As per Intent Market Research, the Uterine Fibroids Treatment Drugs Market was valued at USD 1.7 billion in 2024-e and will surpass USD 3.0 billion by 2030; growing at a CAGR of 8.3% during 2025 - 2030.

The uterine fibroids treatment drugs market is growing as more women seek non-invasive and effective treatments for managing uterine fibroids. Uterine fibroids are benign tumors that develop in the uterus, causing symptoms such as heavy menstrual bleeding, pelvic pain, and reproductive issues. The demand for uterine fibroids treatment drugs is rising as more women seek alternatives to invasive surgical procedures like hysterectomy. With advancements in medical research and drug development, treatments are evolving to offer women effective solutions with fewer side effects.

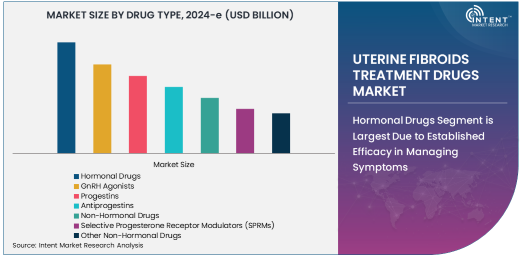

The market is characterized by a range of drug types, including hormonal and non-hormonal treatments, each catering to different needs. Hormonal drugs such as GnRH agonists and progestins have been widely used, while non-hormonal drugs like selective progesterone receptor modulators (SPRMs) are gaining popularity for their ability to manage symptoms without the side effects associated with hormonal treatments. The market is also seeing the emergence of non-surgical treatments that offer patients an alternative to surgery, contributing to the overall growth of the uterine fibroids treatment drug market.

Hormonal Drugs Segment is Largest Due to Established Efficacy in Managing Symptoms

The hormonal drugs segment is the largest in the uterine fibroids treatment drugs market, primarily due to their established efficacy in managing symptoms associated with uterine fibroids. GnRH agonists and progestins are commonly prescribed to help reduce the size of fibroids and alleviate symptoms such as heavy menstrual bleeding and pelvic pain. GnRH agonists work by reducing estrogen production, leading to a temporary menopause-like state that shrinks the fibroids. Progestins, on the other hand, help regulate menstrual bleeding and reduce pain.

Despite potential side effects, such as hot flashes and bone density loss associated with GnRH agonists, these hormonal drugs remain a cornerstone in uterine fibroid treatment due to their effectiveness in controlling symptoms. Hormonal treatments are often used in combination with other therapies, such as surgery or non-hormonal drugs, to optimize outcomes for patients. The availability of these treatments in both oral and injectable forms also provides flexibility for patients, further solidifying the hormonal drugs segment as the dominant player in the market.

Non-Hormonal Drugs Segment Is Fastest Growing Due to Preference for Fewer Side Effects

The non-hormonal drugs segment is the fastest-growing in the uterine fibroids treatment drugs market, driven by a growing preference for treatments with fewer side effects compared to hormonal drugs. Selective progesterone receptor modulators (SPRMs) are a key player in this segment, offering a non-hormonal approach to managing uterine fibroids. These drugs work by blocking the effects of progesterone on the fibroids, reducing their size and alleviating symptoms like heavy bleeding and pelvic pain. SPRMs have gained popularity due to their effectiveness in shrinking fibroids without the hormonal side effects associated with traditional treatments.

The increasing demand for non-hormonal drugs is driven by the need for alternatives to hormonal therapies, particularly among women who may experience adverse effects from hormonal treatments, such as mood swings or weight gain. The ability to offer targeted treatment without systemic hormonal impact is propelling the growth of the non-hormonal drugs segment. As more research is conducted into the efficacy and safety of non-hormonal treatments, this segment is expected to see continued growth, with an increasing number of women opting for these drugs as part of their treatment regimens.

Hospitals Lead as the Largest End-User Segment Due to Comprehensive Care and Access to Advanced Therapies

Hospitals are the largest end-user segment in the uterine fibroids treatment drugs market, owing to their ability to provide comprehensive care for women with uterine fibroids. Hospitals offer a wide range of treatment options, including medical management with drugs, surgical procedures, and non-surgical interventions. In addition to being equipped with advanced diagnostic tools and experienced healthcare professionals, hospitals are typically the first point of contact for women seeking treatment for uterine fibroids.

The demand for uterine fibroids treatment drugs in hospitals is driven by the high volume of patients seeking both conservative and invasive treatments. Hospitals are also at the forefront of offering the latest drug therapies, including hormonal and non-hormonal treatments, which are often combined with other treatment methods like surgery or non-invasive procedures. As hospitals continue to provide comprehensive treatment options, they will remain the dominant setting for uterine fibroids treatment.

Online Pharmacies Segment Is Fastest Growing Distribution Channel Due to Increased Convenience and Accessibility

The online pharmacies segment is the fastest-growing distribution channel in the uterine fibroids treatment drugs market, driven by the increasing demand for convenient and accessible healthcare solutions. Online pharmacies allow patients to easily access medications, including hormonal and non-hormonal treatments for uterine fibroids, from the comfort of their homes. This distribution channel offers several advantages, such as doorstep delivery, price comparisons, and the convenience of ordering without the need to visit a physical pharmacy.

The rise of e-commerce platforms and telemedicine services has made it easier for patients to obtain treatment for uterine fibroids through online pharmacies. Patients who require long-term medication management, such as GnRH agonists or SPRMs, often prefer online pharmacies for their ease of use and convenience. With growing consumer adoption of online healthcare services, the online pharmacies segment is expected to continue expanding, contributing significantly to the growth of the uterine fibroids treatment drugs market.

North America Leads the Uterine Fibroids Treatment Drugs Market Due to Advanced Healthcare Infrastructure and High Awareness

North America holds the largest share in the uterine fibroids treatment drugs market, primarily due to its advanced healthcare infrastructure, high awareness levels, and access to cutting-edge medical treatments. The United States, in particular, has a well-established healthcare system that offers a wide range of treatment options for uterine fibroids, including medications and surgical procedures. Moreover, high levels of awareness about uterine fibroids and their symptoms have led to increased diagnosis and demand for effective treatments.

The region’s focus on women’s health, combined with ongoing research into uterine fibroids and their treatment, is further driving market growth. North America is also home to numerous pharmaceutical companies that develop and market uterine fibroids treatment drugs, ensuring that patients have access to the latest therapies. As awareness continues to rise and treatment options evolve, North America is expected to maintain its dominant position in the uterine fibroids treatment drugs market.

Competitive Landscape: Leading Companies Focus on Innovation and Expanding Treatment Options

The uterine fibroids treatment drugs market is competitive, with several major pharmaceutical companies leading the way in the development of new and innovative therapies. Companies such as AbbVie, Bayer, and Myovant Sciences are at the forefront of research and drug development for uterine fibroids, focusing on improving the efficacy and safety of treatments. These companies are expanding their portfolios to include both hormonal and non-hormonal drugs, aiming to offer a wide range of treatment options for patients.

The competitive landscape is also characterized by ongoing clinical trials and partnerships with research institutions to accelerate the development of novel therapies. As the market continues to grow, pharmaceutical companies are focusing on innovation, aiming to provide patients with more effective, less invasive, and personalized treatment options for managing uterine fibroids. With the rising demand for alternative treatments, competition in the uterine fibroids treatment drugs market is expected to intensify, driving further advancements in drug development.

Recent Developments:

- In December 2024, AbbVie announced a new clinical trial for its SPRM-based drug for treating uterine fibroids, showing promising early results in reducing fibroid size.

- In November 2024, Bayer AG launched a new hormonal treatment option for uterine fibroids, receiving positive feedback from medical professionals for its efficacy.

- In October 2024, Merck & Co. received regulatory approval for its GnRH agonist treatment for uterine fibroids, marking a key milestone in non-surgical fibroid treatment.

- In September 2024, Gedeon Richter expanded its portfolio with a new medication aimed at managing symptoms of uterine fibroids, expected to be available by early 2025.

- In August 2024, HRA Pharma announced a partnership to bring a new non-hormonal drug for uterine fibroid treatment to market, focusing on non-invasive options for patients.

List of Leading Companies:

- AbbVie Inc.

- Bayer AG

- Merck & Co., Inc.

- Pfizer Inc.

- AstraZeneca

- Gedeon Richter

- HRA Pharma

- Novartis International AG

- Eli Lilly and Co.

- Sanofi

- Ferring Pharmaceuticals

- Takeda Pharmaceutical Company

- Johnson & Johnson

- Endo International

- Mitsubishi Tanabe Pharma

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.7 Billion |

|

Forecasted Value (2030) |

USD 3.0 Billion |

|

CAGR (2025 – 2030) |

8.3% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Uterine Fibroids Treatment Drugs Market by Drug Type (Hormonal Drugs, GnRH Agonists, Progestins, Antiprogestins, Non-Hormonal Drugs, Selective Progesterone Receptor Modulators (SPRMs), Other Non-Hormonal Drugs), Treatment Method (Medication-Based Treatments, Surgical Treatments, Non-Surgical Treatments), End-User (Hospitals, Clinics, Ambulatory Surgical Centers), Distribution Channel (Direct Sales, Pharmacies, Online Pharmacies) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

AbbVie Inc., Bayer AG, Merck & Co., Inc., Pfizer Inc., AstraZeneca, Gedeon Richter, HRA Pharma, Novartis International AG, Eli Lilly and Co., Sanofi, Ferring Pharmaceuticals, Takeda Pharmaceutical Company, Johnson & Johnson, Endo International, Mitsubishi Tanabe Pharma |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Uterine Fibroids Treatment Drugs Market, by Drug Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Hormonal Drugs |

|

4.2. GnRH Agonists |

|

4.3. Progestins |

|

4.4. Antiprogestins |

|

4.5. Non-Hormonal Drugs |

|

4.6. Selective Progesterone Receptor Modulators (SPRMs) |

|

4.7. Other Non-Hormonal Drugs |

|

5. Uterine Fibroids Treatment Drugs Market, by Treatment Method (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Medication-Based Treatments |

|

5.2. Surgical Treatments |

|

5.3. Non-Surgical Treatments |

|

6. Uterine Fibroids Treatment Drugs Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals |

|

6.2. Clinics |

|

6.3. Ambulatory Surgical Centers |

|

7. Uterine Fibroids Treatment Drugs Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Direct Sales |

|

7.2. Pharmacies |

|

7.3. Online Pharmacies |

|

7.4. Others |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Uterine Fibroids Treatment Drugs Market, by Drug Type |

|

8.2.7. North America Uterine Fibroids Treatment Drugs Market, by Treatment Method |

|

8.2.8. North America Uterine Fibroids Treatment Drugs Market, by End-User |

|

8.2.9. North America Uterine Fibroids Treatment Drugs Market, by Distribution Channel |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Uterine Fibroids Treatment Drugs Market, by Drug Type |

|

8.2.10.1.2. US Uterine Fibroids Treatment Drugs Market, by Treatment Method |

|

8.2.10.1.3. US Uterine Fibroids Treatment Drugs Market, by End-User |

|

8.2.10.1.4. US Uterine Fibroids Treatment Drugs Market, by Distribution Channel |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. AbbVie Inc. |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Bayer AG |

|

10.3. Merck & Co., Inc. |

|

10.4. Pfizer Inc. |

|

10.5. AstraZeneca |

|

10.6. Gedeon Richter |

|

10.7. HRA Pharma |

|

10.8. Novartis International AG |

|

10.9. Eli Lilly and Co. |

|

10.10. Sanofi |

|

10.11. Ferring Pharmaceuticals |

|

10.12. Takeda Pharmaceutical Company |

|

10.13. Johnson & Johnson |

|

10.14. Endo International |

|

10.15. Mitsubishi Tanabe Pharma |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Uterine Fibroids Treatment Drugs Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Uterine Fibroids Treatment Drugs Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Uterine Fibroids Treatment Drugs Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA