As per Intent Market Research, the Skin Grafts Market was valued at USD 1.1 billion in 2024-e and will surpass USD 2.4 billion by 2030; growing at a CAGR of 11.8% during 2025 - 2030.

The skin grafts market is experiencing significant growth, driven by the rising incidence of burn injuries, traumatic wounds, and chronic skin conditions requiring reconstructive procedures. Skin grafts, which involve the transplantation of skin to cover wounds or defects, have become a critical component of wound care and reconstructive surgeries. The increasing adoption of advanced grafting techniques and materials has further contributed to the market’s expansion, as healthcare providers seek to improve patient outcomes and reduce recovery times.

Segmentation in the market is diverse, encompassing different graft types, applications, end-users, graft thicknesses, and material types. Each segment addresses unique clinical needs, from acute care in hospitals to specialized reconstructive surgeries. The advent of synthetic and biosynthetic materials is also reshaping the landscape, offering innovative solutions to meet growing demand.

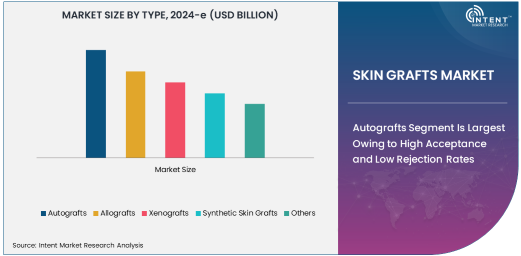

Autografts Segment Is Largest Owing to High Acceptance and Low Rejection Rates

Autografts dominate the skin grafts market, primarily due to their superior compatibility and reduced risk of rejection. Autografts involve harvesting skin from the patient’s own body, ensuring optimal integration and minimal immunological complications. This makes them a preferred choice for treating burn injuries, traumatic wounds, and chronic ulcers where long-term graft survival is critical.

The segment’s growth is further supported by advancements in harvesting techniques, such as dermatomes and skin-meshing devices, which allow for precise and efficient graft preparation. Autografts are widely used in hospitals and specialty clinics, particularly in cases where patient-specific care is paramount. With increasing investments in R&D to enhance procedural outcomes and reduce donor site morbidity, autografts are expected to maintain their dominance in the market.

Burn Injuries Segment Is Fastest Growing Due to Rising Incidence and Advanced Care Solutions

The burn injuries application segment is the fastest growing in the skin grafts market, driven by the increasing prevalence of severe burns worldwide. Burn injuries often result in extensive skin damage, requiring prompt and effective grafting to restore functionality and aesthetics. The availability of advanced grafting options, such as biosynthetic and synthetic skin grafts, has revolutionized burn care, enabling faster healing and reduced infection risks.

Government initiatives and non-governmental organization (NGO) programs to improve burn care in developing regions further fuel this segment’s growth. Specialized burn units in hospitals and advancements in graft materials, such as biosynthetic substitutes mimicking natural skin properties, contribute to better outcomes and increased adoption.

Specialty Clinics Segment Is Largest Due to Expertise in Complex Reconstructive Procedures

Specialty clinics are the largest end-user segment in the skin grafts market, reflecting their focus on providing expert care for complex cases. These clinics cater to patients requiring intricate reconstructive procedures, such as full-thickness grafts for facial burns or post-cancer surgeries. Equipped with advanced technology and staffed by specialists, these facilities deliver superior patient outcomes compared to general healthcare settings.

The growing demand for aesthetic and reconstructive surgeries, particularly in developed countries, has further bolstered the role of specialty clinics. Their ability to offer personalized care, coupled with collaborations with research institutions for clinical trials, ensures they remain at the forefront of skin graft innovations.

Split-Thickness Grafts Segment Is Fastest Growing Due to Versatility and Wound Coverage

Split-thickness grafts are the fastest-growing segment under graft thickness, attributed to their versatility and effectiveness in covering large wounds. These grafts, which consist of the epidermis and part of the dermis, are widely used in burn injuries, traumatic wounds, and chronic ulcers due to their ability to cover extensive areas with minimal donor site morbidity.

The segment’s growth is further driven by technological advancements in graft harvesting and preparation, ensuring better integration and aesthetic outcomes. Split-thickness grafts are particularly favored in emergency settings, where rapid wound coverage is essential to prevent complications like infections and fluid loss.

Biosynthetic Materials Segment Is Fastest Growing Due to Innovation and Biocompatibility

Biosynthetic materials are emerging as the fastest-growing segment in the skin grafts market, offering a blend of natural and synthetic components that enhance biocompatibility and functionality. These materials replicate the properties of natural skin, promoting faster healing and reducing the risk of infection. Their applications range from burn injuries to chronic wounds and reconstructive surgeries.

The rise in research focused on creating next-generation biosynthetic materials, such as hydrogel-based and collagen-infused grafts, is driving this segment’s rapid growth. With increasing adoption in hospitals and ambulatory surgical centers, biosynthetic materials are set to play a pivotal role in advancing skin grafting techniques.

North America Leads the Market Due to Advanced Healthcare Infrastructure and R&D Focus

North America dominates the skin grafts market, supported by its well-established healthcare infrastructure, high adoption of advanced technologies, and robust investment in research and development. The region’s growing incidence of burn injuries and skin cancer has heightened demand for grafting procedures, while its strong presence of key market players ensures continuous innovation.

The availability of specialized burn care centers and increasing public awareness about reconstructive surgery options further bolster North America’s market position. Government initiatives and funding for wound care research add to the region’s growth prospects, making it a leader in the global skin grafts market.

Competitive Landscape: Innovation and Strategic Collaborations Shape the Market

The skin grafts market is highly competitive, with key players such as Integra LifeSciences, Organogenesis, and Smith & Nephew driving innovation through extensive R&D efforts. These companies are focused on developing advanced grafting materials and techniques that enhance patient outcomes and expand their product portfolios.

Collaborations between industry players, research institutions, and healthcare providers are common, fostering innovation and improving access to cutting-edge solutions. The competitive landscape is also characterized by mergers and acquisitions, as companies strive to strengthen their market presence and capitalize on emerging opportunities. With an increasing emphasis on patient-centric care and technological advancements, the skin grafts market is poised for sustained growth and transformation.

Recent Developments:

- In November 2024, Integra LifeSciences launched a new biosynthetic graft product targeting burn injuries.

- In October 2024, Smith & Nephew expanded its product line with a split-thickness graft for chronic wounds.

- In September 2024, Avita Medical announced FDA approval for its regenerative spray-on skin solution.

- In August 2024, Mölnlycke Health Care acquired a graft technology startup to strengthen its burn care portfolio.

- In July 2024, Zimmer Biomet partnered with a biotech firm to develop advanced biosynthetic graft materials.

List of Leading Companies:

- Smith & Nephew

- Integra LifeSciences

- Mölnlycke Health Care

- Medtronic

- Organogenesis Inc.

- Zimmer Biomet

- Stryker Corporation

- MiMedx Group

- Avita Medical

- Baxter International

- Acelity L.P. Inc.

- Vericel Corporation

- Convatec Group Plc

- Allergan (AbbVie)

- Cytori Therapeutics

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.1 Billion |

|

Forecasted Value (2030) |

USD 2.4 Billion |

|

CAGR (2025 – 2030) |

11.8% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Skin Grafts Market by Type (Autografts, Allografts, Xenografts, Synthetic Skin Grafts), Application (Burn Injuries, Traumatic Wounds, Skin Cancer, Chronic Wounds), End-User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers), Graft Thickness (Split-Thickness Grafts, Full-Thickness Grafts, Composite Grafts), Material Type (Natural Materials, Synthetic Materials) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Smith & Nephew, Integra LifeSciences, Mölnlycke Health Care, Medtronic, Organogenesis Inc., Zimmer Biomet, Stryker Corporation, MiMedx Group, Avita Medical, Baxter International, Acelity L.P. Inc., Vericel Corporation, Convatec Group Plc, Allergan (AbbVie), Cytori Therapeutics |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Skin Grafts Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Autografts |

|

4.2. Allografts |

|

4.3. Xenografts |

|

4.4. Synthetic Skin Grafts |

|

4.5. Others |

|

5. Skin Grafts Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Burn Injuries |

|

5.2. Traumatic Wounds |

|

5.3. Skin Cancer |

|

5.4. Chronic Wounds |

|

5.5. Others |

|

6. Skin Grafts Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals |

|

6.2. Specialty Clinics |

|

6.3. Ambulatory Surgical Centers |

|

6.4. Others |

|

7. Skin Grafts Market, by Graft Thickness (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Split-Thickness Grafts |

|

7.2. Full-Thickness Grafts |

|

7.3. Composite Grafts |

|

8. Skin Grafts Market, by Material Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Natural Materials |

|

8.2. Synthetic Materials |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Skin Grafts Market, by Type |

|

9.2.7. North America Skin Grafts Market, by Application |

|

9.2.8. North America Skin Grafts Market, by End-User |

|

9.2.9. North America Skin Grafts Market, by Graft Thickness |

|

9.2.10. North America Skin Grafts Market, by Material Type |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Skin Grafts Market, by Type |

|

9.2.11.1.2. US Skin Grafts Market, by Application |

|

9.2.11.1.3. US Skin Grafts Market, by End-User |

|

9.2.11.1.4. US Skin Grafts Market, by Graft Thickness |

|

9.2.11.1.5. US Skin Grafts Market, by Material Type |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. Smith & Nephew |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Integra LifeSciences |

|

11.3. Mölnlycke Health Care |

|

11.4. Medtronic |

|

11.5. Organogenesis Inc. |

|

11.6. Zimmer Biomet |

|

11.7. Stryker Corporation |

|

11.8. MiMedx Group |

|

11.9. Avita Medical |

|

11.10. Baxter International |

|

11.11. Acelity L.P. Inc. |

|

11.12. Vericel Corporation |

|

11.13. Convatec Group Plc |

|

11.14. Allergan (AbbVie) |

|

11.15. Cytori Therapeutics |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Skin Grafts Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Skin Grafts Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Skin Grafts Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA