As per Intent Market Research, the Pharmaceutical Plastic Bottles Market was valued at USD 8.9 Billion in 2024-e and will surpass USD 15.3 Billion by 2030; growing at a CAGR of 9.5% during 2025 - 2030.

The pharmaceutical plastic bottles market is integral to the packaging and distribution of pharmaceutical products, offering a wide range of packaging solutions that meet the specific requirements of the industry. As the demand for pharmaceutical products continues to rise globally, the need for safe, effective, and cost-efficient packaging solutions is more critical than ever. Plastic bottles are widely used for the packaging of liquid medications, tablets, capsules, and ointments due to their durability, cost-effectiveness, and ability to protect the contents from contamination. The market is driven by technological advancements in packaging materials, along with growing concerns about sustainability and regulatory compliance in packaging. The shift towards eco-friendly materials, such as recyclable and biodegradable plastics, is further boosting the demand for pharmaceutical plastic bottles.

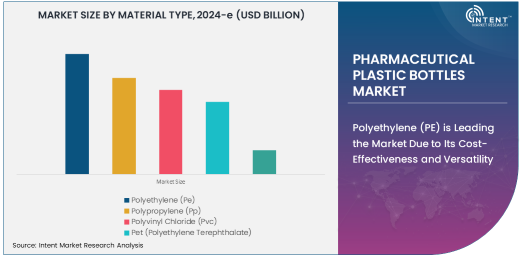

Polyethylene (PE) is Leading the Market Due to Its Cost-Effectiveness and Versatility

Polyethylene (PE) is the dominant material type in the pharmaceutical plastic bottles market, owing to its cost-effectiveness, flexibility, and versatility in various applications. PE plastic bottles are commonly used for packaging liquid medications, as they provide excellent protection against external elements such as moisture and air, which can degrade the product. The material's ability to be molded into a variety of shapes and sizes allows for customization, making it ideal for the packaging of both small and large quantities of medications.

PE plastic bottles are also favored for their lightweight nature, which helps reduce shipping costs and the overall carbon footprint of pharmaceutical products. The material's compatibility with a wide range of medications, including both aqueous and non-aqueous solutions, contributes to its widespread adoption across the pharmaceutical industry. As the demand for cost-effective packaging solutions grows, the use of PE in pharmaceutical bottles is expected to maintain its leading position in the market.

Bottles for Liquid Medications Are the Largest Product Segment Due to High Demand in the Pharmaceutical Industry

Bottles for liquid medications are the largest product segment in the pharmaceutical plastic bottles market, driven by the widespread use of liquid formulations in the treatment of various medical conditions. Liquid medications, including syrups, suspensions, and oral solutions, require packaging that preserves the integrity and stability of the product, while also being easy to dispense. Plastic bottles provide an excellent solution for these needs, offering leak-proof, tamper-evident, and user-friendly features.

The increasing prevalence of chronic diseases, such as diabetes, respiratory disorders, and gastrointestinal diseases, which often require liquid medications, is contributing to the growth of this segment. Moreover, the growing trend toward pediatric medications in liquid form further fuels the demand for plastic bottles in this category. As a result, bottles for liquid medications continue to hold the largest share of the pharmaceutical plastic bottles market.

100 ml to 500 ml Capacity Bottles Are the Fastest Growing Segment Due to Their Versatility

Bottles with a capacity ranging from 100 ml to 500 ml are the fastest-growing segment in the pharmaceutical plastic bottles market. These medium-sized bottles are increasingly in demand due to their versatility in packaging various pharmaceutical products, including both liquid medications and ointments. The 100 ml to 500 ml capacity range offers an ideal balance between convenience for consumers and storage efficiency for pharmaceutical companies.

This capacity range is particularly popular for products like liquid antibiotics, anti-inflammatory syrups, and vitamins, as it is large enough to accommodate a reasonable dosage while remaining compact for easy handling and storage. The rapid growth of this segment is driven by the rising number of over-the-counter medications and the increasing need for packaging solutions that are both user-friendly and capable of accommodating larger quantities of liquid formulations. Additionally, the preference for this size bottle is also influenced by the growing demand for pediatric liquid medicines, which often require medium-sized packaging.

Pharmaceutical Companies Are the Largest End-Use Industry Due to Direct Involvement in Drug Production

Pharmaceutical companies are the largest end-use industry in the pharmaceutical plastic bottles market, as they are directly involved in the production and packaging of medications. These companies require reliable and high-quality packaging solutions to ensure the safety and efficacy of their products. Plastic bottles are ideal for pharmaceutical packaging, offering a durable, cost-effective, and customizable solution for various drug formulations.

As pharmaceutical companies continue to expand their product lines and meet the growing global demand for medications, the need for packaging solutions that maintain product integrity while complying with stringent regulatory standards is more important than ever. Pharmaceutical companies are increasingly adopting advanced plastic packaging technologies to ensure that their products are well-protected, tamper-proof, and convenient for consumers. This demand is expected to drive continued growth in the pharmaceutical plastic bottles market.

North America is the Largest Region Due to Strong Pharmaceutical Industry Presence and Advanced Packaging Solutions

North America is the largest region in the pharmaceutical plastic bottles market, owing to the strong presence of pharmaceutical companies and the increasing demand for advanced packaging solutions. The United States, in particular, is home to some of the largest pharmaceutical manufacturers in the world, who require high-quality packaging materials to meet the needs of the industry. Furthermore, the region's established healthcare infrastructure and regulatory frameworks ensure the continued demand for safe and compliant packaging for pharmaceutical products.

The growth of the North American pharmaceutical plastic bottles market is also driven by the region's focus on sustainability and environmental concerns. With an increasing emphasis on recyclable and eco-friendly packaging solutions, North American companies are adopting more sustainable plastic alternatives, such as polyethylene terephthalate (PET), in their packaging. The region's adoption of advanced technologies in packaging and its large pharmaceutical market share position North America as the largest and fastest-growing market for pharmaceutical plastic bottles.

Competitive Landscape and Key Players

The pharmaceutical plastic bottles market is competitive, with several key players providing a wide range of packaging solutions to meet the needs of pharmaceutical companies, contract manufacturers, and research and development organizations. Major players in the market include Amcor Limited, Gerresheimer AG, Berry Global Inc., WestRock Company, and AptarGroup, Inc., among others. These companies are focusing on innovation and sustainability to capture a larger market share by offering advanced, eco-friendly packaging solutions, as well as meeting stringent regulatory requirements.

In addition to offering a variety of plastic materials such as polyethylene (PE), polypropylene (PP), and polyethylene terephthalate (PET), leading players are also expanding their product portfolios by introducing bottles of varying sizes and designs to cater to the growing demand for pharmaceutical packaging. Strategic partnerships, mergers, and acquisitions are common strategies among key players to strengthen their market position and enhance their product offerings. The competitive landscape is expected to continue evolving as pharmaceutical companies increasingly prioritize high-quality, sustainable, and cost-effective packaging solutions.

Recent Developments:

- Amcor Ltd. launched a new sustainable PET plastic bottle designed for pharmaceutical applications, offering enhanced recyclability and reducing carbon footprint.

- Berry Global, Inc. announced the expansion of its production facilities to meet the growing demand for pharmaceutical plastic packaging in North America.

- Gerresheimer AG introduced a new child-resistant plastic bottle specifically designed for liquid medications, improving safety and compliance.

- Silgan Holdings Inc. acquired Plastipak Packaging, expanding its capabilities in providing plastic bottles for the pharmaceutical industry.

- Alpla Group partnered with a pharmaceutical manufacturer to develop eco-friendly plastic bottles made from recycled PET (rPET) for over-the-counter drug packaging.

List of Leading Companies:

- Amcor Ltd.

- Gerresheimer AG

- Berry Global, Inc.

- Silgan Holdings Inc.

- Alpla Group

- Bormioli Pharma

- RPC Group

- Sonoco Products Company

- Unilux Group

- Pragati Plastic

- West Pharmaceutical Services, Inc.

- Lummus Technology

- Zhejiang Materials Industry Group Co., Ltd.

- Interpack

- Huhtamaki Oyj

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 8.9 Billion |

|

Forecasted Value (2030) |

USD 15.3 Billion |

|

CAGR (2025 – 2030) |

9.5% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Global Pharmaceutical Plastic Bottles Market by Material Type (Polyethylene (PE), Polypropylene (PP), Polyvinyl Chloride (PVC), PET (Polyethylene Terephthalate), Other Materials), by Product Type (Bottles for Liquid Medications, Bottles for Tablets and Capsules, Bottles for Powdered Medications, Bottles for Ointments and Creams), by Capacity (Less than 100 ml, 100 ml to 500 ml, More than 500 ml), by End-Use Industry (Pharmaceutical Companies, Contract Manufacturing Organizations (CMOs), Research & Development (R&D)); Insights & Forecast (2024 – 2030) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Amcor Ltd., Gerresheimer AG, Berry Global, Inc., Silgan Holdings Inc., Alpla Group, Bormioli Pharma, Sonoco Products Company, Unilux Group, Pragati Plastic, West Pharmaceutical Services, Inc., Lummus Technology, Zhejiang Materials Industry Group Co., Ltd., Huhtamaki Oyj |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Pharmaceutical Plastic Bottles Market, by Material Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Polyethylene (PE) |

|

4.2. Polypropylene (PP) |

|

4.3. Polyvinyl Chloride (PVC) |

|

4.4. PET (Polyethylene Terephthalate) |

|

4.5. Other Materials |

|

5. Pharmaceutical Plastic Bottles Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Bottles for Liquid Medications |

|

5.2. Bottles for Tablets and Capsules |

|

5.3. Bottles for Powdered Medications |

|

5.4. Bottles for Ointments and Creams |

|

6. Pharmaceutical Plastic Bottles Market, by Capacity (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Less than 100 ml |

|

6.2. 100 ml to 500 ml |

|

6.3. More than 500 ml |

|

7. Pharmaceutical Plastic Bottles Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Pharmaceutical Companies |

|

7.2. Contract Manufacturing Organizations (CMOs) |

|

7.3. Research & Development (R&D) |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Pharmaceutical Plastic Bottles Market, by Material Type |

|

8.2.7. North America Pharmaceutical Plastic Bottles Market, by Product Type |

|

8.2.8. North America Pharmaceutical Plastic Bottles Market, by Capacity |

|

8.2.9. North America Pharmaceutical Plastic Bottles Market, by End-Use Industry |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Pharmaceutical Plastic Bottles Market, by Material Type |

|

8.2.10.1.2. US Pharmaceutical Plastic Bottles Market, by Product Type |

|

8.2.10.1.3. US Pharmaceutical Plastic Bottles Market, by Capacity |

|

8.2.10.1.4. US Pharmaceutical Plastic Bottles Market, by End-Use Industry |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Amcor Ltd. |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Gerresheimer AG |

|

10.3. Berry Global, Inc. |

|

10.4. Silgan Holdings Inc. |

|

10.5. Alpla Group |

|

10.6. Bormioli Pharma |

|

10.7. RPC Group |

|

10.8. Sonoco Products Company |

|

10.9. Unilux Group |

|

10.10. Pragati Plastic |

|

10.11. West Pharmaceutical Services, Inc. |

|

10.12. Lummus Technology |

|

10.13. Zhejiang Materials Industry Group Co., Ltd. |

|

10.14. Interpack |

|

10.15. Huhtamaki Oyj |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Pharmaceutical Plastic Bottles Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Pharmaceutical Plastic Bottles Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Pharmaceutical Plastic Bottles Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA