As per Intent Market Research, the Surgical Robotics and Navigation for Orthopaedic Market was valued at USD 4.0 billion in 2023 and will surpass USD 11.4 billion by 2030; growing at a CAGR of 16.3% during 2024 - 2030.

The global surgical robotics and navigation for orthopaedic market is rapidly evolving, driven by advancements in technology, the increasing demand for minimally invasive surgeries, and the growing focus on precision and accuracy in orthopaedic procedures. These technologies are reshaping the way surgeries are performed, offering enhanced patient outcomes, faster recovery times, and reduced complications. The market is segmented by product type, technology, end-user, and application, with each segment contributing to the overall growth and transformation of the industry. This content delves into key subsegments within each category, highlighting the factors driving growth and market dynamics.

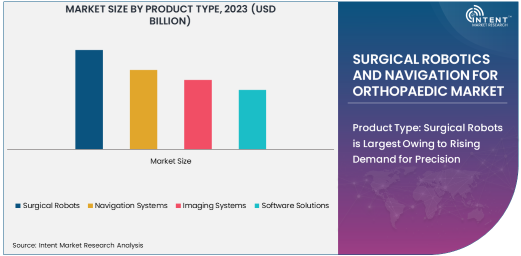

Product Type: Surgical Robots is Largest Owing to Rising Demand for Precision

Surgical robots represent the largest subsegment in the surgical robotics and navigation market, primarily due to their growing adoption in orthopaedic procedures. Robotic-assisted surgeries provide unparalleled precision and flexibility, which is critical for complex procedures such as joint replacement and spine surgeries. These systems allow for smaller incisions, reduced human error, and enhanced dexterity, all of which contribute to better patient outcomes and faster recovery times. Leading surgical robot systems like the da Vinci Surgical System and the Mako robotic system are driving significant market growth, offering advanced features such as real-time imaging, 3D visualization, and robotic arms that can perform delicate movements with high precision.

The demand for surgical robots has been accelerating as orthopaedic surgeons seek to improve the accuracy of their surgeries and reduce the invasiveness of traditional approaches. These systems are particularly valuable in joint replacement surgeries, where precision is essential to ensure proper alignment and prevent complications. As the technology becomes more affordable and accessible, more hospitals and surgical centers are investing in robotic-assisted systems, fueling further growth in this subsegment. This trend is expected to continue, as robotic surgeries gain widespread acceptance across orthopaedic specialties.

Technology: Robotic-Assisted Surgery is Fastest Growing Owing to Minimally Invasive Benefits

The robotic-assisted surgery technology segment is experiencing the fastest growth within the surgical robotics and navigation market, owing to its numerous advantages in minimally invasive procedures. Robotic-assisted surgery allows surgeons to perform highly precise movements using robotic arms controlled by a console, offering better control and flexibility compared to traditional manual techniques. The ability to perform minimally invasive surgeries with enhanced accuracy has led to the increasing adoption of robotic-assisted systems in orthopaedic surgeries, particularly in joint replacements and spine surgeries. Patients benefit from smaller incisions, less pain, shorter hospital stays, and quicker recovery times.

As robotic-assisted surgery technology continues to evolve, it is expected to become more integrated into a wider range of orthopaedic applications. The precision and efficiency offered by robotic-assisted systems are particularly appealing in complex surgeries, where the risk of complications is higher. Surgeons also appreciate the enhanced ergonomics and reduced physical strain when operating these systems, contributing to greater adoption rates. The continuous advancements in artificial intelligence (AI) and machine learning are further fueling the growth of this technology, enabling even more precise and personalized surgeries.

End User: Hospitals is Largest Due to High Adoption of Advanced Technologies

Hospitals are the largest end-user segment in the surgical robotics and navigation for orthopaedics market. The widespread adoption of advanced surgical robots and navigation systems by hospitals is driven by their ability to improve surgical outcomes, reduce recovery times, and lower complication rates. Hospitals, especially in developed regions, are increasingly investing in cutting-edge robotic systems to enhance the capabilities of their orthopaedic departments. These facilities are equipped with state-of-the-art robotic systems that allow surgeons to perform complex surgeries with greater accuracy and minimal invasiveness, appealing to patients who demand high-quality healthcare services.

The hospital segment continues to dominate due to the high volume of surgeries performed, particularly in urban settings where access to advanced medical technologies is prevalent. As the technology becomes more cost-effective and accessible, smaller hospitals are also adopting robotic systems to remain competitive and meet the growing demand for orthopaedic surgeries. The integration of robotic systems into hospital settings is improving patient care and contributing to the overall expansion of the market. Furthermore, hospitals are increasingly partnering with technology providers to incorporate robotic solutions into their surgical practices, driving further adoption in this segment.

Application: Joint Replacement is Largest Owing to Growing Aging Population

Joint replacement surgery is the largest application within the surgical robotics and navigation market, particularly for orthopaedics. The increasing incidence of osteoarthritis and other degenerative joint diseases, along with the aging global population, has driven significant growth in the demand for joint replacement surgeries. Robotic-assisted joint replacement surgeries offer significant advantages, including higher precision, better alignment, and improved long-term outcomes, which are particularly important in procedures like knee and hip replacements. These benefits make robotic systems highly attractive to both surgeons and patients.

As the demand for joint replacement surgeries continues to rise, particularly in aging populations across North America, Europe, and parts of Asia, robotic-assisted systems are becoming an essential part of orthopaedic practice. These surgeries benefit from enhanced accuracy in the placement of implants, leading to reduced complications such as dislocations or infections. The growing trend of personalized medicine, where surgeries are tailored to individual patient anatomy, is also supporting the adoption of robotic systems in joint replacement procedures. This segment is expected to continue driving the growth of the surgical robotics market for the foreseeable future.

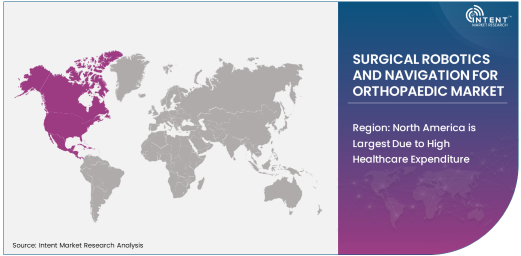

Region: North America is Largest Due to High Healthcare Expenditure

North America holds the largest market share for surgical robotics and navigation for orthopaedics, primarily driven by high healthcare expenditure, technological advancements, and widespread adoption of robotic-assisted surgeries in the region. The United States, in particular, is a key market, where hospitals and surgical centers are increasingly investing in robotic systems to enhance the quality and efficiency of orthopaedic surgeries. The presence of leading companies such as Intuitive Surgical, Stryker, and Medtronic, along with strong healthcare infrastructure, has further cemented North America's dominance in this market.

The region benefits from a well-established regulatory framework, high disposable incomes, and a large patient population with increasing healthcare needs. As robotic technology becomes more affordable and accessible, smaller hospitals and surgery centers are also adopting robotic systems, further expanding the market. Moreover, North America is home to a significant number of clinical trials and research initiatives focused on advancing surgical robotics, which contributes to ongoing innovation and growth in the market. This region is expected to maintain its leadership position in the global market due to continued investment in healthcare technologies and the growing demand for advanced surgical procedures.

Competitive Landscape: Leading Companies and Market Dynamics

The surgical robotics and navigation for orthopaedics market is highly competitive, with a mix of established medical device companies and emerging innovators. Leading players in this market include Intuitive Surgical, Stryker Corporation, Zimmer Biomet, Medtronic, and Johnson & Johnson, all of which offer advanced robotic and navigation systems for orthopaedic procedures. These companies dominate the market by providing a broad range of robotic solutions that cater to different surgical specialties, particularly in joint replacement, spine surgery, and trauma procedures.

Competition in this market is intensifying as companies focus on developing more advanced, cost-effective, and user-friendly robotic systems. Strategic collaborations, acquisitions, and partnerships are common, as companies seek to enhance their product portfolios and expand their market presence. Additionally, the growing trend of integrating AI and machine learning into robotic surgery systems is shaping the competitive landscape, enabling companies to offer more personalized and precise surgical solutions. With the market poised for continued growth, companies are investing heavily in research and development to stay ahead of technological advancements and meet the increasing demand for robotic-assisted surgeries.

Recent Developments:

- Medtronic Launches Spine Surgery Robotic System – Medtronic recently launched the Hugo™ robotic system for spine surgery, enhancing precision and reducing recovery time for patients.

- Stryker Acquires OrthAlign, Inc. – Stryker Corporation announced the acquisition of OrthAlign, Inc., a leader in portable, handheld navigation systems for orthopaedic surgeries, to expand its robotic surgery portfolio.

- Zimmer Biomet Rolls Out Personalized Joint Replacement Solution – Zimmer Biomet introduced a new robotic arm-assisted surgery system for joint replacement that integrates personalized pre-operative planning for better patient outcomes.

- Intuitive Surgical Expands Robotic Surgery Portfolio – Intuitive Surgical, known for its da Vinci systems, expanded its product offerings with additional applications for orthopaedic and spine surgeries.

- FDA Approves New Navigation System from Smith & Nephew – Smith & Nephew received FDA clearance for a new robotic-assisted navigation system for knee and hip arthroplasty, promising improved surgical accuracy.

List of Leading Companies:

- Intuitive Surgical

- Stryker Corporation

- Zimmer Biomet

- Medtronic PLC

- Johnson & Johnson (DePuy Synthes)

- Smith & Nephew

- Mazor Robotics (acquired by Medtronic)

- Corindus Vascular Robotics

- Think Surgical

- Blue Belt Technologies (acquired by Smith & Nephew)

- KUKA Robotics

- TransEnterix

- Robotic Surgery Technologies, Inc.

- OrthAlign, Inc.

- DJO Global (A Zimmer Biomet Company)

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 4.0 Billion |

|

Forecasted Value (2030) |

USD 11.4 Billion |

|

CAGR (2024 – 2030) |

16.3% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Surgical Robotics and Navigation for Orthopaedic Market By Product Type (Surgical Robots, Navigation Systems, Imaging Systems, Software Solutions), By Technology (Robotic-Assisted Surgery, Image-Guided Surgery, Minimally Invasive Surgery, Computer-Assisted Surgery), By End-User (Hospitals, Ambulatory Surgery Centers, Orthopaedic Clinics), By Application (Joint Replacement, Spine Surgery, Trauma Surgery, Sports Medicine, Reconstructive Surgery) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Intuitive Surgical, Stryker Corporation, Zimmer Biomet, Medtronic PLC, Johnson & Johnson (DePuy Synthes), Smith & Nephew, Mazor Robotics (acquired by Medtronic), Corindus Vascular Robotics, Think Surgical, Blue Belt Technologies (acquired by Smith & Nephew), KUKA Robotics, TransEnterix, Robotic Surgery Technologies, Inc., OrthAlign, Inc., DJO Global (A Zimmer Biomet Company) |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Surgical Robotics and Navigation for Orthopaedic Market, by Product Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Surgical Robots |

|

4.2. Navigation Systems |

|

4.3. Imaging Systems |

|

4.4. Software Solutions |

|

5. Surgical Robotics and Navigation for Orthopaedic Market, by Technology (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Robotic-Assisted Surgery |

|

5.2. Image-Guided Surgery |

|

5.3. Minimally Invasive Surgery |

|

5.4. Computer-Assisted Surgery |

|

6. Surgical Robotics and Navigation for Orthopaedic Market, by End User (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Hospitals |

|

6.2. Ambulatory Surgery Centers |

|

6.3. Orthopaedic Clinics |

|

7. Surgical Robotics and Navigation for Orthopaedic Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Joint Replacement |

|

7.2. Spine Surgery |

|

7.3. Trauma Surgery |

|

7.4. Sports Medicine |

|

7.5. Reconstructive Surgery |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Surgical Robotics and Navigation for Orthopaedic Market, by Product Type |

|

8.2.7. North America Surgical Robotics and Navigation for Orthopaedic Market, by Technology |

|

8.2.8. North America Surgical Robotics and Navigation for Orthopaedic Market, by End User |

|

8.2.9. North America Surgical Robotics and Navigation for Orthopaedic Market, by Application |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Surgical Robotics and Navigation for Orthopaedic Market, by Product Type |

|

8.2.10.1.2. US Surgical Robotics and Navigation for Orthopaedic Market, by Technology |

|

8.2.10.1.3. US Surgical Robotics and Navigation for Orthopaedic Market, by End User |

|

8.2.10.1.4. US Surgical Robotics and Navigation for Orthopaedic Market, by Application |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Intuitive Surgical |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Stryker Corporation |

|

10.3. Zimmer Biomet |

|

10.4. Medtronic PLC |

|

10.5. Johnson & Johnson (DePuy Synthes) |

|

10.6. Smith & Nephew |

|

10.7. Mazor Robotics (acquired by Medtronic) |

|

10.8. Corindus Vascular Robotics |

|

10.9. Think Surgical |

|

10.10. Blue Belt Technologies (acquired by Smith & Nephew) |

|

10.11. KUKA Robotics |

|

10.12. TransEnterix |

|

10.13. Robotic Surgery Technologies, Inc. |

|

10.14. OrthAlign, Inc. |

|

10.15. DJO Global (A Zimmer Biomet Company) |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Surgical Robotics and Navigation for Orthopaedic Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Surgical Robotics and Navigation for Orthopaedic Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Surgical Robotics and Navigation for Orthopaedic Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA