As per Intent Market Research, the UV Stabilizers Market was valued at USD 1.7 billion in 2024-e and will surpass USD 3.4 billion by 2030; growing at a CAGR of 10.7% during 2025 - 2030.

The global UV stabilizers market is experiencing significant growth due to the increasing demand for materials that can withstand ultraviolet radiation, which can cause degradation, discoloration, and other forms of damage. These stabilizers are essential additives used in a variety of industries, from automotive to construction, to enhance the longevity and performance of materials. As environmental concerns grow, industries are focusing on products that provide better durability and sustainability. The UV stabilizers market consists of several segments, such as product type, application, end-user industry, and distribution channels, each contributing to the market's expansion.

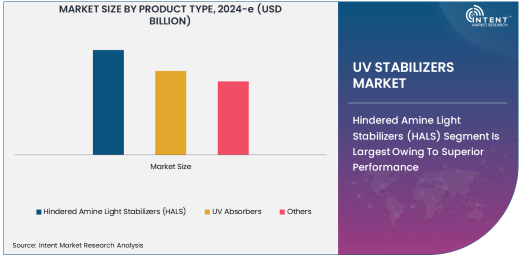

Hindered Amine Light Stabilizers (HALS) Segment Is Largest Owing To Superior Performance

Among the different types of UV stabilizers, Hindered Amine Light Stabilizers (HALS) dominate the market due to their exceptional performance in protecting materials against UV degradation. HALS are widely used in various industries because they prevent polymer degradation by scavenging free radicals that are generated when materials are exposed to UV light. This type of stabilizer is particularly effective in plastic materials, which are highly susceptible to UV-induced damage. HALS' ability to provide long-term protection against fading, cracking, and deterioration makes them a preferred choice in numerous applications, especially in the automotive, packaging, and construction industries.

The demand for HALS is being driven by the increasing use of plastics in outdoor applications, such as automotive parts and packaging materials. As manufacturers seek to improve the durability and sustainability of their products, HALS offer the advantage of enhancing the lifespan of materials without compromising their visual or functional properties. This trend is expected to continue as industries focus on reducing material replacement costs and improving product quality. Furthermore, the versatility of HALS in different environmental conditions, such as extreme sunlight exposure, further strengthens its position in the market.

Plastics Application Is Largest Owing To Widespread Usage Across Industries

The plastics application segment holds the largest share in the UV stabilizers market, driven by the widespread use of plastics in both consumer and industrial products. Plastics are particularly vulnerable to UV radiation, which can cause discoloration, brittleness, and degradation of their structural integrity. Therefore, the use of UV stabilizers, especially HALS and UV absorbers, has become crucial in ensuring the longevity of plastic products, particularly those exposed to outdoor environments. The automotive and packaging industries are the largest consumers of UV-stabilized plastics, as they require materials that can withstand long-term exposure to sunlight without deteriorating.

In addition to automotive and packaging, the plastics segment also includes applications in construction, electronics, and agricultural sectors, where UV-stabilized plastics are used for a variety of products, such as window frames, roofing materials, electrical housings, and agricultural films. As the global plastic production continues to grow, the demand for UV stabilizers in this segment is expected to remain strong. Moreover, with increasing awareness about sustainability, there is a growing push for eco-friendly stabilizers that offer similar or superior protection with less environmental impact, which is further propelling the market growth.

Automotive End-User Industry Is Fastest Growing Owing To Demand for Durable Materials

The automotive industry is the fastest-growing end-user segment for UV stabilizers, driven by the increasing demand for durable materials that can withstand harsh environmental conditions. The use of UV stabilizers in automotive parts such as exterior trim, bumpers, and dashboards helps to maintain the aesthetic appeal and structural integrity of these components. As automakers focus on producing vehicles with longer lifespans and improved environmental performance, UV stabilizers are becoming essential in automotive manufacturing. Moreover, the shift towards electric vehicles (EVs) has opened up new opportunities for UV stabilizers, as these vehicles require durable materials for both interior and exterior parts.

As the automotive industry continues to expand in emerging markets, particularly in Asia-Pacific and Latin America, the demand for UV-stabilized materials is expected to rise. In addition to vehicle parts, UV stabilizers are used in automotive coatings to protect surfaces from the damaging effects of UV radiation. This trend is likely to continue as car manufacturers increasingly prioritize the durability and sustainability of their products. Furthermore, government regulations regarding vehicle emissions and environmental impact are encouraging automakers to use more durable and sustainable materials, which in turn drives the demand for UV stabilizers.

Direct Sales Distribution Channel Is Largest Owing To Strong Manufacturer-Consumer Relationships

In the distribution channel segment, direct sales is the largest channel for UV stabilizers, primarily due to the strong relationships between manufacturers and end-users. This channel allows for better control over product quality, customer service, and product customization. Direct sales are particularly advantageous for large-scale industrial clients, such as those in the automotive, construction, and packaging sectors, who require specialized products tailored to their specific needs. Additionally, direct sales facilitate better communication and technical support, ensuring that clients receive the right UV stabilizers for their applications.

Direct sales are especially important in markets where UV stabilizers are used in highly regulated industries or where product performance is critical. Manufacturers often rely on direct relationships with suppliers to ensure that they meet the specific performance standards and regulatory requirements needed for their products. Furthermore, direct sales offer manufacturers the opportunity to educate clients on the benefits of using UV stabilizers, providing them with the necessary information to make informed purchasing decisions. As a result, this distribution channel is expected to maintain its dominance in the UV stabilizers market.

Asia-Pacific Region Is Fastest Growing Owing To Increasing Industrialization

The Asia-Pacific region is the fastest-growing market for UV stabilizers, owing to rapid industrialization and the increasing demand for durable materials across various industries. Countries like China, India, Japan, and South Korea are witnessing significant growth in manufacturing sectors, including automotive, packaging, and construction, all of which require UV-stabilized materials. As these countries continue to expand their industrial output, the demand for UV stabilizers is expected to rise, driven by the need for high-performance materials that can withstand UV degradation. The growing middle class in these regions is also contributing to the demand for UV-stabilized consumer goods, such as electronics and textiles.

In addition to industrial growth, the increasing awareness about environmental sustainability is driving the adoption of UV stabilizers in the region. Governments in Asia-Pacific are implementing stricter regulations on product durability and environmental impact, prompting industries to adopt UV stabilizers that provide long-lasting protection. As a result, the Asia-Pacific region is poised to see significant growth in the UV stabilizers market, with demand driven by both industrial applications and the consumer goods sector.

Competitive Landscape

The UV stabilizers market is highly competitive, with several key players dominating the industry. Companies like BASF SE, Evonik Industries AG, and Clariant International Ltd. are the leading suppliers of UV stabilizers, offering a wide range of products that cater to various industries, including automotive, packaging, and construction. These companies are focusing on product innovation, sustainability, and expanding their market reach through mergers, acquisitions, and partnerships.

To stay ahead in the market, these companies are investing in research and development to create advanced UV stabilizers that offer superior protection while minimizing environmental impact. The competitive landscape is also shaped by the increasing demand for eco-friendly products, which is pushing companies to develop more sustainable and biodegradable UV stabilizers. Additionally, as industries continue to grow in emerging markets, competition is expected to intensify, leading to further innovations and collaborations in the UV stabilizers market

Recent Developments:

- BASF SE announced the launch of a new range of UV stabilizers for the automotive industry to enhance the longevity of exterior components exposed to sunlight.

- Clariant International Ltd. expanded its portfolio with advanced UV absorbers that offer improved protection for plastic products in outdoor applications.

- Evonik Industries AG entered a strategic partnership with a leading coatings manufacturer to develop UV-resistant coatings for the construction sector.

- Songwon Industrial Co., Ltd. launched a new product that combines HALS and UV absorbers, offering superior protection against environmental degradation in polymers.

- Lanxess AG acquired a smaller player in the UV stabilizer market to strengthen its position in the personal care and cosmetics industries

List of Leading Companies:

- BASF SE

- Clariant International Ltd.

- Evonik Industries AG

- Songwon Industrial Co., Ltd.

- SABIC

- Addivant

- Solvay S.A.

- Lanxess AG

- The Dow Chemical Company

- Uvinul (A division of BASF)

- Asahi Kasei Corporation

- Arkema SA

- Sumitomo Chemical Co., Ltd.

- Chemtura Corporation

- Mitsui Chemicals

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.7 billion |

|

Forecasted Value (2030) |

USD 3.4 billion |

|

CAGR (2025 – 2030) |

10.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

UV Stabilizers Market By Product Type (Hindered Amine Light Stabilizers (HALS), UV Absorbers), By Application (Plastics, Coatings, Adhesives & Sealants, Textiles, Cosmetics & Personal Care), By End-User Industry (Automotive, Packaging, Construction, Agriculture, Electronics), and By Distribution Channel (Direct Sales, Online Retail, Distributors, Specialty Stores, Wholesale Markets) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

BASF SE, Clariant International Ltd., Evonik Industries AG, Songwon Industrial Co., Ltd., SABIC, Addivant, Solvay S.A., Lanxess AG, The Dow Chemical Company, Uvinul (A division of BASF), Asahi Kasei Corporation, Arkema SA, Sumitomo Chemical Co., Ltd., Chemtura Corporation, Mitsui Chemicals |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. UV Stabilizers Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Hindered Amine Light Stabilizers (HALS) |

|

4.2. UV Absorbers |

|

4.3. Others |

|

5. UV Stabilizers Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Plastics |

|

5.2. Coatings |

|

5.3. Adhesives & Sealants |

|

5.4. Textiles |

|

5.5. Cosmetics & Personal Care |

|

5.6. Others |

|

6. UV Stabilizers Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Automotive |

|

6.2. Packaging |

|

6.3. Construction |

|

6.4. Agriculture |

|

6.5. Electronics |

|

6.6. Others |

|

7. UV Stabilizers Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Direct Sales |

|

7.2. Online Retail |

|

7.3. Distributors |

|

7.4. Specialty Stores |

|

7.5. Wholesale Markets |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America UV Stabilizers Market, by Product Type |

|

8.2.7. North America UV Stabilizers Market, by Application |

|

8.2.8. North America UV Stabilizers Market, by End-User Industry |

|

8.2.9. North America UV Stabilizers Market, by Distribution Channel |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US UV Stabilizers Market, by Product Type |

|

8.2.10.1.2. US UV Stabilizers Market, by Application |

|

8.2.10.1.3. US UV Stabilizers Market, by End-User Industry |

|

8.2.10.1.4. US UV Stabilizers Market, by Distribution Channel |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. BASF SE |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Clariant International Ltd. |

|

10.3. Evonik Industries AG |

|

10.4. Songwon Industrial Co., Ltd. |

|

10.5. SABIC |

|

10.6. Addivant |

|

10.7. Solvay S.A. |

|

10.8. Lanxess AG |

|

10.9. The Dow Chemical Company |

|

10.10. Uvinul (A division of BASF) |

|

10.11. Asahi Kasei Corporation |

|

10.12. Arkema SA |

|

10.13. Sumitomo Chemical Co., Ltd. |

|

10.14. Chemtura Corporation |

|

10.15. Mitsui Chemicals |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the UV Stabilizers Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the UV Stabilizers Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the UV Stabilizers Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA