As per Intent Market Research, the Utility Scale High Voltage Digital Substation Market was valued at USD 5.0 Billion in 2024-e and will surpass USD 12.1 Billion by 2030; growing at a CAGR of 15.9% during 2025-2030.

The utility scale high voltage digital substation market is experiencing significant growth as the global energy infrastructure modernizes to meet the increasing demand for efficient power transmission and the integration of renewable energy. Digital substations are transforming traditional power systems by incorporating advanced technologies such as digital protection and control systems, SCADA systems, and advanced metering infrastructure (AMI). These technologies enhance the monitoring, control, and automation capabilities of substations, allowing utilities to improve grid reliability, efficiency, and flexibility. As energy generation increasingly shifts to renewable sources such as solar and wind, digital substations play a pivotal role in optimizing grid performance and ensuring that power is transmitted reliably and efficiently across large distances.

The demand for utility-scale high voltage digital substations is further amplified by the growing need for smart grid infrastructure and the shift towards decentralized energy systems. Digital substations allow for better management of variable renewable energy generation and facilitate the real-time integration of energy from diverse sources. With the ability to handle high and extra-high voltage levels, these substations are integral to modernizing power systems to accommodate fluctuating energy inputs while ensuring a stable and resilient grid. The ongoing investment in renewable energy, as well as the drive to reduce carbon emissions globally, is expected to continue driving the adoption of digital substations in the coming years.

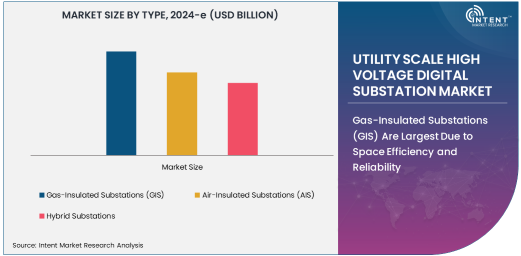

Gas-Insulated Substations (GIS) Are Largest Due to Space Efficiency and Reliability

Gas-insulated substations (GIS) are the largest sub-segment within the utility scale high voltage digital substation market due to their compact design, high reliability, and enhanced performance. GIS use sulfur hexafluoride (SF6) gas as an insulating medium, which provides superior dielectric strength and allows for smaller, more efficient substation designs. This makes GIS particularly suitable for areas where space is limited, such as in urban environments or places with high population density. GIS is also the preferred option for high and extra-high voltage transmission due to its ability to efficiently handle large electrical loads while minimizing the footprint of substations.

The growing demand for GIS is closely linked to the need for reliable, space-efficient electrical infrastructure, particularly in cities and industrial hubs where space comes at a premium. Additionally, GIS technology offers superior protection against environmental conditions such as dust, humidity, and temperature extremes, making it a suitable choice for use in harsh operating environments. This segment’s dominance in the market is also driven by the increasing complexity of power transmission systems, as GIS ensures the uninterrupted flow of electricity while reducing the risk of faults and outages, further enhancing grid reliability.

Extra High Voltage Substations Are Critical for Renewable Energy Integration

The demand for extra high voltage (EHV) substations is particularly strong as the need to integrate renewable energy sources into the grid grows. EHV substations, designed to handle voltages above 300 kV, are essential for long-distance power transmission, especially from renewable energy plants located in remote areas. These substations are instrumental in ensuring that electricity generated from wind, solar, and other renewable sources can be efficiently transported to urban centers and industrial areas where demand is highest.

The push for renewable energy integration and the expansion of clean energy projects are expected to drive the adoption of EHV substations further. As more large-scale renewable energy projects come online, these substations will be key to maintaining grid stability and ensuring that renewable power is delivered reliably. EHV substations also play an essential role in improving transmission capacity and reducing power losses, making them crucial for managing the growing energy demands of the global population while supporting sustainability initiatives.

Digital Protection and Control Systems Drive Market Demand

Digital protection and control systems are one of the fastest-growing technologies in the utility scale high voltage digital substation market. These systems are responsible for monitoring, controlling, and protecting the electrical equipment within substations, offering real-time responses to faults and other issues. By leveraging advanced algorithms and automation, digital protection systems can quickly detect faults, isolate them, and restore power, thereby reducing downtime and improving grid stability.

The integration of digital protection and control systems is critical to the functioning of modern power grids, especially as utilities move towards smart grid solutions. These systems offer enhanced monitoring and diagnostics, allowing utilities to anticipate problems before they occur and respond more effectively to changing energy demands. With the growing complexity of modern power networks, particularly in integrating renewable energy sources, the role of digital protection and control systems has become indispensable in ensuring the resilience and efficiency of power transmission.

Indoor Installations Are Preferred for Urban and Industrial Applications

Indoor installations of high voltage digital substations are increasingly preferred in urban and industrial settings due to their compact nature and ability to operate in confined spaces. Indoor substations offer protection from external environmental factors such as extreme weather conditions, dirt, and moisture, which enhances the longevity and reliability of the equipment. Moreover, indoor substations reduce the visual impact and noise pollution that outdoor substations can cause, making them more suitable for densely populated areas.

With urbanization continuing at a rapid pace and industries requiring reliable, uninterrupted power supplies, indoor installations have become a crucial element of modern power infrastructure. These substations are also better equipped to handle the safety concerns associated with high-voltage operations in residential or commercially sensitive areas. Their space-saving qualities and lower environmental impact make them the preferred choice in many industrial and urban developments.

Power Transmission and Distribution Is the Key Application Driving Growth

Power transmission and distribution is one of the primary applications of high voltage digital substations. These substations are integral to the efficient transmission of electricity across long distances, particularly from energy generation facilities to local grids or consumers. The digitalization of substations plays a significant role in improving the efficiency and reliability of power transmission networks by providing real-time monitoring and control capabilities.

As grids become smarter and more complex, digital substations enable better control over power flows, minimizing transmission losses, and reducing the risk of faults. Additionally, with the integration of renewable energy sources, power transmission systems require modern substations that can manage variable inputs while maintaining grid stability. The increasing need for reliable and efficient power transmission is expected to continue to drive demand for high voltage digital substations in the market.

Utilities Are Leading the End-User Industry with High Adoption of Digital Substations

Utilities are the largest end-user segment of the utility scale high voltage digital substation market. Utilities are heavily investing in digital substation technology to improve the reliability, flexibility, and efficiency of their electrical grids. Digital substations enable utilities to better manage growing electricity demand, integrate renewable energy sources, and ensure a more resilient power distribution system. These substations also help utilities maintain compliance with increasingly stringent regulations and standards related to grid modernization, sustainability, and energy security.

The need for high voltage digital substations is particularly critical as utilities across the globe upgrade aging infrastructure to incorporate smart grid systems, which offer more control, automation, and real-time monitoring of power networks. As global electricity demand increases and more renewable energy projects come online, utilities are expected to continue driving demand for high voltage digital substations, making this sector a key focus for industry growth.

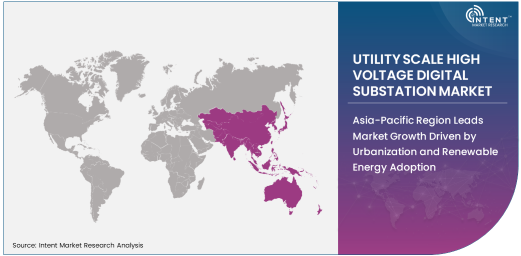

Asia-Pacific Region Leads Market Growth Driven by Urbanization and Renewable Energy Adoption

The Asia-Pacific region is the fastest-growing market for utility scale high voltage digital substations, driven by rapid urbanization, industrialization, and the large-scale adoption of renewable energy sources. Countries like China, India, and Japan are investing heavily in modernizing their power infrastructure to accommodate growing energy demands and integrate renewable sources such as wind and solar into the grid. The demand for high voltage digital substations in this region is fueled by the need to upgrade aging infrastructure, support smart grid initiatives, and expand transmission networks to connect remote renewable energy projects with major consumption centers.

Asia-Pacific's focus on developing smart cities and expanding renewable energy capacity has positioned the region as a key growth driver for the digital substation market. Additionally, the government's push for sustainable energy solutions and the reduction of carbon emissions has further accelerated the adoption of digital substations, making it a hub for innovation and infrastructure development in the power sector.

Competitive Landscape of the Utility Scale High Voltage Digital Substation Market

The utility scale high voltage digital substation market is highly competitive, with major players offering cutting-edge solutions to meet the growing demand for smart, efficient, and reliable power transmission infrastructure. Leading companies in this market include Siemens AG, General Electric (GE), Schneider Electric, ABB Ltd., and Eaton Corporation. These firms provide a wide range of digital substation solutions that incorporate advanced technologies such as SCADA systems, digital protection and control systems, and real-time monitoring tools.

The competition is expected to intensify as the demand for renewable energy integration and smart grid infrastructure continues to grow. Companies are focusing on technological innovations, regulatory compliance, and service excellence to differentiate themselves in the market. Strategic partnerships, mergers, and acquisitions are also expected to shape the competitive dynamics as firms seek to expand their product offerings and enter new markets. Additionally, the growing importance of cybersecurity and data protection in digital substations will drive further innovations and collaborations between technology companies and energy providers.

Recent Developments:

- In December 2024, Siemens AG launched a new high voltage digital substation solution featuring advanced SCADA integration for enhanced grid control.

- In November 2024, General Electric Company announced the deployment of digital substations for an offshore wind farm project, optimizing power transmission and grid stability.

- In October 2024, Schneider Electric SE unveiled an AI-driven digital substation platform for real-time predictive maintenance and energy optimization.

- In September 2024, ABB Ltd. secured a contract for supplying a high voltage digital substation to a large industrial power system in Asia.

- In August 2024, Mitsubishi Electric Corporation introduced a hybrid substation design combining digital and traditional technologies for energy-efficient power transmission.

List of Leading Companies:

- Siemens AG

- General Electric Company

- Schneider Electric SE

- Mitsubishi Electric Corporation

- ABB Ltd.

- Eaton Corporation

- Hitachi Energy Ltd.

- Toshiba Corporation

- Siemens Energy

- Hyundai Electric & Energy Systems Co.

- Alstom SA

- Kroger Electric Ltd.

- IC Electrical Ltd.

- Samsung Engineering Co.

- Tata Power

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 5.0 Billion |

|

Forecasted Value (2030) |

USD 12.1 Billion |

|

CAGR (2025 – 2030) |

15.9% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Utility Scale High Voltage Digital Substation Market by Type (Gas-Insulated Substations [GIS], Air-Insulated Substations [AIS], Hybrid Substations), Technology (Digital Protection and Control Systems, Advanced Metering Infrastructure [AMI], SCADA Systems), End-User Industry (Utilities, Renewable Energy, Industrial Applications, Power Transmission), Voltage Level (High Voltage, Extra High Voltage), Application (Power Transmission and Distribution, Renewable Energy Integration, Smart Grid Infrastructure, Industrial Power Systems), Installation (Indoor, Outdoor) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Siemens AG, General Electric Company, Schneider Electric SE, Mitsubishi Electric Corporation, ABB Ltd., Eaton Corporation, Hitachi Energy Ltd., Toshiba Corporation, Siemens Energy, Hyundai Electric & Energy Systems Co., Alstom SA, Kroger Electric Ltd., IC Electrical Ltd., Samsung Engineering Co., Tata Power |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Utility Scale High Voltage Digital Substation Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Gas-Insulated Substations (GIS) |

|

4.2. Air-Insulated Substations (AIS) |

|

4.3. Hybrid Substations |

|

5. Utility Scale High Voltage Digital Substation Market, by Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Digital Protection and Control Systems |

|

5.2. Advanced Metering Infrastructure (AMI) |

|

5.3. SCADA Systems |

|

6. Utility Scale High Voltage Digital Substation Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Utilities |

|

6.2. Renewable Energy |

|

6.3. Industrial Applications |

|

6.4. Power Transmission |

|

7. Utility Scale High Voltage Digital Substation Market, by Voltage Level (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. High Voltage (above 36 kV) |

|

7.2. Extra High Voltage (above 300 kV) |

|

8. Utility Scale High Voltage Digital Substation Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Power Transmission and Distribution |

|

8.2. Renewable Energy Integration |

|

8.3. Smart Grid Infrastructure |

|

8.4. Industrial Power Systems |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Utility Scale High Voltage Digital Substation Market, by Type |

|

9.2.7. North America Utility Scale High Voltage Digital Substation Market, by Technology |

|

9.2.8. North America Utility Scale High Voltage Digital Substation Market, by End-User Industry |

|

9.2.9. North America Utility Scale High Voltage Digital Substation Market, by Voltage Level |

|

9.2.10. North America Utility Scale High Voltage Digital Substation Market, by Application |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Utility Scale High Voltage Digital Substation Market, by Type |

|

9.2.11.1.2. US Utility Scale High Voltage Digital Substation Market, by Technology |

|

9.2.11.1.3. US Utility Scale High Voltage Digital Substation Market, by End-User Industry |

|

9.2.11.1.4. US Utility Scale High Voltage Digital Substation Market, by Voltage Level |

|

9.2.11.1.5. US Utility Scale High Voltage Digital Substation Market, by Application |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. Siemens AG |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. General Electric Company |

|

11.3. Schneider Electric SE |

|

11.4. Mitsubishi Electric Corporation |

|

11.5. ABB Ltd. |

|

11.6. Eaton Corporation |

|

11.7. Hitachi Energy Ltd. |

|

11.8. Toshiba Corporation |

|

11.9. Siemens Energy |

|

11.10. Hyundai Electric & Energy Systems Co. |

|

11.11. Alstom SA |

|

11.12. Kroger Electric Ltd. |

|

11.13. IC Electrical Ltd. |

|

11.14. Samsung Engineering Co. |

|

11.15. Tata Power |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Utility Scale High Voltage Digital Substation Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Utility Scale High Voltage Digital Substation Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Utility Scale High Voltage Digital Substation Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA