As per Intent Market Research, the Pharmaceutical Waste Management Market was valued at USD 8.6 Billion in 2024-e and will surpass USD 14.1 Billion by 2030; growing at a CAGR of 8.5% during 2025 - 2030.

The pharmaceutical waste management market is an essential component of the healthcare and pharmaceutical industries, focused on the proper disposal, recycling, and treatment of pharmaceutical waste. As the production and consumption of pharmaceuticals increase globally, the need for effective waste management solutions becomes even more critical. Improper disposal of pharmaceutical products, including expired drugs, chemicals, and other related waste, can pose environmental and public health risks. Hence, specialized waste management services are necessary to ensure safe and sustainable handling of pharmaceutical, cytotoxic, and hazardous wastes. This market is growing due to increasing regulatory requirements, environmental concerns, and the need to reduce contamination risks in healthcare settings and pharmaceutical manufacturing.

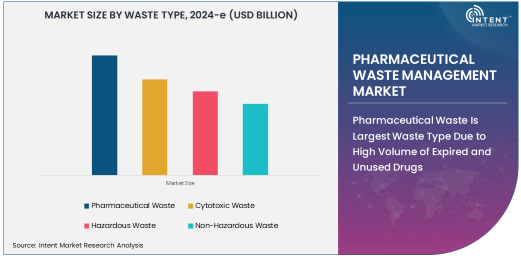

Pharmaceutical Waste Is Largest Waste Type Due to High Volume of Expired and Unused Drugs

Pharmaceutical waste is the largest waste type in the pharmaceutical waste management market, primarily driven by the high volume of expired or unused drugs generated by hospitals, pharmacies, and healthcare providers. These drugs, often classified as expired or returned, need to be disposed of properly to prevent harm to the environment or accidental ingestion. The significant volume of pharmaceutical waste is generated daily, especially in healthcare settings where medications are prescribed in large quantities for various treatments.

Additionally, the rising awareness regarding the environmental impact of improperly disposed pharmaceuticals further drives the demand for specialized pharmaceutical waste management services. Strict regulations governing the disposal of pharmaceutical waste, such as the Environmental Protection Agency (EPA) standards, ensure that waste is disposed of in a manner that mitigates any potential negative impact on the environment. As the global healthcare industry expands, the need for efficient and safe pharmaceutical waste management solutions will continue to grow.

Waste Disposal Is Largest Service Type Due to Regulatory Compliance and Environmental Safety

Waste disposal is the largest service type in the pharmaceutical waste management market, primarily due to the stringent regulatory requirements surrounding pharmaceutical waste. Regulatory bodies, such as the FDA and EPA, enforce specific guidelines for the disposal of pharmaceutical waste to prevent environmental contamination and ensure public safety. Pharmaceutical waste, especially when it includes hazardous or cytotoxic substances, must be handled with care to avoid leakage, exposure, or improper incineration.

Waste disposal services provide comprehensive solutions, including collection, transportation, and safe disposal of pharmaceutical products that can no longer be used or are expired. Hospitals, healthcare providers, and pharmaceutical manufacturers often rely on third-party service providers to manage their pharmaceutical waste disposal needs. This growing need for compliance with environmental standards and the safe disposal of pharmaceutical waste will continue to drive the demand for waste disposal services in the pharmaceutical waste management market.

Healthcare Providers Are Largest End-Use Industry Due to High Waste Generation from Medical Practices

Healthcare providers represent the largest end-use industry in the pharmaceutical waste management market, as hospitals, clinics, and pharmacies generate significant volumes of pharmaceutical waste. Healthcare providers are responsible for the disposal of not only unused or expired drugs but also biologics, vaccines, and other pharmaceutical products that cannot be used due to contamination or patient non-compliance. The healthcare industry’s need for specialized pharmaceutical waste management services is critical in maintaining safety standards and protecting both the environment and public health.

Healthcare providers, including hospitals and clinics, must adhere to strict guidelines and protocols to ensure pharmaceutical waste is handled, stored, and disposed of in accordance with regulatory requirements. The growing volume of pharmaceutical waste generated by healthcare providers, along with increasing regulatory scrutiny, contributes to the high demand for pharmaceutical waste management services within this sector.

North America Is Largest Region Due to Stringent Regulations and Growing Healthcare Infrastructure

North America is the largest region in the pharmaceutical waste management market, driven by the robust healthcare infrastructure and strict regulatory standards in the region. The United States, in particular, plays a significant role in driving the demand for pharmaceutical waste management services, with stringent regulations set by the EPA and other environmental bodies. These regulations ensure that pharmaceutical waste is disposed of safely and without risk to the environment.

The increasing awareness about the environmental impact of pharmaceutical waste, along with the rising number of healthcare facilities and pharmaceutical manufacturing units in North America, further supports the growth of the market. The region also has a high concentration of pharmaceutical manufacturers, research laboratories, and hospitals, all of which require effective waste management solutions. As North American regulatory frameworks become even more stringent, the demand for pharmaceutical waste management services will continue to expand.

Competitive Landscape and Key Players

The pharmaceutical waste management market is highly competitive, with leading players such as Stericycle, Clean Harbors, and Veolia North America at the forefront. These companies offer comprehensive waste management services, including waste disposal, collection, treatment, and recycling, to pharmaceutical manufacturers, healthcare providers, and research institutions.

To maintain a competitive edge, companies focus on expanding their service portfolios, improving waste management technologies, and ensuring compliance with ever-evolving regulations. Sustainability is also becoming a key driver in the market, with many companies looking to introduce eco-friendly waste disposal and recycling options. Partnerships with healthcare organizations and pharmaceutical manufacturers are common, as companies seek to expand their market reach and service offerings. With ongoing regulatory changes and increasing environmental concerns, the market is expected to remain dynamic and competitive in the coming years.

Recent Developments:

- Stericycle, Inc. expanded its pharmaceutical waste management services by launching a new compliance-focused program for healthcare facilities to ensure proper disposal of hazardous drugs.

- Veolia North America announced an investment in advanced pharmaceutical waste treatment technologies, aiming to enhance safety and environmental compliance in waste disposal.

- Clean Harbors, Inc. entered a partnership with Thermo Fisher Scientific to provide comprehensive waste management solutions for pharmaceutical manufacturers, including hazardous drug disposal.

- Waste Management, Inc. introduced a new pharmaceutical waste recycling program, focusing on reducing the environmental impact of unused and expired medications.

- SUEZ Recycling & Recovery unveiled a new waste management facility designed specifically for pharmaceutical waste, ensuring safe disposal and treatment of hazardous materials.

List of Leading Companies:

- Stericycle, Inc.

- Veolia North America

- Republic Services, Inc.

- Clean Harbors, Inc.

- Waste Management, Inc.

- SUEZ Recycling & Recovery

- Thermo Fisher Scientific

- Praxair Technology, Inc.

- Covanta Holding Corporation

- Biocycle

- Medasend Biomedical

- Evergreen Waste Solutions

- Roche Recycling

- Becton, Dickinson and Company (BD)

- Alpina Global Solutions

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 8.6 Billion |

|

Forecasted Value (2030) |

USD 14.1 Billion |

|

CAGR (2025 – 2030) |

8.5% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Global Pharmaceutical Waste Management Market by Waste Type (Pharmaceutical Waste, Cytotoxic Waste, Hazardous Waste, Non-Hazardous Waste), by Service Type (Waste Disposal, Waste Collection, Waste Treatment, Waste Recycling), by End-Use Industry (Pharmaceutical Manufacturers, Healthcare Providers, Research and Development Laboratories, Hospitals and Clinics); Insights & Forecast (2024 – 2030) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Stericycle, Inc., Veolia North America, Republic Services, Inc., Clean Harbors, Inc., Waste Management, Inc., SUEZ Recycling & Recovery, Praxair Technology, Inc., Covanta Holding Corporation, Biocycle, Medasend Biomedical, Evergreen Waste Solutions, Roche Recycling, Alpina Global Solutions |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Pharmaceutical Waste Management Market, by Waste Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Pharmaceutical Waste |

|

4.2. Cytotoxic Waste |

|

4.3. Hazardous Waste |

|

4.4. Non-Hazardous Waste |

|

5. Pharmaceutical Waste Management Market, by Service Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Waste Disposal |

|

5.2. Waste Collection |

|

5.3. Waste Treatment |

|

5.4. Waste Recycling |

|

6. Pharmaceutical Waste Management Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Pharmaceutical Manufacturers |

|

6.2. Healthcare Providers |

|

6.3. Research and Development Laboratories |

|

6.4. Hospitals and Clinics |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Pharmaceutical Waste Management Market, by Waste Type |

|

7.2.7. North America Pharmaceutical Waste Management Market, by Service Type |

|

7.2.8. North America Pharmaceutical Waste Management Market, by End-Use Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Pharmaceutical Waste Management Market, by Waste Type |

|

7.2.9.1.2. US Pharmaceutical Waste Management Market, by Service Type |

|

7.2.9.1.3. US Pharmaceutical Waste Management Market, by End-Use Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Stericycle, Inc. |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Veolia North America |

|

9.3. Republic Services, Inc. |

|

9.4. Clean Harbors, Inc. |

|

9.5. Waste Management, Inc. |

|

9.6. SUEZ Recycling & Recovery |

|

9.7. Thermo Fisher Scientific |

|

9.8. Praxair Technology, Inc. |

|

9.9. Covanta Holding Corporation |

|

9.10. Biocycle |

|

9.11. Medasend Biomedical |

|

9.12. Evergreen Waste Solutions |

|

9.13. Roche Recycling |

|

9.14. Becton, Dickinson and Company (BD) |

|

9.15. Alpina Global Solutions |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Pharmaceutical Waste Management Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Pharmaceutical Waste Management Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Pharmaceutical Waste Management Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA