As per Intent Market Research, the Supplemental Health Market was valued at USD 28.5 billion in 2024-e and will surpass USD 59.1 billion by 2030; growing at a CAGR of 11.0% during 2025 - 2030.

The supplemental health market is experiencing rapid expansion, driven by increasing consumer awareness of the importance of maintaining good health through proper nutrition. As more people seek ways to improve their well-being and prevent chronic diseases, the demand for health supplements has grown significantly. These products, which include vitamins, minerals, herbal supplements, and amino acids, are widely used to address specific health needs, enhance physical performance, and boost overall vitality. The market is also fueled by rising health consciousness, the aging population, and the growing trend of preventive healthcare.

Consumers are increasingly turning to supplements as part of their daily routines, seeking convenience and efficacy in managing health concerns such as immunity, digestion, cardiovascular health, and bone strength. The market is further boosted by innovations in product formulations, with personalized supplements gaining popularity as more people opt for customized health solutions. With the ongoing rise of e-commerce platforms and the widespread availability of these products, the supplemental health market is positioned for sustained growth across the globe.

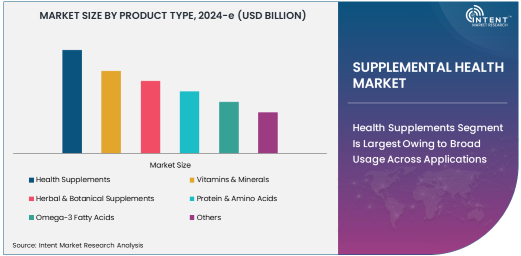

Health Supplements Segment Is Largest Owing to Broad Usage Across Applications

The health supplements segment is the largest in the supplemental health market, accounting for a significant portion of market demand. This broad category includes products designed to address general health needs, boost energy, improve immune function, and manage various chronic conditions. Health supplements have become a staple in many people's daily routines as they seek to enhance their well-being and fill nutritional gaps.

These products encompass a wide array of offerings, from multivitamins to specialized formulas targeting specific health concerns such as weight management, skin health, and digestive issues. The versatility of health supplements, their accessibility, and the growing recognition of their role in promoting a healthy lifestyle have contributed to the dominance of this segment. Additionally, the rising interest in preventative healthcare and self-care practices further supports the growth of health supplements as a key market driver.

Vitamins & Minerals Segment Is Fastest Growing Due to Rising Deficiency Awareness

The vitamins and minerals segment is the fastest growing in the supplemental health market, driven by increasing awareness of vitamin and mineral deficiencies and their impact on health. These deficiencies can lead to a range of health issues, including weakened immunity, fatigue, and poor bone health. As more consumers become aware of the need to supplement their diet with essential vitamins and minerals, the demand for these products has surged.

Vitamins such as vitamin D, B12, and vitamin C, along with minerals like calcium, magnesium, and zinc, are among the most commonly sought-after supplements. The increasing popularity of personalized nutrition, where individuals take specific vitamin and mineral supplements based on their health needs, has also accelerated the growth of this segment. As a result, the vitamins and minerals segment continues to see significant market expansion.

Immune Support Segment Is Largest Application Owing to Pandemic-Driven Demand

The immune support segment is the largest application area in the supplemental health market, largely due to heightened consumer awareness surrounding immunity, especially in the wake of the COVID-19 pandemic. The global health crisis significantly increased interest in products that promote a strong immune system, leading to a surge in demand for supplements containing vitamins C, D, and zinc, as well as herbal ingredients like echinacea and elderberry.

Immune support supplements are now a common part of many consumers' daily health regimens, driven by the desire to prevent illness and enhance the body’s natural defenses. The rise of immune-boosting supplements in response to the pandemic has created a long-lasting shift in consumer behavior, positioning immune support as a dominant application segment with continued strong demand in the post-pandemic era.

Individuals Segment Is Largest End-User Due to Growing Self-Care Trends

The individuals segment is the largest end-user group in the supplemental health market, driven by the increasing trend of self-care and personalized health management. Consumers are increasingly taking responsibility for their health, using supplements as a proactive measure to prevent illness and maintain overall wellness. This shift toward self-care is supported by growing awareness of the benefits of supplementation and a desire for more control over personal health outcomes.

Individuals are using supplements to target specific health concerns, improve energy levels, and boost performance. The convenience and ease of purchasing supplements from a variety of distribution channels, including retail stores and online platforms, have made them accessible to a wide consumer base. As personalized health becomes a priority, the individual consumer segment will continue to lead the market.

E-commerce Segment Is Fastest Growing Distribution Channel Due to Convenience and Accessibility

The e-commerce distribution channel is the fastest growing in the supplemental health market, driven by the convenience and accessibility it offers to consumers. Online shopping has become increasingly popular for purchasing health supplements due to the ability to compare products, read customer reviews, and take advantage of discounts. E-commerce platforms such as Amazon, specialized health websites, and direct-to-consumer brand websites provide a wide variety of health supplements, making it easier for consumers to access these products from the comfort of their homes.

The ability to have health supplements delivered directly to their doorsteps, along with the availability of a broad selection of products, has contributed to the rapid growth of the e-commerce channel. Moreover, the growth of mobile apps and subscription services tailored to consumers' health needs is expected to continue fueling the rise of e-commerce as the preferred distribution channel in the supplemental health market.

North America Leads the Market Due to High Health Consciousness and Market Penetration

North America is the largest region in the supplemental health market, driven by high levels of health consciousness, strong purchasing power, and advanced healthcare systems. The United States, in particular, is a dominant market for health supplements, with consumers increasingly turning to dietary supplements to address specific health concerns and enhance overall wellness. The widespread availability of supplements through retail stores, pharmacies, and e-commerce platforms has made these products easily accessible to a large population.

Moreover, the growing awareness of chronic health conditions, along with an aging population, has fueled the demand for supplements to support bone health, cardiovascular health, and immune function. North America's well-established infrastructure for health and wellness products, along with a large consumer base, ensures its continued leadership in the supplemental health market.

Competitive Landscape: Leading Companies Innovating for Market Share

The supplemental health market is highly competitive, with numerous global and regional players vying for market share. Leading companies such as Nestlé Health Science, Herbalife Nutrition, Amway, and GNC are driving innovation in product development, offering a broad range of supplements catering to various health concerns. These companies focus on enhancing the efficacy and quality of their products, developing new formulations, and expanding their product lines to cater to growing consumer demand.

In addition to traditional players, new entrants and smaller companies are also capitalizing on the demand for personalized and natural health supplements, creating niche products that cater to specific consumer needs. The competitive landscape is marked by a focus on branding, quality, and consumer trust, as companies strive to differentiate themselves in a market that is becoming increasingly consumer-driven. Ongoing research and development, partnerships with health professionals, and strategic marketing campaigns will be critical to maintaining leadership and gaining market share in this dynamic and fast-growing sector.

Recent Developments:

- In December 2024, Pfizer Inc. launched a new vitamin D supplement designed to improve bone health.

- In November 2024, Amway Corporation introduced a line of omega-3 fatty acid supplements to boost cardiovascular health.

- In October 2024, Herbalife Nutrition Ltd. expanded its weight management supplement offerings with a new plant-based product.

- In September 2024, Nestlé Health Science acquired a leading probiotics company to enhance its digestive health supplement portfolio.

- In August 2024, USANA Health Sciences partnered with fitness centers to provide customized supplement plans for members.

List of Leading Companies:

- Pfizer Inc.

- GlaxoSmithKline (GSK)

- Abbott Laboratories

- Amway Corporation

- Herbalife Nutrition Ltd.

- Nature's Bounty Co.

- Bayer AG

- USANA Health Sciences

- Nestlé Health Science

- Danone Nutricia

- DuPont de Nemours, Inc.

- Reckitt Benckiser Group

- Shaklee Corporation

- NOW Foods

- Arbonne International

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 28.5 Billion |

|

Forecasted Value (2030) |

USD 59.1 Billion |

|

CAGR (2025 – 2030) |

11.0% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Supplemental Health Market by Product Type (Health Supplements, Vitamins & Minerals, Herbal & Botanical Supplements, Protein & Amino Acids, Omega-3 Fatty Acids, Others), Application (General Health, Weight Management, Immune Support, Bone & Joint Health, Cardiovascular Health, Skin Health, Digestive Health, Others), End-User (Individuals, Healthcare Providers, Fitness Centers, Online Retailers, Pharmacies), Distribution Channel (Direct Sales, Retail Stores, E-commerce) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Pfizer Inc., GlaxoSmithKline (GSK), Abbott Laboratories, Amway Corporation, Herbalife Nutrition Ltd., Nature's Bounty Co., Bayer AG, USANA Health Sciences, Nestlé Health Science, Danone Nutricia, DuPont de Nemours, Inc., Reckitt Benckiser Group, Shaklee Corporation, NOW Foods, Arbonne International |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Supplemental Health Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Health Supplements |

|

4.2. Vitamins & Minerals |

|

4.3. Herbal & Botanical Supplements |

|

4.4. Protein & Amino Acids |

|

4.5. Omega-3 Fatty Acids |

|

4.6. Others |

|

5. Supplemental Health Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. General Health |

|

5.2. Weight Management |

|

5.3. Immune Support |

|

5.4. Bone & Joint Health |

|

5.5. Cardiovascular Health |

|

5.6. Skin Health |

|

5.7. Digestive Health |

|

5.8. Others |

|

6. Supplemental Health Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Individuals |

|

6.2. Healthcare Providers |

|

6.3. Fitness Centers |

|

6.4. Online Retailers |

|

6.5. Pharmacies |

|

7. Supplemental Health Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Direct Sales |

|

7.2. Retail Stores |

|

7.3. E-commerce |

|

7.4. Others |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Supplemental Health Market, by Product Type |

|

8.2.7. North America Supplemental Health Market, by |

|

8.2.8. By Country |

|

8.2.8.1. US |

|

8.2.8.1.1. US Supplemental Health Market, by Product Type |

|

8.2.8.1.2. US Supplemental Health Market, by |

|

8.2.8.2. Canada |

|

8.2.8.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Pfizer Inc. |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. GlaxoSmithKline (GSK) |

|

10.3. Abbott Laboratories |

|

10.4. Amway Corporation |

|

10.5. Herbalife Nutrition Ltd. |

|

10.6. Nature's Bounty Co. |

|

10.7. Bayer AG |

|

10.8. USANA Health Sciences |

|

10.9. Nestlé Health Science |

|

10.10. Danone Nutricia |

|

10.11. DuPont de Nemours, Inc. |

|

10.12. Reckitt Benckiser Group |

|

10.13. Shaklee Corporation |

|

10.14. NOW Foods |

|

10.15. Arbonne International |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Supplemental Health Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Supplemental Health Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Supplemental Health Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA