand vascular patch materials.

List of Leading Companies:

- Medtronic

- Johnson & Johnson

- Boston Scientific

- Cook Medical

- Terumo Corporation

- W.L. Gore & Associates

- B. Braun Melsungen

- Edwards Lifesciences

- LeMaitre Vascular

- Abbott Laboratories

- Cardinal Health

- Cryolife

- Asahi Kasei Medical

- Biomerics

- Maquet Medical Systems

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.8 billion |

|

Forecasted Value (2030) |

USD 3.2 billion |

|

CAGR (2025 – 2030) |

10.0% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Vascular Patches Market By Type (Polyester Vascular Patches, Expanded Polytetrafluoroethylene (ePTFE) Vascular Patches, Collagen Vascular Patches, Bovine Pericardium Vascular Patches), By Application (Aortic Repair, Carotid Artery Repair, Femoral Artery Repair), By End-Use (Hospitals, Clinics, Ambulatory Surgical Centers) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Medtronic, Johnson & Johnson, Boston Scientific, Cook Medical, Terumo Corporation, W.L. Gore & Associates, B. Braun Melsungen, Edwards Lifesciences, LeMaitre Vascular, Abbott Laboratories, Cardinal Health, Cryolife, Asahi Kasei Medical, Biomerics, Maquet Medical Systems |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Vascular Patches Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Polyester Vascular Patches |

|

4.2. Expanded Polytetrafluoroethylene (ePTFE) Vascular Patches |

|

4.3. Collagen Vascular Patches |

|

4.4. Bovine Pericardium Vascular Patches |

|

4.5. Others |

|

5. Vascular Patches Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Aortic Repair |

|

5.2. Carotid Artery Repair |

|

5.3. Femoral Artery Repair |

|

5.4. Others |

|

6. Vascular Patches Market, by End-Use (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals |

|

6.2. Clinics |

|

6.3. Ambulatory Surgical Centers |

|

6.4. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Vascular Patches Market, by Type |

|

7.2.7. North America Vascular Patches Market, by Application |

|

7.2.8. North America Vascular Patches Market, by End-Use |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Vascular Patches Market, by Type |

|

7.2.9.1.2. US Vascular Patches Market, by Application |

|

7.2.9.1.3. US Vascular Patches Market, by End-Use |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Medtronic |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Johnson & Johnson |

|

9.3. Boston Scientific |

|

9.4. Cook Medical |

|

9.5. Terumo Corporation |

|

9.6. W.L. Gore & Associates |

|

9.7. B. Braun Melsungen |

|

9.8. Edwards Lifesciences |

|

9.9. LeMaitre Vascular |

|

9.10. Abbott Laboratories |

|

9.11. Cardinal Health |

|

9.12. Cryolife |

|

9.13. Asahi Kasei Medical |

|

9.14. Biomerics |

|

9.15. Maquet Medical Systems |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Vascular Patches Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Vascular Patches Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Vascular Patches Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA