As per Intent Market Research, the Utility Distribution Transformer Market was valued at USD 18.4 Billion in 2024-e and will surpass USD 30.1 Billion by 2030; growing at a CAGR of 8.5% during 2025-2030.

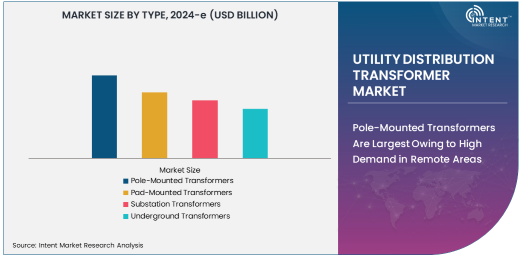

The utility distribution transformer market is essential to modern electricity distribution systems, ensuring the reliable delivery of power from substations to end-users. The market is segmented by type, power rating, end-use industry, voltage level, and cooling type. Among the various transformer types, pole-mounted transformers dominate the market due to their widespread usage in rural and remote areas. These transformers are highly favored in low-density residential areas, where overhead power lines are commonly installed. Pole-mounted transformers are compact, easy to install, and cost-effective, making them the preferred choice for utilities to extend their services to underserved regions.

Pole-Mounted Transformers Are Largest Owing to High Demand in Remote Areas

Pole-mounted transformers are an integral part of power distribution networks due to their ability to handle varied load capacities while occupying minimal space. Their easy installation and relatively low maintenance costs make them ideal for infrastructure in remote areas. The continuous need for rural electrification and the development of power distribution networks in emerging economies further supports the growth of pole-mounted transformers. These transformers ensure that even in sparsely populated regions, electricity can be efficiently delivered to homes and small businesses, providing a stable energy supply while keeping operational expenses low.

Low Power Rating (Up to 500 kVA) Leads the Market with Residential Demand

In the power rating segment, low power rating transformers (up to 500 kVA) are the largest due to their extensive use in residential and small-scale commercial applications. These transformers are commonly used to step down the voltage for domestic electricity supply, where power requirements are relatively small compared to industrial or large commercial needs. With the growing demand for residential electricity, particularly in developing regions, low power transformers are being installed in vast numbers to meet the needs of both existing and new housing developments.

The demand for low power rating transformers is also being driven by urbanization and the expansion of electrical grids in emerging markets. As cities and towns grow, there is an increasing need for reliable electrical infrastructure to support new residential areas. These transformers are ideal for such applications because of their efficiency in handling smaller loads and their ability to serve multiple residential units at once. The continued development of smart cities and residential complexes further fuels the demand for low power rating transformers, ensuring their dominance in the market.

Utilities Sector Drives Growth with Grid Modernization Initiatives

The utility industry plays a pivotal role in the global utility distribution transformer market. The utilities sector is the fastest-growing subsegment, primarily driven by the ongoing efforts to modernize aging electrical grids and incorporate renewable energy sources. Utilities require transformers that can handle the fluctuating demands of a dynamic grid while ensuring stable and efficient power distribution. The shift toward renewable energy sources, such as solar and wind, necessitates advanced transformer solutions that can manage the variability of power inputs and stabilize energy flow.

Grid modernization initiatives across the globe have significantly increased the demand for high-capacity transformers with advanced monitoring and control features. As governments and utilities invest in smart grid technologies, the need for distribution transformers that can support these developments is growing. The integration of renewable energy sources further underscores the importance of robust transformers in utility networks, enabling utilities to maintain grid stability and reliability. These factors make the utilities sector the driving force behind the market’s expansion.

Low Voltage Transformers Are Largest Owing to Residential and Commercial Use

In the voltage level segment, low voltage transformers are the largest subsegment, owing to their widespread use in residential and commercial applications. Low voltage transformers are designed to step down electricity from high transmission voltages to lower voltages suitable for domestic and small commercial use. As urban populations grow and residential areas expand, the demand for low voltage transformers continues to increase, ensuring their dominance in the market.

The low voltage segment is heavily influenced by the rise in residential construction and commercial buildings. With a growing emphasis on energy efficiency, low voltage transformers are essential for ensuring stable power distribution in homes, office buildings, and small businesses. Furthermore, the development of smart homes and buildings, which require precise and reliable power distribution systems, is fueling the demand for low voltage transformers. These transformers are critical in ensuring that electrical appliances and systems operate efficiently without overloading or damaging sensitive equipment.

Oil-Cooled Transformers Are Largest Due to Higher Efficiency and Reliability

Oil-cooled transformers are the largest segment in the cooling type category, attributed to their superior efficiency and ability to handle higher loads. Oil cooling offers better heat dissipation, making oil-cooled transformers ideal for areas with high power demands. They are widely used in industrial, commercial, and utility applications where large amounts of power need to be managed, and reliability is paramount. Oil-based cooling systems also offer the advantage of extended operational life and lower maintenance requirements compared to air-cooled transformers.

The use of oil-cooled transformers is particularly prominent in applications where transformers need to operate under high temperatures or in environments with significant load fluctuations. The ability of oil to efficiently transfer heat ensures that these transformers remain operational for long periods, even under heavy load conditions. As industrialization and urbanization continue to expand, the demand for oil-cooled transformers is expected to grow, further solidifying their position as the dominant cooling type in the utility distribution transformer market.

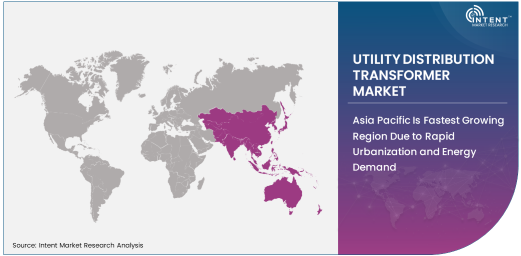

Asia Pacific Is Fastest Growing Region Due to Rapid Urbanization and Energy Demand

The Asia Pacific region is the fastest growing in the utility distribution transformer market, driven by rapid urbanization and increasing energy demand. Countries such as China, India, and Southeast Asian nations are witnessing significant population growth, resulting in the expansion of urban areas and the need for reliable electricity distribution systems. This surge in demand for electricity infrastructure, combined with government initiatives to enhance power generation and distribution networks, has spurred the demand for utility distribution transformers in the region.

Asia Pacific's rapid industrialization and urbanization make it a hotbed for transformer demand. The region's continuous expansion of residential, commercial, and industrial sectors further accelerates the need for advanced and efficient transformers. Furthermore, the growing emphasis on sustainable energy and smart grid systems in countries like India and China is driving the adoption of high-performance distribution transformers. As a result, Asia Pacific is set to remain the fastest-growing region in the global market for utility distribution transformers.

Leading Companies and Competitive Landscape

The utility distribution transformer market is highly competitive, with several global players leading the charge. Companies such as ABB Ltd., Siemens AG, Schneider Electric SE, and General Electric Company dominate the market due to their vast experience, extensive product portfolios, and innovation in energy-efficient transformer technologies. These companies are continuously investing in research and development to improve transformer performance, enhance energy efficiency, and meet the growing demand for smart grid solutions.

The competitive landscape is characterized by frequent mergers and acquisitions, with companies seeking to expand their product offerings and geographic reach. Additionally, strategic partnerships with utility providers and involvement in large-scale infrastructure projects help companies maintain their market position. As the demand for renewable energy integration and grid modernization grows, market leaders are focusing on developing advanced, adaptable, and efficient transformers to cater to the evolving needs of the energy sector.

Recent Developments:

- ABB recently launched a new range of compact, highly efficient distribution transformers, aimed at improving grid management and reducing energy losses.

- Siemens announced the acquisition of a leading smart grid technology company to enhance its capabilities in energy distribution and transformer operations.

- Schneider Electric unveiled a new innovative transformer monitoring system that integrates IoT for real-time performance data and predictive maintenance.

- GE has received regulatory approval to expand its manufacturing facility for medium- and high-voltage distribution transformers in North America.

- Mitsubishi Electric secured a major contract to supply distribution transformers for a large-scale urban development project in Asia.

List of Leading Companies:

- ABB Ltd.

- Siemens AG

- Schneider Electric SE

- General Electric Company

- Mitsubishi Electric Corporation

- Eaton Corporation PLC

- Kirloskar Electric Company

- Siemens Energy

- Toshiba Corporation

- Crompton Greaves

- Hyundai Electric & Energy Systems Co.

- Hitachi Ltd.

- Westinghouse Electric Company

- BHEL (Bharat Heavy Electricals Limited)

- TBEA Co., Ltd.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 18.4 Billion |

|

Forecasted Value (2030) |

USD 30.1 Billion |

|

CAGR (2025 – 2030) |

8.5% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Utility Distribution Transformer Market By Type (Pole-Mounted Transformers, Pad-Mounted Transformers, Substation Transformers, Underground Transformers), By Power Rating (Low Power Rating, Medium Power Rating, High Power Rating), By End-Use Industry (Residential, Commercial, Industrial, Utilities), By Voltage Level (Low Voltage, Medium Voltage, High Voltage), By Cooling Type (Air-Cooled, Oil-Cooled) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

ABB Ltd., Siemens AG, Schneider Electric SE, General Electric Company, Mitsubishi Electric Corporation, Eaton Corporation PLC, Kirloskar Electric Company, Siemens Energy, Toshiba Corporation, Crompton Greaves, Hyundai Electric & Energy Systems Co., Hitachi Ltd., Westinghouse Electric Company, BHEL (Bharat Heavy Electricals Limited), TBEA Co., Ltd. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Utility Distribution Transformer Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Pole-Mounted Transformers |

|

4.2. Pad-Mounted Transformers |

|

4.3. Substation Transformers |

|

4.4. Underground Transformers |

|

5. Utility Distribution Transformer Market, by Power Rating (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Low Power Rating (Up to 500 kVA) |

|

5.2. Medium Power Rating (501 kVA to 2 MVA) |

|

5.3. High Power Rating (Above 2 MVA) |

|

6. Utility Distribution Transformer Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Residential |

|

6.2. Commercial |

|

6.3. Industrial |

|

6.4. Utilities |

|

7. Utility Distribution Transformer Market, by Voltage Level (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Low Voltage |

|

7.2. Medium Voltage |

|

7.3. High Voltage |

|

8. Utility Distribution Transformer Market, by Cooling Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Air-Cooled |

|

8.2. Oil-Cooled |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Utility Distribution Transformer Market, by Type |

|

9.2.7. North America Utility Distribution Transformer Market, by Power Rating |

|

9.2.8. North America Utility Distribution Transformer Market, by End-Use Industry |

|

9.2.9. North America Utility Distribution Transformer Market, by Voltage Level |

|

9.2.10. North America Utility Distribution Transformer Market, by Cooling Type |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Utility Distribution Transformer Market, by Type |

|

9.2.11.1.2. US Utility Distribution Transformer Market, by Power Rating |

|

9.2.11.1.3. US Utility Distribution Transformer Market, by End-Use Industry |

|

9.2.11.1.4. US Utility Distribution Transformer Market, by Voltage Level |

|

9.2.11.1.5. US Utility Distribution Transformer Market, by Cooling Type |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. ABB Ltd. |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Siemens AG |

|

11.3. Schneider Electric SE |

|

11.4. General Electric Company |

|

11.5. Mitsubishi Electric Corporation |

|

11.6. Eaton Corporation PLC |

|

11.7. Kirloskar Electric Company |

|

11.8. Siemens Energy |

|

11.9. Toshiba Corporation |

|

11.10. Crompton Greaves |

|

11.11. Hyundai Electric & Energy Systems Co. |

|

11.12. Hitachi Ltd. |

|

11.13. Westinghouse Electric Company |

|

11.14. BHEL (Bharat Heavy Electricals Limited) |

|

11.15. TBEA Co., Ltd. |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Utility Distribution Transformer Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Utility Distribution Transformer Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Utility Distribution Transformer Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA