As per Intent Market Research, the Photodiode Sensors Market was valued at USD 1.0 Billion in 2024-e and will surpass USD 1.8 Billion by 2030; growing at a CAGR of 10.2% during 2025-2030.

The photodiode sensors market is experiencing robust growth, driven by their widespread adoption across diverse applications including consumer electronics, automotive, healthcare, and industrial automation. Photodiode sensors offer high-speed response, precision, and reliability in detecting light, making them indispensable in various technological advancements. With the rising demand for compact, efficient, and cost-effective sensors, innovations in photodiode technology are rapidly shaping the market landscape. The integration of photodiodes in emerging applications such as autonomous vehicles, medical imaging, and telecommunications further underscores their expanding significance.

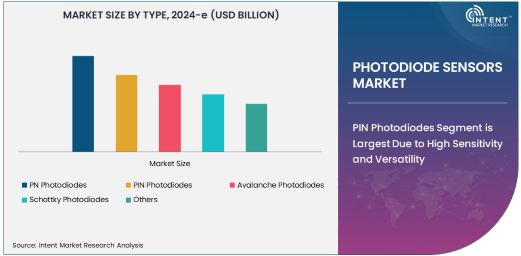

The market is segmented by type, material, and application, each playing a critical role in determining the suitability and performance of photodiode sensors for specific use cases. Among these, PIN photodiodes stand out for their versatility, while silicon remains the most commonly used material due to its cost-effectiveness and efficiency. Telecommunications and automotive sectors are witnessing rapid adoption of photodiodes, bolstering overall market growth.

PIN Photodiodes Segment is Largest Due to High Sensitivity and Versatility

The PIN photodiodes segment dominates the photodiode sensors market, owing to their high sensitivity and fast response times. These photodiodes are widely used in applications requiring precise light detection and high-speed data transmission, such as fiber-optic communication, industrial automation, and healthcare diagnostics. Their ability to operate efficiently in low-light conditions and high-frequency applications makes them highly versatile across multiple industries.

PIN photodiodes' simple design and compatibility with a range of materials, including silicon and InGaAs, further enhance their popularity. As demand for high-performance photodetectors increases, especially in telecommunications and industrial sectors, the PIN photodiodes segment is expected to maintain its leadership position.

Indium Gallium Arsenide (InGaAs) Material Segment is Fastest Growing Due to Superior Performance

Indium Gallium Arsenide (InGaAs) is the fastest-growing material segment in the photodiode sensors market. InGaAs photodiodes are known for their exceptional performance in detecting near-infrared light, making them ideal for advanced applications such as optical spectroscopy, laser range-finding, and night vision systems. Their high quantum efficiency and low noise levels enable superior performance in critical industries like aerospace & defense and healthcare.

The rising demand for high-precision sensors in emerging technologies, including LiDAR systems for autonomous vehicles and high-speed data communication, is driving the adoption of InGaAs photodiodes. While they are costlier than silicon photodiodes, their unmatched efficiency and expanding use cases justify their rapid growth trajectory.

Automotive Application Segment is Fastest Growing Due to ADAS Integration

The automotive segment is the fastest-growing application area for photodiode sensors, primarily driven by the increasing integration of Advanced Driver Assistance Systems (ADAS). Photodiodes are critical in ADAS technologies, enabling features such as automatic braking, collision avoidance, and adaptive cruise control. Additionally, their use in LiDAR systems for autonomous driving and optical sensors for vehicle monitoring is further accelerating their adoption.

With the global push towards vehicle electrification and smart transportation systems, the demand for photodiode sensors in the automotive sector is set to surge. The need for highly sensitive and durable sensors that can operate efficiently in dynamic environments positions photodiodes as essential components in the future of automotive innovation.

Telecommunications Segment is Largest Due to Data Transmission Demands

The telecommunications segment holds the largest share in the photodiode sensors market, driven by the ever-increasing demand for high-speed data transmission and optical communication. Photodiodes play a crucial role in converting optical signals into electrical signals in fiber-optic networks, enabling faster and more reliable communication. With the proliferation of 5G networks, cloud computing, and IoT, the need for advanced photodiodes capable of handling high bandwidth and low latency is growing exponentially.

The transition from traditional copper-based networks to fiber-optic infrastructure further boosts the demand for photodiode sensors. As the telecommunications industry continues to expand globally, the reliance on photodiodes for seamless connectivity is expected to sustain their dominance in this sector.

North America is Largest Market Owing to Technological Advancements

North America leads the photodiode sensors market, attributed to its robust technological infrastructure and high adoption of advanced technologies across industries. The region's strong presence in sectors like telecommunications, aerospace & defense, and healthcare drives the demand for high-performance photodiodes. The United States, in particular, is a hub for innovation, with significant investments in research and development for optical communication, autonomous vehicles, and medical imaging technologies.

Additionally, the growing implementation of 5G networks and the presence of leading market players further enhance North America's position as the largest market. As industries in the region continue to prioritize efficiency and innovation, the demand for photodiode sensors is expected to remain strong.

Competitive Landscape: Leading Companies and Market Dynamics

The photodiode sensors market is highly competitive, with key players such as Hamamatsu Photonics, OSI Optoelectronics, ON Semiconductor, and Excelitas Technologies driving innovation through extensive research and development. These companies are focusing on developing next-generation photodiodes with improved sensitivity, faster response times, and broader spectral ranges to meet the evolving demands of various industries.

Collaborations with end-use industries, particularly in telecommunications and automotive, are shaping the competitive landscape. Additionally, the growing focus on miniaturization and energy efficiency in sensor technologies is encouraging market players to invest in advanced materials and designs, further intensifying competition in this dynamic market.

Recent Developments:

- Hamamatsu Photonics K.K. developed a new high-speed photodiode for LiDAR applications.

- First Sensor AG expanded its production capacity to meet growing demand for automotive photodiodes.

- Vishay Intertechnology, Inc. launched a new range of silicon PIN photodiodes for optical communication systems.

- Excelitas Technologies Corp. introduced a compact photodiode sensor for industrial automation.

- ON Semiconductor Corporation announced a collaboration to create advanced photodiode sensors for healthcare devices.

List of Leading Companies:

- Hamamatsu Photonics K.K.

- OSI Optoelectronics

- First Sensor AG

- Excelitas Technologies Corp.

- Vishay Intertechnology, Inc.

- ON Semiconductor Corporation

- Broadcom Inc.

- Everlight Electronics Co., Ltd.

- Rohm Semiconductor

- Honeywell International Inc.

- Kyosemi Corporation

- Toshiba Corporation

- TT Electronics Plc

- Luna Innovations Incorporated

- Advanced Photonix, Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.0 Billion |

|

Forecasted Value (2030) |

USD 1.8 Billion |

|

CAGR (2025 – 2030) |

10.2% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Photodiode Sensors Market By Type (PN Photodiodes, PIN Photodiodes, Avalanche Photodiodes, Schottky Photodiodes), By Material (Silicon, Germanium, Indium Gallium Arsenide (InGaAs)), By Application (Consumer Electronics, Automotive, Healthcare, Industrial Automation, Aerospace & Defense, Telecommunications) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Hamamatsu Photonics K.K., OSI Optoelectronics, First Sensor AG, Excelitas Technologies Corp., Vishay Intertechnology, Inc., ON Semiconductor Corporation, Broadcom Inc., Everlight Electronics Co., Ltd., Rohm Semiconductor, Honeywell International Inc., Kyosemi Corporation, Toshiba Corporation, TT Electronics Plc, Luna Innovations Incorporated, Advanced Photonix, Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Photodiode Sensors Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. PN Photodiodes |

|

4.2. PIN Photodiodes |

|

4.3. Avalanche Photodiodes |

|

4.4. Schottky Photodiodes |

|

4.5. Others |

|

5. Photodiode Sensors Market, by Material (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Silicon |

|

5.2. Germanium |

|

5.3. Indium Gallium Arsenide (InGaAs) |

|

5.4. Others |

|

6. Photodiode Sensors Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Consumer Electronics |

|

6.2. Automotive |

|

6.3. Healthcare |

|

6.4. Industrial Automation |

|

6.5. Aerospace & Defense |

|

6.6. Telecommunications |

|

6.7. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Photodiode Sensors Market, by Type |

|

7.2.7. North America Photodiode Sensors Market, by Material |

|

7.2.8. North America Photodiode Sensors Market, by Application |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Photodiode Sensors Market, by Type |

|

7.2.9.1.2. US Photodiode Sensors Market, by Material |

|

7.2.9.1.3. US Photodiode Sensors Market, by Application |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Hamamatsu Photonics K.K. |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. OSI Optoelectronics |

|

9.3. First Sensor AG |

|

9.4. Excelitas Technologies Corp. |

|

9.5. Vishay Intertechnology, Inc. |

|

9.6. ON Semiconductor Corporation |

|

9.7. Broadcom Inc. |

|

9.8. Everlight Electronics Co., Ltd. |

|

9.9. Rohm Semiconductor |

|

9.10. Honeywell International Inc. |

|

9.11. Kyosemi Corporation |

|

9.12. Toshiba Corporation |

|

9.13. TT Electronics Plc |

|

9.14. Luna Innovations Incorporated |

|

9.15. Advanced Photonix, Inc. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Photodiode Sensors Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Photodiode Sensors Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Photodiode Sensors Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA