As per Intent Market Research, the Post Surgical Scar Treatment Market was valued at USD 5.1 billion in 2024-e and will surpass USD 7.8 billion by 2030; growing at a CAGR of 7.5% during 2025 - 2030.

The global post-surgical scar treatment market is experiencing significant growth due to increasing surgical procedures, rising awareness about scar management, and advancements in treatment technologies. Post-surgical scar treatments are essential for improving the aesthetic outcomes of patients, particularly following invasive surgeries. These treatments include a variety of options such as creams, gels, silicone sheets, laser devices, and more, each targeting different types of scars, ranging from keloids to acne scars. The market is driven by the rising number of cosmetic surgeries, growing focus on dermatological care, and an expanding range of effective scar treatment solutions.

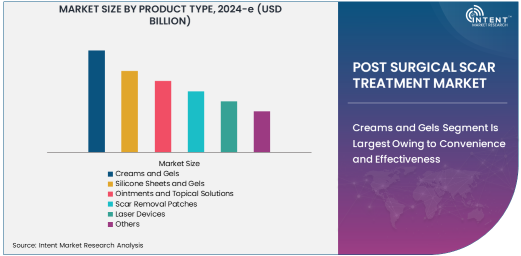

Creams and Gels Segment Is Largest Owing to Convenience and Effectiveness

The creams and gels segment holds the largest share in the post-surgical scar treatment market, primarily due to their ease of use and effectiveness in reducing scar visibility. These topical treatments are widely used by patients post-surgery, as they offer a non-invasive and convenient solution for scar management. Creams and gels typically contain active ingredients like silicone, vitamins, and antioxidants that help in the healing process, improving the skin's appearance and promoting tissue regeneration. The availability of over-the-counter products further enhances their market penetration, making them accessible to a broader consumer base.

Moreover, the cream and gel segment benefits from continuous product innovations and the development of advanced formulations that improve the efficacy of scar healing. These products are often recommended by dermatologists for at-home use, driving their widespread adoption. The low cost compared to other treatment options and the ease of application contribute to the segment's dominance in the market.

Keloid Scars Segment Is Fastest Growing Due to Growing Awareness and Advancements in Treatments

The keloid scars segment is expected to grow at the fastest rate in the global post-surgical scar treatment market. Keloid scars, which are raised, thick, and often extend beyond the original wound area, are more difficult to treat than other types of scars. As awareness about the availability of effective treatments grows, including silicone-based therapies, corticosteroid injections, and laser treatments, the demand for specialized products targeting keloids has surged. This is fueled by the increasing incidence of surgeries that result in keloid formation, particularly among individuals with a genetic predisposition to develop these scars.

Healthcare professionals are also more aware of the need for early intervention, which has led to a rise in the adoption of products that prevent keloid formation or minimize its appearance. This trend is driving the demand for keloid-specific treatments, positioning this segment as the fastest-growing in the market. Additionally, the expanding research into advanced treatments, such as laser therapies and biologic treatments, is further accelerating the market growth for keloid scar treatments.

Home Care Settings Segment Is Largest End-User Due to Growing Demand for Convenience

The home care settings segment is the largest end-user segment in the post-surgical scar treatment market, driven by the increasing preference for at-home care solutions. Many patients prefer using scar treatment products in the comfort of their own homes, especially for cosmetic or minor surgeries that do not require professional supervision. Home care treatments such as creams, gels, and silicone sheets provide an affordable and convenient method for patients to manage their scars post-surgery. This segment's growth is further supported by the rise of online retail platforms, which allow consumers to easily access these products.

In addition, the growing trend of self-care and at-home beauty treatments contributes to the popularity of home-based scar management solutions. With a wide range of products available over-the-counter and through e-commerce platforms, patients can choose the treatments that best suit their needs, fostering the continued expansion of this segment in the market.

Online Retail Segment Is Fastest Growing Distribution Channel Due to E-Commerce Boom

The online retail segment is the fastest-growing distribution channel in the post-surgical scar treatment market. With the rise of e-commerce and digital platforms, more consumers are opting to purchase scar treatment products online due to the convenience of doorstep delivery and the availability of a wide variety of options. E-commerce platforms provide customers with easy access to both well-known and niche brands, allowing for price comparisons and product reviews that help in making informed purchasing decisions.

Furthermore, online platforms often provide exclusive deals and discounts, which attract more customers, especially in markets where traditional retail infrastructure may be underdeveloped. The ongoing shift towards online shopping, particularly in regions like North America and Asia Pacific, is driving the rapid growth of this segment.

Asia Pacific Region Is Fastest Growing Due to Increasing Surgical Procedures and Awareness

The Asia Pacific region is the fastest-growing market for post-surgical scar treatments, driven by the increasing number of cosmetic and reconstructive surgeries, as well as rising awareness of scar management. Countries like China, India, and Japan are witnessing a surge in both medical and aesthetic procedures, leading to a higher incidence of post-surgical scars. Moreover, the increasing focus on personal aesthetics and the growing healthcare infrastructure in these regions are accelerating demand for scar treatment products.

The growing middle class and the rising disposable income in countries like India and China are also contributing to the market's expansion. As consumers in these regions are becoming more aware of the availability and effectiveness of scar treatment solutions, the demand for both over-the-counter and prescription scar management products is increasing rapidly.

Competitive Landscape: Leading Companies and Strategic Developments

The global post-surgical scar treatment market is competitive, with several key players dominating the landscape. Companies such as Mederma, Kelo-cote, and Smith & Nephew are leading the market, offering a range of advanced and effective scar treatment solutions. These companies are focused on product innovation, expanding their distribution networks, and enhancing their online retail presence to capture a larger share of the market.

Strategic partnerships, acquisitions, and technological advancements are key strategies employed by these companies to strengthen their market positions. For instance, companies like Stratpharma and NewGel+ have introduced innovative silicone-based treatments, which are gaining popularity due to their effectiveness in preventing and treating scars. The competitive landscape is also evolving with the entry of new players offering cutting-edge treatments such as laser devices and biologic therapies, further intensifying the competition in the market.

Recent Developments:

- Mederma launched a new silicone-based scar treatment gel, offering improved formulation for faster healing and better scar reduction.

- Smith & Nephew announced an acquisition of a leading scar treatment company to expand its dermatology portfolio and enhance product offerings for scar management.

- Hollister Incorporated received FDA approval for a new silicone gel sheet designed for both hypertrophic and keloid scars.

- Stratpharma entered a strategic partnership with a major pharmaceutical company to distribute their innovative scar treatment solutions globally.

- Avita Medical has expanded its product portfolio by introducing a new treatment focused on scar healing and skin regeneration, targeting surgical scars in the post-surgical care market.

List of Leading Companies:

- Mederma

- ScarAway

- Kelo-cote

- Smith & Nephew

- Hollister Incorporated

- Stratpharma

- Biodermis

- NewGel+

- Dermatix

- Avita Medical

- Hada Labo

- Revitol

- Emo Oil

- TCL

- TetraRx

- Keyword

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 5.1 Billion |

|

Forecasted Value (2030) |

USD 7.8 Billion |

|

CAGR (2025 – 2030) |

7.5% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Post-Surgical Scar Treatment Market By Product Type (Creams and Gels, Silicone Sheets and Gels, Ointments and Topical Solutions, Scar Removal Patches, Laser Devices), By Scar Type (Keloid Scars, Hypertrophic Scars, Atrophic Scars, Contracture Scars, Acne Scars, Stretch Marks), By End-User (Hospitals, Clinics, Home Care Settings, Dermatology Centers), By Distribution Channel (Online Retail, Offline Retail, Drug Stores/Pharmacies, Supermarkets/Hypermarkets, Direct Sales) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Mederma, ScarAway, Kelo-cote, Smith & Nephew, Hollister Incorporated, Stratpharma, Biodermis, NewGel+, Dermatix, Avita Medical, Hada Labo, Revitol, Emo Oil, TCL, TetraRx |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Post Surgical Scar Treatment Market, by Product Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Creams and Gels |

|

4.2. Silicone Sheets and Gels |

|

4.3. Ointments and Topical Solutions |

|

4.4. Scar Removal Patches |

|

4.5. Laser Devices |

|

4.6. Others |

|

5. Post Surgical Scar Treatment Market, by Scar Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Keloid Scars |

|

5.2. Hypertrophic Scars |

|

5.3. Atrophic Scars |

|

5.4. Contracture Scars |

|

5.5. Acne Scars |

|

5.6. Stretch Marks |

|

6. Post Surgical Scar Treatment Market, by End-User (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Hospitals |

|

6.2. Clinics |

|

6.3. Home Care Settings |

|

6.4. Dermatology Centers |

|

6.5. Others |

|

7. Post Surgical Scar Treatment Market, by Distribution Channel (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Online Retail |

|

7.2. Offline Retail |

|

7.3. Drug Stores/Pharmacies |

|

7.4. Supermarkets/Hypermarkets |

|

7.5. Direct Sales |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Post Surgical Scar Treatment Market, by Product Type |

|

8.2.7. North America Post Surgical Scar Treatment Market, by Scar Type |

|

8.2.8. North America Post Surgical Scar Treatment Market, by End-User |

|

8.2.9. North America Post Surgical Scar Treatment Market, by |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Post Surgical Scar Treatment Market, by Product Type |

|

8.2.10.1.2. US Post Surgical Scar Treatment Market, by Scar Type |

|

8.2.10.1.3. US Post Surgical Scar Treatment Market, by End-User |

|

8.2.10.1.4. US Post Surgical Scar Treatment Market, by |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Mederma |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. ScarAway |

|

10.3. Kelo-cote |

|

10.4. Smith & Nephew |

|

10.5. Hollister Incorporated |

|

10.6. Stratpharma |

|

10.7. Biodermis |

|

10.8. NewGel+ |

|

10.9. Dermatix |

|

10.10. Avita Medical |

|

10.11. Hada Labo |

|

10.12. Revitol |

|

10.13. Emo Oil |

|

10.14. TCL |

|

10.15. TetraRx |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Post-Surgical Scar Treatment Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Post-Surgical Scar Treatment Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Post-Surgical Scar Treatment Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA