As per Intent Market Research, the Pharmaceutical Pouch Market was valued at USD 4.8 Billion in 2024-e and will surpass USD 8.9 Billion by 2030; growing at a CAGR of 10.8% during 2025 - 2030.

The pharmaceutical pouch market is an essential segment within the pharmaceutical packaging industry, offering flexible and lightweight packaging solutions for a variety of pharmaceutical products. Pouches are widely used due to their convenience, ease of handling, and cost-effectiveness, especially for single-use applications and small to medium-sized quantities of drugs. As the demand for pharmaceutical products continues to rise globally, the need for reliable and high-quality packaging solutions is more crucial than ever. The market is being driven by advancements in materials and manufacturing techniques that allow pharmaceutical pouches to meet the specific needs of the industry, including product safety, convenience, and tamper-evidence.

The increasing demand for over-the-counter medications, liquid formulations, and solid dosage forms packaged in pouches is contributing to the market's growth. Additionally, growing concerns about sustainability are prompting manufacturers to explore eco-friendly materials for pouch production, further boosting the market for pharmaceutical pouches. This trend is expected to drive innovation in both materials and designs, enabling the pharmaceutical pouch market to expand in line with the evolving needs of the pharmaceutical industry.

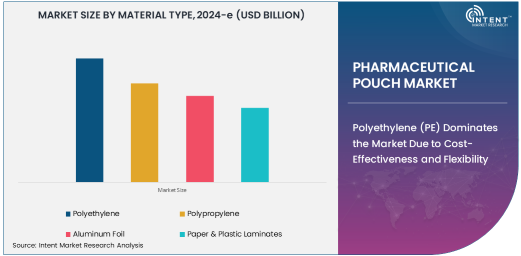

Polyethylene (PE) Dominates the Market Due to Cost-Effectiveness and Flexibility

Polyethylene (PE) is the leading material type in the pharmaceutical pouch market, owing to its cost-effectiveness, flexibility, and wide range of applications. PE pouches are widely used for the packaging of solid and liquid medications, providing an excellent balance between cost and performance. The material’s properties, such as moisture resistance, durability, and ease of sealing, make it ideal for pharmaceutical applications where product safety and convenience are key considerations.

PE-based pouches are particularly favored for their ability to be easily processed into various shapes and sizes, making them versatile for a variety of pharmaceutical products, including single-dose packaging for over-the-counter medications and small volume prescription drugs. Furthermore, polyethylene is lightweight, which helps reduce transportation costs and supports the overall sustainability efforts of the pharmaceutical industry. As a result, PE pouches are expected to maintain their dominant position in the pharmaceutical pouch market.

Single Pouch Packaging is the Largest Product Segment Due to Consumer Demand for Convenience

The single pouch packaging is the largest product segment in the pharmaceutical pouch market, driven by its convenience and widespread use in the packaging of individual doses of pharmaceutical products. Single pouches are particularly popular for the packaging of oral solid medications, such as tablets and capsules, as well as single-dose liquid medications. These pouches offer an ideal solution for products that need to be delivered in pre-measured quantities for ease of use, especially for over-the-counter medications.

The growing preference for unit-dose packaging, which enhances medication safety and compliance, is contributing to the growth of this segment. Single pouches are also highly favored in markets where convenience and portability are key, such as for travel-sized or emergency medications. As the demand for single-dose, tamper-evident, and convenient packaging solutions increases, the single pouch segment is expected to maintain its leadership in the pharmaceutical pouch market.

50 ml to 500 ml Capacity Pouches Are the Fastest Growing Segment, Meeting the Demand for Small to Medium Volume Packaging

The 50 ml to 500 ml capacity pouches are the fastest-growing segment in the pharmaceutical pouch market, driven by their suitability for small to medium-sized pharmaceutical products. This capacity range is increasingly preferred for packaging liquid medications, oral suspensions, and even some topical formulations, as it provides the right balance between consumer convenience and storage efficiency.

As the demand for liquid medications, particularly for pediatric and geriatric populations, continues to grow, the need for packaging that ensures product stability and easy administration is becoming more critical. Pouches in the 50 ml to 500 ml range offer ease of use, space-saving benefits, and protection against environmental factors such as air and moisture. Additionally, this capacity range is ideal for products like oral liquid antibiotics, digestive aids, and nutritional supplements, contributing to its rapid growth in the market.

Pharmaceutical Manufacturers Lead the End-Use Industry, Driven by Large-Scale Drug Production and Packaging Requirements

Pharmaceutical manufacturers are the largest end-use industry for pharmaceutical pouches, as they are directly involved in the mass production and packaging of pharmaceutical products. These manufacturers require flexible, reliable, and cost-effective packaging solutions that can protect their products, ensure compliance with industry regulations, and meet consumer demands for convenience and portability. Pouches provide an efficient and space-saving solution for both liquid and solid dosage forms, making them an essential packaging format for a wide range of pharmaceutical products.

With the growing global demand for pharmaceuticals, manufacturers are increasingly adopting advanced pouch packaging solutions that incorporate features such as tamper-evident seals, easy-opening mechanisms, and child-resistant packaging. As a result, the pharmaceutical manufacturing sector is expected to continue driving the growth of the pharmaceutical pouch market.

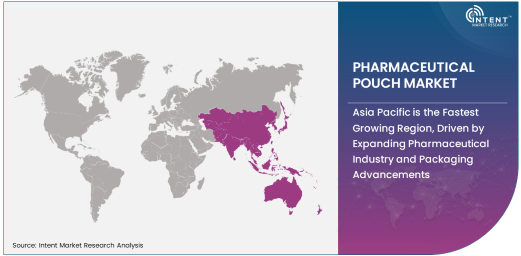

Asia Pacific is the Fastest Growing Region, Driven by Expanding Pharmaceutical Industry and Packaging Advancements

Asia Pacific is the fastest-growing region in the pharmaceutical pouch market, fueled by the rapidly expanding pharmaceutical industry and increased demand for innovative packaging solutions. The region’s growing population, rising healthcare needs, and increasing access to healthcare services are driving the demand for pharmaceutical products, which in turn increases the need for efficient and safe packaging solutions.

Countries such as China and India are at the forefront of the growth in pharmaceutical production and consumption, and the demand for packaging solutions that meet international standards is growing rapidly. The rise of local pharmaceutical manufacturers, combined with advancements in packaging technology, is helping to propel the pharmaceutical pouch market forward in the Asia Pacific region. Additionally, the trend toward sustainable and eco-friendly packaging solutions is gaining momentum in the region, further contributing to the market’s growth.

Competitive Landscape and Key Players

The pharmaceutical pouch market is competitive, with several key players offering a range of packaging solutions tailored to the needs of pharmaceutical manufacturers, contract manufacturing organizations, and research institutions. Leading players in the market include Amcor Limited, Sealed Air Corporation, Berry Global Inc., Huhtamaki Group, and Winpak Ltd. These companies are focusing on product innovation, sustainability, and technological advancements to strengthen their market positions.

Strategic collaborations, mergers, and acquisitions are common in this market as companies aim to expand their product portfolios and meet the growing demand for high-quality, eco-friendly pharmaceutical packaging. The competitive landscape is further intensified by the shift toward advanced packaging solutions, such as biodegradable and recyclable pouches, and the increasing adoption of automation and digital technologies to enhance manufacturing processes.

Recent Developments:

- Amcor Ltd. launched a new range of pharmaceutical pouches made from recyclable materials, aimed at reducing the environmental impact of packaging.

- Mondi Group expanded its production capabilities in pharmaceutical pouch packaging to meet growing demand in the European market.

- Sealed Air Corporation introduced a sterile pharmaceutical pouch designed to improve drug safety during transportation and storage.

- Huhtamaki Oyj entered into a partnership with a pharmaceutical company to provide custom-designed pouches for liquid and solid dosage forms.

- Berry Global, Inc. developed a new series of tamper-evident pharmaceutical pouches, improving the security and compliance of pharmaceutical packaging.

List of Leading Companies:

- Amcor Ltd.

- Mondi Group

- Sealed Air Corporation

- Huhtamaki Oyj

- Bemis Company, Inc.

- Berry Global, Inc.

- Sonoco Products Company

- Groupe Guillin

- Smurfit Kappa Group

- Fresenius Kabi

- Uflex Limited

- Wipak Walsrode GmbH & Co. KG

- Constantia Flexibles

- DuPont

- FlexPak Corporation

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 4.8 Billion |

|

Forecasted Value (2030) |

USD 8.9 Billion |

|

CAGR (2025 – 2030) |

10.8% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Global Pharmaceutical Pouch Market by Material Type (Polyethylene (PE), Polypropylene (PP), Aluminum Foil, Paper & Plastic Laminates, Other Materials), by Product Type (Single Pouch, Multi Pouch, Zipper Pouch, Stand-Up Pouch, Gusseted Pouch), by Capacity (Less than 50 ml, 50 ml to 500 ml, More than 500 ml), by End-Use Industry (Pharmaceutical Manufacturers, Contract Manufacturing Organizations (CMOs), Research & Development (R&D)); Insights & Forecast (2024 – 2030) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Amcor Ltd., Mondi Group, Sealed Air Corporation, Huhtamaki Oyj, Bemis Company, Inc., Berry Global, Inc., Groupe Guillin, Smurfit Kappa Group, Fresenius Kabi, Uflex Limited, Wipak Walsrode GmbH & Co. KG, Constantia Flexibles, FlexPak Corporation |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Pharmaceutical Pouch Market, by Material Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Polyethylene (PE) |

|

4.2. Polypropylene (PP) |

|

4.3. Aluminum Foil |

|

4.4. Paper & Plastic Laminates |

|

4.5. Other Materials |

|

5. Pharmaceutical Pouch Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Single Pouch |

|

5.2. Multi Pouch |

|

5.3. Zipper Pouch |

|

5.4. Stand-Up Pouch |

|

5.5. Gusseted Pouch |

|

6. Pharmaceutical Pouch Market, by Capacity (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Less than 50 ml |

|

6.2. 50 ml to 500 ml |

|

6.3. More than 500 ml |

|

7. Pharmaceutical Pouch Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Pharmaceutical Manufacturers |

|

7.2. Contract Manufacturing Organizations (CMOs) |

|

7.3. Research & Development (R&D) |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Pharmaceutical Pouch Market, by Material Type |

|

8.2.7. North America Pharmaceutical Pouch Market, by Product Type |

|

8.2.8. North America Pharmaceutical Pouch Market, by Capacity |

|

8.2.9. North America Pharmaceutical Pouch Market, by End-Use Industry |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Pharmaceutical Pouch Market, by Material Type |

|

8.2.10.1.2. US Pharmaceutical Pouch Market, by Product Type |

|

8.2.10.1.3. US Pharmaceutical Pouch Market, by Capacity |

|

8.2.10.1.4. US Pharmaceutical Pouch Market, by End-Use Industry |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Amcor Ltd. |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Mondi Group |

|

10.3. Sealed Air Corporation |

|

10.4. Huhtamaki Oyj |

|

10.5. Bemis Company, Inc. |

|

10.6. Berry Global, Inc. |

|

10.7. Sonoco Products Company |

|

10.8. Groupe Guillin |

|

10.9. Smurfit Kappa Group |

|

10.10. Fresenius Kabi |

|

10.11. Uflex Limited |

|

10.12. Wipak Walsrode GmbH & Co. KG |

|

10.13. Constantia Flexibles |

|

10.14. DuPont |

|

10.15. FlexPak Corporation |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Pharmaceutical Pouch Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Pharmaceutical Pouch Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Pharmaceutical Pouch Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA