As per Intent Market Research, the Thermosetting Plastics Market was valued at USD 14.8 billion in 2024-e and will surpass USD 26.5 billion by 2030; growing at a CAGR of 8.7% during 2025 - 2030.

Thermosetting plastics are a key category of polymers widely utilized across numerous industries for their excellent durability, heat resistance, and structural integrity. These plastics, which undergo a chemical change during curing, cannot be re-melted or reshaped, making them ideal for high-performance applications. The thermosetting plastics market continues to evolve with innovations in product types and applications, driven by demand for more efficient and sustainable materials. The market's expansion is particularly significant in automotive, aerospace, and electrical sectors, where performance and safety are paramount.

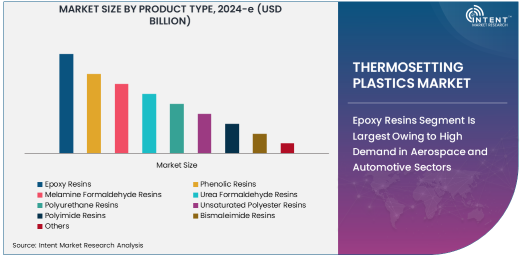

Epoxy Resins Segment Is Largest Owing to High Demand in Aerospace and Automotive Sectors

Epoxy resins are the largest subsegment in the thermosetting plastics market, primarily due to their superior adhesion properties, excellent chemical resistance, and thermal stability. They are widely used in automotive and aerospace manufacturing, where strength, safety, and durability are non-negotiable. Epoxy resins are extensively employed in producing composite materials, adhesives, coatings, and electrical insulation, making them integral to industries focused on high-performance materials.

The increasing adoption of epoxy resins is driven by their ability to enhance product longevity and provide solutions that meet stringent regulatory standards, particularly in the aerospace and automotive industries. Additionally, their widespread use in electrical insulation applications further contributes to the growth of the epoxy resins market, as the electronics sector requires robust, long-lasting materials for circuit boards and other components exposed to heat and chemicals.

Automotive Segment Is Fastest Growing Owing to Demand for Lightweight, Durable Components

The automotive industry represents the fastest-growing end-user segment in the thermosetting plastics market, with the increasing focus on lightweight yet durable materials. Thermosetting plastics, particularly epoxy resins, and polyurethane resins, are used extensively in automotive parts due to their strength, thermal stability, and ability to withstand harsh conditions. These plastics are key in making components such as bumpers, dashboard parts, and under-the-hood components, contributing to the automotive industry's push toward energy-efficient and fuel-saving solutions.

As electric vehicles (EVs) gain market share and manufacturers look for lightweight components to improve fuel efficiency and reduce emissions, the demand for thermosetting plastics, especially in automotive parts, is expected to grow rapidly. The need for advanced composites that offer better strength-to-weight ratios is particularly driving this trend, positioning the automotive sector as a pivotal player in the overall market growth.

Coatings Application Is Largest Owing to Demand for Durability and Aesthetics

Coatings represent the largest application subsegment in the thermosetting plastics market, with epoxy and polyurethane resins being the most commonly used materials. These coatings are essential for a variety of industries, including automotive, aerospace, and construction, where protective, aesthetic, and functional coatings are required to enhance product life and appearance. Thermosetting plastics are ideal for coatings due to their resistance to environmental stress, UV degradation, and abrasion, making them indispensable in high-demand applications such as industrial coatings and automotive finishes.

The coatings segment’s growth is also being fueled by the rise in demand for high-performance materials that can provide long-lasting protection in harsh environmental conditions. The development of coatings with superior scratch resistance and better performance in extreme temperatures is a key trend driving the adoption of thermosetting plastics in this area.

Liquid Form Segment Is Largest Owing to Ease of Application and Versatility

The liquid form of thermosetting plastics is the largest subsegment due to its versatility and ease of application in various industries. Liquid resins, particularly in the form of epoxy or polyurethane, can be easily applied and cured in molds, making them ideal for producing intricate parts and components. The liquid form is essential in industries such as automotive, aerospace, and electrical, where thermosetting plastics are used to create high-strength components and coatings that need to withstand extreme conditions.

Additionally, liquid thermosetting resins allow for better control over the curing process, making them a preferred choice for industries requiring precision in manufacturing. This ability to form complex shapes and structures without compromising on material integrity makes liquid thermosetting resins a critical material in the production of everything from automotive parts to electrical insulation components.

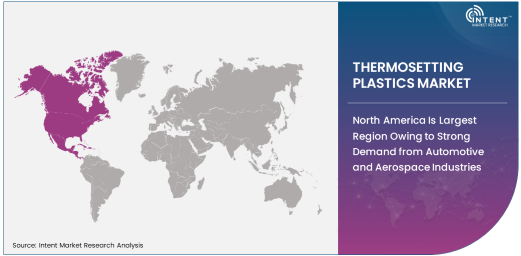

North America Is Largest Region Owing to Strong Demand from Automotive and Aerospace Industries

North America holds the largest share of the thermosetting plastics market, driven by the strong presence of industries such as automotive, aerospace, and electrical. The United States, in particular, remains a global leader in the demand for high-performance materials used in manufacturing lightweight, durable, and heat-resistant parts. The aerospace sector’s reliance on thermosetting plastics for composite materials, coatings, and insulation further supports the market's expansion in the region.

The increasing focus on electric vehicle (EV) production and the rapid development of fuel-efficient, high-performance automotive parts have further accelerated the adoption of thermosetting plastics in North America. With established regulatory frameworks supporting sustainability and innovation, the region continues to dominate the market, and this trend is expected to continue over the forecast period.

Leading Companies and Competitive Landscape

The thermosetting plastics market is highly competitive, with several key players leading the industry in terms of product innovation, quality, and market presence. Companies such as BASF SE, Huntsman International LLC, and Dow Chemical Company dominate the market, offering a wide range of thermosetting resin products used across various industries. These companies are focused on expanding their product portfolios through research and development, partnerships, and acquisitions to meet the growing demand for advanced materials in automotive, aerospace, and electrical sectors.

The competitive landscape is characterized by ongoing investments in new technologies and innovations aimed at improving the performance and sustainability of thermosetting plastics. As industries increasingly demand materials that are both high-performance and eco-friendly, companies are exploring bio-based alternatives and more sustainable production methods to stay ahead in the market. Moreover, the rise in electric vehicles and advancements in aerospace technology are expected to fuel the competition among players, driving continuous product improvements and market expansion

Recent Developments:

- Huntsman International launched a new line of thermosetting resins aimed at improving the performance of automotive composites, enhancing durability and impact resistance.

- SABIC introduced a series of high-performance thermosetting resins designed for use in aerospace and automotive applications, with an emphasis on lightweight and energy-efficient solutions.

- Covestro AG announced the acquisition of a thermoset resin technology company, expanding its portfolio of advanced materials for automotive and industrial applications.

- Momentive Performance Materials collaborated with major automotive manufacturers to develop advanced thermoset composites for electric vehicle battery housing, improving safety and thermal stability.

- Dow Chemical Company received regulatory approval for its new line of epoxy resins that meet sustainability goals while offering improved performance in industrial and electrical applications

List of Leading Companies:

- BASF SE

- Huntsman International LLC

- Momentive Performance Materials Inc.

- SABIC

- Dow Chemical Company

- Covestro AG

- LG Chem

- 3M Company

- DSM N.V.

- Polynt-Reichhold Group

- Arkema Group

- Celanese Corporation

- Hexcel Corporation

- Ineos Styrolution

- Sumitomo Bakelite Co

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 14.8 Billion |

|

Forecasted Value (2030) |

USD 26.5 Billion |

|

CAGR (2025 – 2030) |

8.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Thermosetting Plastics Market By Product Type (Epoxy Resins, Phenolic Resins, Melamine Formaldehyde Resins, Urea Formaldehyde Resins, Polyurethane Resins, Unsaturated Polyester Resins, Polyimide Resins, Bismaleimide Resins), By End-User Industry (Automotive, Electrical & Electronics, Aerospace, Construction, Industrial Equipment, Consumer Goods, Medical Devices, Packaging), By Application (Coatings, Adhesives, Composites, Electrical Insulation, Encapsulation, Laminates, Molded Components, Automotive Parts), By Form (Liquid, Powder, Granules, Sheet, Resin-based) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

BASF SE, Huntsman International LLC, Momentive Performance Materials Inc., SABIC, Dow Chemical Company, Covestro AG, LG Chem, 3M Company, DSM N.V., Polynt-Reichhold Group, Arkema Group, Celanese Corporation, Hexcel Corporation, Ineos Styrolution, Sumitomo Bakelite Co |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Thermosetting Plastics Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Epoxy Resins |

|

4.2. Phenolic Resins |

|

4.3. Melamine Formaldehyde Resins |

|

4.4. Urea Formaldehyde Resins |

|

4.5. Polyurethane Resins |

|

4.6. Unsaturated Polyester Resins |

|

4.7. Polyimide Resins |

|

4.8. Bismaleimide Resins |

|

4.9. Others |

|

5. Thermosetting Plastics Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Automotive |

|

5.2. Electrical & Electronics |

|

5.3. Aerospace |

|

5.4. Construction |

|

5.5. Industrial Equipment |

|

5.6. Consumer Goods |

|

5.7. Medical Devices |

|

5.8. Packaging |

|

6. Thermosetting Plastics Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Coatings |

|

6.2. Adhesives |

|

6.3. Composites |

|

6.4. Electrical Insulation |

|

6.5. Encapsulation |

|

6.6. Laminates |

|

6.7. Molded Components |

|

6.8. Automotive Parts |

|

7. Thermosetting Plastics Market, by Form (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Liquid |

|

7.2. Powder |

|

7.3. Granules |

|

7.4. Sheet |

|

7.5. Resin-based |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Thermosetting Plastics Market, by Product Type |

|

8.2.7. North America Thermosetting Plastics Market, by End-User Industry |

|

8.2.8. North America Thermosetting Plastics Market, by Application |

|

8.2.9. North America Thermosetting Plastics Market, by Form |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Thermosetting Plastics Market, by Product Type |

|

8.2.10.1.2. US Thermosetting Plastics Market, by End-User Industry |

|

8.2.10.1.3. US Thermosetting Plastics Market, by Application |

|

8.2.10.1.4. US Thermosetting Plastics Market, by Form |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. BASF SE |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Huntsman International LLC |

|

10.3. Momentive Performance Materials Inc. |

|

10.4. SABIC |

|

10.5. Dow Chemical Company |

|

10.6. Covestro AG |

|

10.7. LG Chem |

|

10.8. 3M Company |

|

10.9. DSM N.V. |

|

10.10. Polynt-Reichhold Group |

|

10.11. Arkema Group |

|

10.12. Celanese Corporation |

|

10.13. Hexcel Corporation |

|

10.14. Ineos Styrolution |

|

10.15. Sumitomo Bakelite Co |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Thermosetting Plastics Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Thermosetting Plastics Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Thermosetting Plastics Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA