As per Intent Market Research, the Urinalysis Market was valued at USD 5.0 billion in 2024-e and will surpass USD 9.7 billion by 2030; growing at a CAGR of 11.8% during 2025 - 2030.

The urinalysis market has experienced steady growth due to the increasing prevalence of chronic conditions like diabetes, renal diseases, and urinary tract infections (UTIs), which require routine monitoring and diagnosis. Urinalysis is one of the most common diagnostic tests used for detecting various diseases and conditions, as it provides valuable insights into a patient's health status through the analysis of urine samples. The market is driven by advancements in testing technologies and the increasing adoption of point-of-care diagnostics, which offer rapid results and enhanced patient convenience.

As healthcare systems worldwide focus on early disease detection and preventive care, the demand for urinalysis products continues to rise. Urinalysis tests are used in multiple applications, including diabetes monitoring, UTI testing, renal disease diagnosis, and pregnancy testing, among others. Additionally, the growing number of outpatient visits, increased awareness about regular health screenings, and rising healthcare costs contribute to the expansion of the market. With technological improvements and innovations in urine testing devices and reagents, the market is poised for further growth, meeting the need for efficient, non-invasive diagnostic solutions.

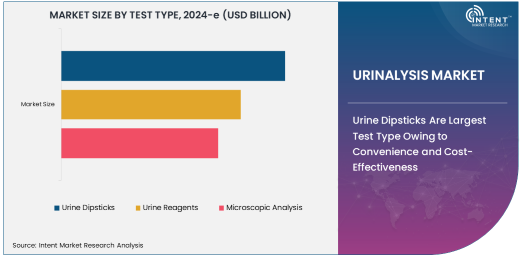

Urine Dipsticks Are Largest Test Type Owing to Convenience and Cost-Effectiveness

Urine dipsticks are the largest segment in the urinalysis market, primarily due to their convenience, ease of use, and cost-effectiveness. These diagnostic tools allow for quick and accurate testing of various parameters, such as glucose, protein, pH, blood, and other substances in the urine. Urine dipsticks are commonly used in both clinical and home settings for the screening of diseases like diabetes, kidney disorders, and UTIs. Their simplicity and low cost make them the preferred choice for initial screenings and routine health check-ups.

The widespread use of urine dipsticks is also fueled by their accessibility and the ability to provide rapid results without the need for specialized equipment or laboratory facilities. This makes them highly popular for both at-home use and in urgent care settings, where fast results are necessary. Furthermore, urine dipsticks are essential tools in the monitoring of chronic conditions such as diabetes and hypertension, where regular testing is required to assess disease progression or response to treatment. Their continued demand is expected to keep them at the forefront of the urinalysis market.

Urine Reagents Are Fastest Growing Test Type Owing to Technological Advancements

Urine reagents represent the fastest-growing test type in the urinalysis market, driven by the continuous advancements in reagent technology, which offer higher precision and more comprehensive testing capabilities. These reagents, which are used in conjunction with automated analyzers or manual testing systems, help detect a wide array of substances in the urine, including glucose, ketones, and proteins, that are indicative of various diseases such as diabetes and kidney failure. The growth of urine reagents is also supported by the increasing demand for high-quality diagnostic testing in both clinical and point-of-care settings.

Recent innovations in reagent formulations have enhanced their sensitivity and specificity, enabling more accurate diagnoses of conditions like UTIs, renal diseases, and metabolic disorders. As healthcare providers and patients increasingly prioritize accurate and timely diagnostics, the demand for urine reagents has grown significantly. The market for urine reagents is particularly strong in settings where high throughput and precision are crucial, such as hospitals and diagnostic laboratories, which expect fast and reliable results from their testing equipment.

Diabetes Monitoring Is Largest Application Owing to High Prevalence of Diabetes

Diabetes monitoring is the largest application segment in the urinalysis market, driven by the high global prevalence of diabetes and the need for regular monitoring of glucose levels in patients. Urinalysis plays a critical role in diabetes management, as the presence of glucose or ketones in the urine can be an early indicator of uncontrolled blood sugar levels. As diabetes rates continue to rise, particularly in aging populations and developing countries, the demand for reliable and cost-effective monitoring tools like urine dipsticks and urine reagents has increased.

The ease of use and affordability of urine tests for diabetes monitoring make them a popular choice for both patients and healthcare providers. With an increasing emphasis on home care and self-monitoring, patients with diabetes are turning to urine-based tests to track their condition and avoid complications. Moreover, the growing awareness of the link between urine glucose levels and long-term health outcomes has driven healthcare systems to incorporate routine urinalysis testing into diabetes management protocols. The continued expansion of this segment is expected to dominate the market due to the global diabetes epidemic.

Hospitals and Clinics Are Largest End-User Segment Owing to High Demand for Routine Diagnostics

Hospitals and clinics are the largest end-users of urinalysis products, as these healthcare facilities conduct routine diagnostic tests for a wide range of conditions, including diabetes, UTIs, renal diseases, and pregnancy. These institutions perform a significant volume of urinalysis tests as part of regular health screenings, pre-surgical assessments, and patient management. The increasing patient population, especially among those with chronic conditions, has led to a higher demand for urinalysis services in hospitals and clinics.

In hospitals, urinalysis is often used in conjunction with other diagnostic tests to confirm or rule out a variety of diseases, and it is a key part of the diagnostic workflow for conditions such as kidney disease and urinary tract infections. The availability of advanced diagnostic equipment and trained laboratory personnel in hospitals further supports the dominance of this end-user segment. With the rising demand for diagnostics in both outpatient and inpatient settings, hospitals and clinics remain the primary consumers of urinalysis products, ensuring continued growth in this segment.

North America Is the Largest Region Owing to Advanced Healthcare Infrastructure and High Diagnosis Rates

North America holds the largest share of the urinalysis market, largely due to its advanced healthcare infrastructure, high diagnosis rates, and widespread access to diagnostic testing. The U.S. and Canada are major contributors to this growth, as they have well-established healthcare systems with robust hospital and clinic networks that routinely conduct urinalysis for various medical conditions. The high prevalence of chronic diseases such as diabetes, kidney disorders, and UTIs in the region further drives the demand for urinalysis products, as they are essential for ongoing disease management and early detection.

The region also benefits from significant investments in healthcare technology, including automated urinalysis systems that provide faster, more accurate results. Additionally, North America has a strong culture of preventative healthcare and health monitoring, which further supports the adoption of urinalysis testing across different patient demographics. With a growing focus on early diagnosis and chronic disease management, North America is expected to maintain its position as the largest and most lucrative market for urinalysis products.

Competitive Landscape: Key Players and Product Innovations

The urinalysis market is highly competitive, with leading companies such as Roche Diagnostics, Abbott Laboratories, Siemens Healthineers, and Thermo Fisher Scientific dominating the market. These companies offer a wide range of products, including urine dipsticks, reagents, and automated analyzers, and focus on innovations that improve the accuracy, efficiency, and convenience of urinalysis tests. Product developments such as enhanced reagent formulations, integrated testing platforms, and point-of-care diagnostic solutions are becoming increasingly common as companies strive to meet the growing demand for reliable and timely testing.

The competitive landscape also includes several smaller regional players that focus on niche product offerings, such as specialized urine testing kits or point-of-care devices. As the market continues to evolve, companies are investing in research and development to introduce new and improved products that cater to both clinical and home care settings. Partnerships, acquisitions, and collaborations between diagnostic companies, healthcare providers, and research institutions are expected to play a key role in the expansion of the urinalysis market, leading to continued innovation and market growth.

Recent Developments:

- In December 2024, Roche Diagnostics launched a new automated urinalysis system designed to improve test accuracy and speed.

- In November 2024, Abbott Laboratories received FDA approval for their latest urine reagent strip designed for home use in diabetes management.

- In October 2024, Siemens Healthineers expanded its urinalysis product range with the introduction of a new test panel for renal disease detection.

- In September 2024, Thermo Fisher Scientific announced a partnership with Bio-Rad Laboratories to co-develop advanced diagnostic tools for urinalysis.

- In August 2024, BD unveiled a new urine collection device aimed at improving the accuracy of UTI diagnostics in clinical settings.

List of Leading Companies:

- Siemens Healthineers

- Roche Diagnostics

- Abbott Laboratories

- Thermo Fisher Scientific

- BD (Becton, Dickinson and Company)

- Arkray, Inc.

- F. Hoffmann-La Roche AG

- Quidel Corporation

- LabCorp

- Urineology

- Bio-Rad Laboratories

- Acon Laboratories, Inc.

- Fisher Scientific

- Trividia Health, Inc.

- Medtronic PLC

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 5.0 billion |

|

Forecasted Value (2030) |

USD 9.7 billion |

|

CAGR (2025 – 2030) |

11.8% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Urinalysis Market By Test Type (Urine Dipsticks, Urine Reagents, Microscopic Analysis), By Application (Diabetes Monitoring, Urinary Tract Infections (UTI) Testing, Renal Disease Diagnosis, Pregnancy Testing), By End-User (Hospitals and Clinics, Diagnostic Laboratories, Home Care Settings) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Siemens Healthineers, Roche Diagnostics, Abbott Laboratories, Thermo Fisher Scientific, BD (Becton, Dickinson and Company), Arkray, Inc., F. Hoffmann-La Roche AG, Quidel Corporation, LabCorp, Urineology, Bio-Rad Laboratories, Acon Laboratories, Inc., Fisher Scientific, Trividia Health, Inc., Medtronic PLC |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Urinalysis Market, by Test Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Urine Dipsticks |

|

4.2. Urine Reagents |

|

4.3. Microscopic Analysis |

|

5. Urinalysis Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Diabetes Monitoring |

|

5.2. Urinary Tract Infections (UTI) Testing |

|

5.3. Renal Disease Diagnosis |

|

5.4. Pregnancy Testing |

|

6. Urinalysis Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals and Clinics |

|

6.2. Diagnostic Laboratories |

|

6.3. Home Care Settings |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Urinalysis Market, by Test Type |

|

7.2.7. North America Urinalysis Market, by Application |

|

7.2.8. North America Urinalysis Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Urinalysis Market, by Test Type |

|

7.2.9.1.2. US Urinalysis Market, by Application |

|

7.2.9.1.3. US Urinalysis Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Siemens Healthineers |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Roche Diagnostics |

|

9.3. Abbott Laboratories |

|

9.4. Thermo Fisher Scientific |

|

9.5. BD (Becton, Dickinson and Company) |

|

9.6. Arkray, Inc. |

|

9.7. F. Hoffmann-La Roche AG |

|

9.8. Quidel Corporation |

|

9.9. LabCorp |

|

9.10. Urineology |

|

9.11. Bio-Rad Laboratories |

|

9.12. Acon Laboratories, Inc. |

|

9.13. Fisher Scientific |

|

9.14. Trividia Health, Inc. |

|

9.15. Medtronic PLC |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Urinalysis Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Urinalysis Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Urinalysis Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA