As per Intent Market Research, the Phenoxy Resins Market was valued at USD 944.4 Million in 2024-e and will surpass USD 2077.8 Million by 2030; growing at a CAGR of 14.0% during 2025-2030.

The phenoxy resins market is witnessing steady growth driven by the increasing demand for high-performance materials that offer exceptional chemical resistance, flexibility, and durability. These resins, known for their versatility, are utilized across a wide array of industries, including automotive, coatings, adhesives, and electronics. With a broad range of applications, phenoxy resins are highly valued for their ability to withstand harsh environments and improve the overall functionality of products. The market is further fueled by innovations in resin formulations and the expanding need for advanced materials in various industrial applications.

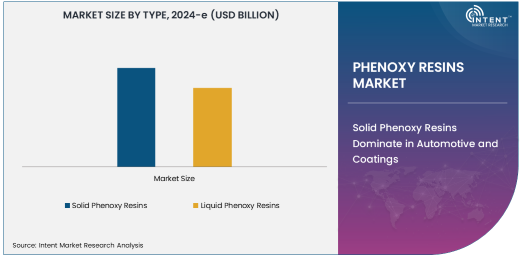

Among the types of phenoxy resins, solid and liquid variants dominate the market, each offering distinct benefits depending on the application. Solid phenoxy resins are favored in industries that require strong adhesion and excellent impact resistance, such as automotive coatings and adhesives. On the other hand, liquid phenoxy resins are preferred for their ease of handling and suitability in applications requiring higher flexibility. As industries continue to focus on improving product performance and reducing material costs, the demand for phenoxy resins is expected to grow in tandem, particularly in high-performance sectors.

Solid Phenoxy Resins Dominate in Automotive and Coatings

Solid phenoxy resins are the largest subsegment within the phenoxy resins market, driven primarily by their use in automotive and coatings applications. These resins offer superior chemical resistance, high-temperature stability, and excellent adhesion properties, making them ideal for automotive coatings and adhesives. In the automotive sector, solid phenoxy resins are used to enhance the durability and aesthetic appeal of vehicle exteriors and interiors. The demand for automotive coatings that can withstand environmental stressors like UV radiation, humidity, and temperature variations further boosts the growth of solid phenoxy resins in this sector.

Additionally, in the coatings industry, solid phenoxy resins are extensively used in high-performance industrial coatings due to their ability to provide a smooth, resistant finish. These coatings are ideal for metal substrates, offering protection against corrosion and wear. As automotive and industrial coatings continue to evolve with an emphasis on durability and long-lasting performance, the preference for solid phenoxy resins is expected to remain strong. With an increasing focus on high-quality finishes and environmentally resilient materials, the automotive and coatings sectors will continue to be the driving force behind the demand for solid phenoxy resins.

Liquid Phenoxy Resins Fuel Growth in Adhesives and Electronics

Liquid phenoxy resins are the fastest-growing subsegment in the phenoxy resins market, particularly in the adhesives and electronics industries. These resins are known for their flexibility, ease of processing, and ability to provide strong bonding solutions for various substrates. In adhesives, liquid phenoxy resins are used for their excellent adhesion to metals, plastics, and composites, making them a preferred choice in applications such as automotive assembly, construction, and packaging. The increasing demand for high-performance adhesives that offer strong bonds under extreme conditions continues to propel the growth of liquid phenoxy resins.

In the electronics sector, liquid phenoxy resins are used in the manufacture of electrical components, such as connectors, switches, and circuit boards, where their electrical insulating properties are crucial. The rise of the consumer electronics industry and the need for efficient, durable, and heat-resistant materials in devices such as smartphones, computers, and home appliances have significantly contributed to the market expansion of liquid phenoxy resins. As the demand for miniaturized, high-performance electronic devices continues to rise, the use of liquid phenoxy resins in electronics and adhesives will likely increase, making it the fastest-growing subsegment in the phenoxy resins market.

Asia-Pacific Region Drives Phenoxy Resins Market Growth

The Asia-Pacific region is expected to be the largest and fastest-growing market for phenoxy resins. The region's rapid industrialization, coupled with increasing demand for automotive, electronics, and coatings products, makes it a key growth area for phenoxy resins. Countries like China, India, and Japan are witnessing significant demand from the automotive and electronics industries, where phenoxy resins are used extensively to meet the growing need for durable, high-performance materials.

Asia-Pacific’s automotive industry, in particular, is expanding rapidly, with increasing production and consumption of vehicles, leading to a surge in demand for high-quality automotive coatings and adhesives. Similarly, the electronics sector in the region is booming, driven by consumer electronics and the growing need for sophisticated electronic components. As a result, the Asia-Pacific region is expected to dominate the global phenoxy resins market in terms of both market size and growth rate over the forecast period.

Competitive Landscape: Key Players and Strategic Developments

The phenoxy resins market is competitive, with several global and regional players contributing to its growth. Leading companies in the market include Hexion Inc., Kaneka Corporation, Mitsubishi Chemical Corporation, and Sumitomo Bakelite Co., Ltd. These companies are focusing on product innovation, expanding their production capacities, and strengthening their supply chains to meet the growing demand for high-performance resins. Strategic partnerships, mergers and acquisitions, and investments in research and development are common approaches to enhance product offerings and market reach.

To stay ahead of market trends, companies are also focusing on sustainability and eco-friendly product development, offering resins that meet environmental regulations while maintaining high performance. Additionally, the development of advanced resin formulations that cater to specific industry needs, such as automotive lightweighting and electronics miniaturization, is helping companies differentiate their products in the competitive landscape.

Recent Developments:

- DIC Corporation launched a new range of Phenoxy resins designed for automotive coatings, enhancing durability and chemical resistance.

- Huntsman Corporation expanded its Phenoxy resin production capacity to meet the increasing demand from the coatings industry.

- Momentive Performance Materials introduced a new Phenoxy resin formulation offering better adhesion for industrial applications.

- Eastman Chemical Company announced a partnership with a leading automotive brand to supply high-performance Phenoxy resins for vehicle coatings.

- BASF SE introduced a Phenoxy resin-based product line focused on enhancing electrical insulation for electronics applications.

List of Leading Companies:

- DIC Corporation

- Huntsman Corporation

- Aditya Birla Chemicals

- Mitsubishi Chemical Corporation

- BASF SE

- Dow Chemical Company

- Hexion Inc.

- Momentive Performance Materials

- Olin Corporation

- Asahi Kasei Corporation

- Kaneka Corporation

- Eastman Chemical Company

- TCI America

- Solvay SA

- Arkema Group

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 944.4 Million |

|

Forecasted Value (2030) |

USD 2,077.8 Million |

|

CAGR (2025 – 2030) |

14.0% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Phenoxy Resins Market By Type (Solid Phenoxy Resins, Liquid Phenoxy Resins), By End-Use Application (Automotive, Coatings and Paints, Adhesives and Sealants, Electrical and Electronics, Industrial Applications) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

DIC Corporation, Huntsman Corporation, Aditya Birla Chemicals, Mitsubishi Chemical Corporation, BASF SE, Dow Chemical Company, Hexion Inc., Momentive Performance Materials, Olin Corporation, Asahi Kasei Corporation, Kaneka Corporation, Eastman Chemical Company, TCI America, Solvay SA, Arkema Group |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Phenoxy Resins Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Solid Phenoxy Resins |

|

4.2. Liquid Phenoxy Resins |

|

5. Phenoxy Resins Market, by End-Use Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Automotive |

|

5.2. Coatings and Paints |

|

5.3. Adhesives and Sealants |

|

5.4. Electrical and Electronics |

|

5.5. Industrial Applications |

|

6. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Regional Overview |

|

6.2. North America |

|

6.2.1. Regional Trends & Growth Drivers |

|

6.2.2. Barriers & Challenges |

|

6.2.3. Opportunities |

|

6.2.4. Factor Impact Analysis |

|

6.2.5. Technology Trends |

|

6.2.6. North America Phenoxy Resins Market, by Type |

|

6.2.7. North America Phenoxy Resins Market, by End-Use Application |

|

6.2.8. By Country |

|

6.2.8.1. US |

|

6.2.8.1.1. US Phenoxy Resins Market, by Type |

|

6.2.8.1.2. US Phenoxy Resins Market, by End-Use Application |

|

6.2.8.2. Canada |

|

6.2.8.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

6.3. Europe |

|

6.4. Asia-Pacific |

|

6.5. Latin America |

|

6.6. Middle East & Africa |

|

7. Competitive Landscape |

|

7.1. Overview of the Key Players |

|

7.2. Competitive Ecosystem |

|

7.2.1. Level of Fragmentation |

|

7.2.2. Market Consolidation |

|

7.2.3. Product Innovation |

|

7.3. Company Share Analysis |

|

7.4. Company Benchmarking Matrix |

|

7.4.1. Strategic Overview |

|

7.4.2. Product Innovations |

|

7.5. Start-up Ecosystem |

|

7.6. Strategic Competitive Insights/ Customer Imperatives |

|

7.7. ESG Matrix/ Sustainability Matrix |

|

7.8. Manufacturing Network |

|

7.8.1. Locations |

|

7.8.2. Supply Chain and Logistics |

|

7.8.3. Product Flexibility/Customization |

|

7.8.4. Digital Transformation and Connectivity |

|

7.8.5. Environmental and Regulatory Compliance |

|

7.9. Technology Readiness Level Matrix |

|

7.10. Technology Maturity Curve |

|

7.11. Buying Criteria |

|

8. Company Profiles |

|

8.1. DIC Corporation |

|

8.1.1. Company Overview |

|

8.1.2. Company Financials |

|

8.1.3. Product/Service Portfolio |

|

8.1.4. Recent Developments |

|

8.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

8.2. Huntsman Corporation |

|

8.3. Aditya Birla Chemicals |

|

8.4. Mitsubishi Chemical Corporation |

|

8.5. BASF SE |

|

8.6. Dow Chemical Company |

|

8.7. Hexion Inc. |

|

8.8. Momentive Performance Materials |

|

8.9. Olin Corporation |

|

8.10. Asahi Kasei Corporation |

|

8.11. Kaneka Corporation |

|

8.12. Eastman Chemical Company |

|

8.13. TCI America |

|

8.14. Solvay SA |

|

8.15. Arkema Group |

|

9. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Phenoxy Resins Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Phenoxy Resins Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Phenoxy Resins Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA