As per Intent Market Research, the Transparent Plastics Market was valued at USD 17.6 billion in 2024-e and will surpass USD 33.1 billion by 2030; growing at a CAGR of 9.5% during 2025 - 2030.

The transparent plastics market has emerged as a critical segment in the global plastics industry, driven by the material’s versatility, lightweight nature, and superior optical properties. Transparent plastics are widely used across diverse sectors such as packaging, automotive, healthcare, and electronics, owing to their excellent clarity, impact resistance, and ease of processing. As industries shift towards lightweight and durable materials, the demand for transparent plastics is set to grow exponentially.

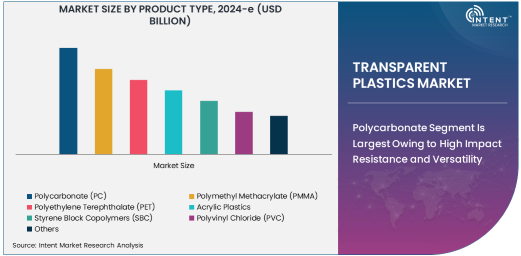

Polycarbonate Segment Is Largest Owing to High Impact Resistance and Versatility

Polycarbonate (PC) dominates the transparent plastics market due to its exceptional impact resistance, high thermal stability, and clarity, making it a preferred choice in demanding applications. Widely used in automotive components, electronics, and construction, polycarbonate offers unmatched performance under high-stress conditions.

The automotive industry heavily relies on polycarbonate for headlamps, sunroofs, and glazing applications, where strength and transparency are critical. Furthermore, the electronics sector leverages polycarbonate for its optical clarity and flame resistance in products such as housings for consumer electronics and LED lighting systems.

Packaging Segment Is Fastest Growing Owing to Rising Sustainability Trends

The packaging segment is experiencing rapid growth in the transparent plastics market, fueled by the global demand for sustainable, lightweight, and recyclable materials. Transparent plastics such as PET and acrylic are extensively used for food, beverage, and pharmaceutical packaging, offering superior aesthetics and product protection.

The increasing preference for clear packaging to enhance product visibility and the adoption of bio-based transparent plastics are key drivers in this sector. The food and beverage industry, in particular, has seen a surge in the use of PET due to its recyclability and compliance with food safety standards.

Healthcare Industry Is Fastest Growing Owing to Demand for Sterile and Durable Materials

The healthcare industry is emerging as the fastest-growing end-user segment, driven by the rising demand for transparent plastics in medical devices, surgical instruments, and diagnostic tools. Materials like PMMA and PVC are highly sought after for their clarity, biocompatibility, and ability to be sterilized.

Applications in syringes, IV tubing, and diagnostic equipment have bolstered the use of transparent plastics in healthcare. The growing emphasis on hygiene and safety in medical practices, coupled with advancements in bio-based plastics, further amplifies this trend.

Rigid Transparent Plastics Segment Is Largest Owing to Structural Integrity and Versatility

Rigid transparent plastics hold the largest share in the market due to their structural integrity and wide range of applications. These plastics, including PC and PMMA, are extensively used in automotive components, construction materials, and consumer goods that demand durability and optical clarity.

In construction, rigid transparent plastics are favored for skylights, safety windows, and partition walls, where strength and transparency are essential. The segment's dominance is underpinned by its ability to balance performance with aesthetics in diverse industrial applications.

Asia-Pacific Is Largest Region Owing to Industrialization and Growing Consumer Base

Asia-Pacific leads the transparent plastics market, accounting for the largest regional share due to rapid industrialization, urbanization, and a burgeoning middle class. Countries like China and India are major contributors, driven by demand from the automotive, packaging, and electronics industries.

The region’s manufacturing hub status, coupled with increasing investments in infrastructure and healthcare, further propels the market. Government initiatives promoting sustainability and the adoption of bio-based plastics also play a crucial role in the region's dominance.

Leading Companies and Competitive Landscape

The transparent plastics market features intense competition, with key players like BASF SE, Covestro AG, SABIC, and Dow Inc. leading the industry. These companies focus on innovation, sustainability, and strategic partnerships to strengthen their market presence. Recent trends include the development of bio-based and recyclable transparent plastics, addressing environmental concerns and regulatory mandates.

Collaborations with end-user industries, advancements in manufacturing technologies, and geographic expansion are defining strategies among competitors. The competitive landscape is further shaped by the growing emphasis on circular economy practices and customer-specific product solutions.

Recent Developments:

- BASF SE launched an advanced optical grade polycarbonate aimed at healthcare applications.

- Covestro AG announced a collaboration with a sustainable packaging firm to produce bio-based transparent plastics.

- Dow Inc. expanded its product portfolio with innovative PMMA solutions for automotive applications.

- SABIC completed the acquisition of a regional manufacturer to strengthen its position in Asia's transparent plastics market.

- Arkema SA secured regulatory approval for a new production plant focusing on high-performance transparent plastics.

List of Leading Companies:

- BASF SE

- Covestro AG

- SABIC

- Dow Inc.

- Arkema SA

- Evonik Industries AG

- LyondellBasell Industries Holdings B.V.

- Eastman Chemical Company

- Trinseo S.A.

- Mitsubishi Chemical Holdings Corporation

- Röhm GmbH

- Asahi Kasei Corporation

- Teijin Limited

- LG Chem Ltd.

- Toray Industries

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 17.6 Billion |

|

Forecasted Value (2030) |

USD 33.1 Billion |

|

CAGR (2025 – 2030) |

9.5% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Transparent Plastics Market by Product Type (Polycarbonate, Polymethyl Methacrylate, Polyethylene Terephthalate, Acrylic Plastics, Styrene Block Copolymers, Polyvinyl Chloride), Application (Packaging, Building & Construction, Automotive Components, Consumer Goods, Electronics, Medical Devices), End-User Industry (Automotive, Healthcare, Electronics, Packaging, Construction, Industrial), and Form (Rigid Transparent Plastics, Flexible Transparent Plastics) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

BASF SE, Covestro AG, SABIC, Dow Inc., Arkema SA, Evonik Industries AG, LyondellBasell Industries Holdings B.V., Eastman Chemical Company, Trinseo S.A., Mitsubishi Chemical Holdings Corporation, Röhm GmbH, Asahi Kasei Corporation, Teijin Limited, LG Chem Ltd., Toray Industries |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Transparent Plastics Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Polycarbonate (PC) |

|

4.2. Polymethyl Methacrylate (PMMA) |

|

4.3. Polyethylene Terephthalate (PET) |

|

4.4. Acrylic Plastics |

|

4.5. Styrene Block Copolymers (SBC) |

|

4.6. Polyvinyl Chloride (PVC) |

|

4.7. Others |

|

5. Transparent Plastics Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Packaging |

|

5.2. Building & Construction |

|

5.3. Automotive Components |

|

5.4. Consumer Goods |

|

5.5. Electronics |

|

5.6. Medical Devices |

|

5.7. Others |

|

6. Transparent Plastics Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Automotive |

|

6.2. Healthcare |

|

6.3. Electronics |

|

6.4. Packaging |

|

6.5. Construction |

|

7. Transparent Plastics Market, by Industrial (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8. Transparent Plastics Market, by Form (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Rigid Transparent Plastics |

|

8.2. Flexible Transparent Plastics |

|

8.3. Resin-based |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Transparent Plastics Market, by Product Type |

|

9.2.7. North America Transparent Plastics Market, by Application |

|

9.2.8. North America Transparent Plastics Market, by End-User Industry |

|

9.2.9. North America Transparent Plastics Market, by Industrial |

|

9.2.10. North America Transparent Plastics Market, by Form |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Transparent Plastics Market, by Product Type |

|

9.2.11.1.2. US Transparent Plastics Market, by Application |

|

9.2.11.1.3. US Transparent Plastics Market, by End-User Industry |

|

9.2.11.1.4. US Transparent Plastics Market, by Industrial |

|

9.2.11.1.5. US Transparent Plastics Market, by Form |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. BASF SE |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Covestro AG |

|

11.3. SABIC |

|

11.4. Dow Inc. |

|

11.5. Arkema SA |

|

11.6. Evonik Industries AG |

|

11.7. LyondellBasell Industries Holdings B.V. |

|

11.8. Eastman Chemical Company |

|

11.9. Trinseo S.A. |

|

11.10. Mitsubishi Chemical Holdings Corporation |

|

11.11. Röhm GmbH |

|

11.12. Asahi Kasei Corporation |

|

11.13. Teijin Limited |

|

11.14. LG Chem Ltd. |

|

11.15. Toray Industries |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Transparent Plastics Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Transparent Plastics Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Transparent Plastics Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA