As per Intent Market Research, the Utility Boiler Market was valued at USD 44.2 Billion in 2024-e and will surpass USD 65.1 Billion by 2030; growing at a CAGR of 6.7% during 2025-2030.

The utility boiler market plays a significant role in energy generation across multiple industries, providing essential steam and power for electricity generation and industrial processes. With growing demand for energy worldwide, coupled with the transition toward cleaner technologies, the market is evolving to accommodate both traditional energy sources like coal and oil, as well as renewable energy options such as biomass. This market is expected to grow steadily, driven by both technological advancements in boiler design and the increasing need for energy efficiency.

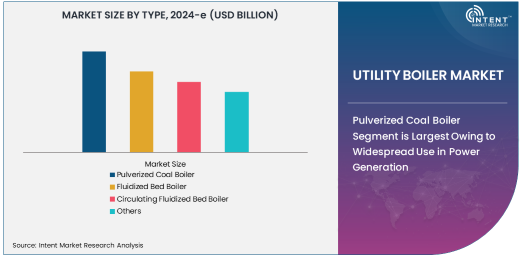

Pulverized Coal Boiler Segment is Largest Owing to Widespread Use in Power Generation

Pulverized coal boilers (PCBs) are the most widely used boilers in the utility boiler market, particularly in large-scale power plants. The segment dominates the global market due to the high efficiency and cost-effectiveness of coal as a fuel source. Pulverized coal boilers are favored for their ability to handle larger capacities and provide high thermal efficiency, which is critical in large-scale power generation. These boilers offer better combustion control and lower emissions, making them suitable for meeting strict environmental regulations in many regions.

As countries like China, India, and the United States continue to rely heavily on coal for power generation, the demand for pulverized coal boilers is expected to remain strong. Additionally, improvements in boiler technology have made these systems more efficient and environmentally friendly, allowing them to comply with ever-tightening emissions standards. The ongoing use of coal as a primary energy source in emerging markets further supports the continued dominance of the pulverized coal boiler segment.

Coal Fuel Type is Largest Owing to Cost-Effectiveness and Abundant Supply

Coal remains the dominant fuel type for utility boilers, primarily due to its affordability and abundance, particularly in regions like Asia-Pacific, North America, and Europe. The economic advantage of coal as a fuel compared to other alternatives, such as natural gas or oil, positions it as the largest subsegment in the fuel type category. Coal-fired boilers are widely used in power generation and industrial sectors, where a constant and reliable source of energy is crucial.

Although there is a global shift toward cleaner energy sources, coal continues to be a preferred fuel type due to its low cost and high energy content. For instance, India and China, as major coal consumers, continue to drive the demand for coal-based utility boilers. Despite the growing push for renewable energy, coal remains a key player in meeting the world's energy needs, especially in countries with abundant coal reserves and limited access to alternative energy sources.

Power Generation is the Largest End-Use Industry for Utility Boilers

The power generation industry is the largest end-user of utility boilers, accounting for the highest demand in the market. Boilers in this sector are responsible for generating steam required to drive turbines in thermal power plants, making them essential for electricity generation. With the global demand for electricity rising, especially in developing countries, the need for reliable, high-capacity boilers has surged.

Thermal power plants, which rely on coal, natural gas, or biomass, are the primary consumers of utility boilers. As energy needs continue to grow, particularly in emerging economies, the power generation sector is expected to remain the largest end-use industry for utility boilers. Furthermore, advancements in boiler technology, such as supercritical and ultra-supercritical steam conditions, continue to enhance the efficiency of power plants, making utility boilers even more integral to the power generation process.

Above 500 MW Capacity is the Largest Due to High Demand for Large-Scale Power Plants

The "Above 500 MW" capacity segment dominates the utility boiler market, driven by the growing need for large-scale power plants capable of meeting the increasing global demand for electricity. Larger boilers provide higher thermal efficiency and are crucial for utility-scale power generation. These boilers are typically used in coal-fired and gas-fired power plants, where high capacity is necessary to generate a large volume of electricity for both industrial and residential needs.

The demand for high-capacity boilers is particularly strong in regions such as Asia-Pacific and the Middle East, where rapid industrialization and urbanization drive the need for large power plants. Larger boilers, with their ability to produce more energy per unit, are also favored for their economies of scale, making them more cost-efficient over the long term. The growing trend toward mega power plants further supports the dominance of the "Above 500 MW" capacity segment.

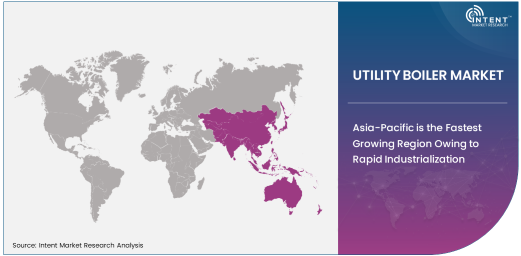

Asia-Pacific is the Fastest Growing Region Owing to Rapid Industrialization

Asia-Pacific is the fastest-growing region in the utility boiler market, driven by rapid industrialization, population growth, and increasing urbanization. Countries like China and India are expanding their power generation capacity to meet the rising energy demands of their burgeoning economies. As these nations invest in both traditional and renewable energy sources, the demand for utility boilers continues to rise.

The region is also investing heavily in modernizing its infrastructure to improve energy efficiency and reduce emissions. As a result, the Asia-Pacific market is expected to witness significant growth in the coming years, especially in countries with abundant coal reserves. The ongoing push for renewable energy sources, such as biomass, in the region further enhances the market's growth potential for utility boilers.

Competitive Landscape and Leading Companies

The competitive landscape of the utility boiler market is highly fragmented, with numerous global and regional players competing for market share. Leading companies in the market include General Electric (GE), Siemens AG, Mitsubishi Heavy Industries, Babcock & Wilcox Enterprises, and Doosan Heavy Industries & Construction. These companies have strong portfolios of boiler technologies, offering solutions for both traditional and renewable energy applications. They also invest heavily in research and development to improve boiler efficiency, reduce emissions, and enhance the sustainability of power plants.

In addition to these established players, smaller companies and regional manufacturers are also capitalizing on the growing demand for utility boilers in emerging markets. The increasing emphasis on cleaner energy technologies and boiler innovations presents opportunities for both established and new players to capture market share in this evolving landscape. With a growing shift toward renewable energy and sustainability goals, companies are focusing on offering more energy-efficient solutions to stay competitive.

Recent Developments:

- General Electric announced securing a contract to supply high-efficiency boilers for a new power plant in India, expanding their presence in the country’s energy sector.

- Siemens AG acquired a leading boiler technology provider to enhance its portfolio of energy-efficient solutions and strengthen its position in the global energy market.

- Mitsubishi Heavy Industries expanded its production capacity for Circulating Fluidized Bed (CFB) Boilers to meet the growing demand for cleaner energy solutions.

- Doosan Heavy Industries secured a contract to supply biomass boilers for a power plant in Europe, reinforcing its commitment to renewable energy projects.

- Bharat Heavy Electricals Limited (BHEL) was awarded a contract for supplying supercritical boilers to a large power project in India, aligning with India’s energy efficiency goals.

List of Leading Companies:

- General Electric (GE)

- Siemens AG

- Babcock & Wilcox Enterprises, Inc.

- Andritz AG

- Mitsubishi Heavy Industries

- Doosan Heavy Industries & Construction

- Foster Wheeler

- Alstom Power

- Toshiba Corporation

- Hitachi Ltd.

- Thermax Ltd.

- IHI Corporation

- Bharat Heavy Electricals Limited (BHEL)

- Aalborg Engineering

- Sumitomo SHI FW

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 44.2 Billion |

|

Forecasted Value (2030) |

USD 65.1 Billion |

|

CAGR (2025 – 2030) |

6.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Utility Boiler Market By Product Type (Pulverized Coal Boiler, Fluidized Bed Boiler, Circulating Fluidized Bed Boiler), By Fuel Type (Coal, Natural Gas, Oil, Biomass), By End-Use Industry (Power Generation, Oil & Gas, Chemical Processing, Paper & Pulp), By Capacity (Below 100 MW, 100 MW - 500 MW, Above 500 MW) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

General Electric (GE), Siemens AG, Babcock & Wilcox Enterprises, Inc., Andritz AG, Mitsubishi Heavy Industries, Doosan Heavy Industries & Construction, Foster Wheeler, Alstom Power, Toshiba Corporation, Hitachi Ltd., Thermax Ltd., IHI Corporation, Bharat Heavy Electricals Limited (BHEL), Aalborg Engineering, Sumitomo SHI FW |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Utility Boiler Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Pulverized Coal Boiler |

|

4.2. Fluidized Bed Boiler |

|

4.3. Circulating Fluidized Bed Boiler |

|

4.4. Others |

|

5. Utility Boiler Market, by Fuel Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Coal |

|

5.2. Natural Gas |

|

5.3. Oil |

|

5.4. Biomass |

|

5.5. Others |

|

6. Utility Boiler Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Power Generation |

|

6.2. Oil & Gas |

|

6.3. Chemical Processing |

|

6.4. Paper & Pulp |

|

6.5. Others |

|

7. Utility Boiler Market, by Capacity (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Below 100 MW |

|

7.2. 100 MW - 500 MW |

|

7.3. Above 500 MW |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Utility Boiler Market, by Type |

|

8.2.7. North America Utility Boiler Market, by Fuel Type |

|

8.2.8. North America Utility Boiler Market, by End-Use Industry |

|

8.2.9. North America Utility Boiler Market, by Capacity |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Utility Boiler Market, by Type |

|

8.2.10.1.2. US Utility Boiler Market, by Fuel Type |

|

8.2.10.1.3. US Utility Boiler Market, by End-Use Industry |

|

8.2.10.1.4. US Utility Boiler Market, by Capacity |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. General Electric (GE) |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Siemens AG |

|

10.3. Babcock & Wilcox Enterprises, Inc. |

|

10.4. Andritz AG |

|

10.5. Mitsubishi Heavy Industries |

|

10.6. Doosan Heavy Industries & Construction |

|

10.7. Foster Wheeler |

|

10.8. Alstom Power |

|

10.9. Toshiba Corporation |

|

10.10. Hitachi Ltd. |

|

10.11. Thermax Ltd. |

|

10.12. IHI Corporation |

|

10.13. Bharat Heavy Electricals Limited (BHEL) |

|

10.14. Aalborg Engineering |

|

10.15. Sumitomo SHI FW |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Utility Boiler Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Utility Boiler Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Utility Boiler Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA