As per Intent Market Research, the Pharmaceutical Manufacturing Market was valued at USD 912.2 Billion in 2024-e and will surpass USD 1435.6 Billion by 2030; growing at a CAGR of 7.9% during 2025 - 2030.

The pharmaceutical manufacturing market is integral to the global healthcare industry, encompassing the production of active pharmaceutical ingredients (APIs), finished dosage forms (FDF), and biologics, along with the services provided by contract manufacturing organizations (CMOs). This market is pivotal in ensuring the availability of drugs and biologics to address the growing global healthcare needs. Advancements in manufacturing technologies such as automation, continuous manufacturing, and 3D printing are transforming the industry, improving efficiency, and enabling the production of complex drugs and biologics. As the pharmaceutical landscape evolves with the rise of personalized medicine and biologics, the demand for advanced manufacturing techniques will continue to increase, fostering innovation within the sector.

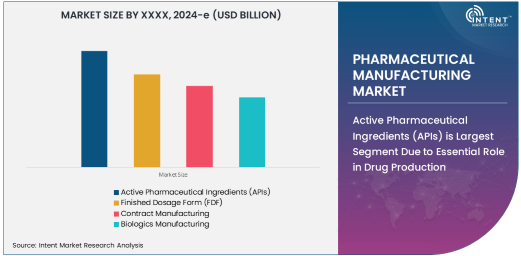

Active Pharmaceutical Ingredients (APIs) is Largest Segment Due to Essential Role in Drug Production

The Active Pharmaceutical Ingredients (APIs) segment is the largest in the pharmaceutical manufacturing market due to the critical role APIs play in the creation of pharmaceutical products. APIs are the biologically active components in drugs that produce the desired therapeutic effect. As the foundation of drug formulations, APIs are indispensable in the development of both generic and branded drugs. The increasing global demand for medications, especially with the rise of chronic diseases, an aging population, and expanding healthcare access, has propelled the need for API production.

In addition, the shift toward biologic drugs, which require more complex and specialized API manufacturing processes, has significantly boosted this segment's growth. The increasing prevalence of diseases such as cancer, diabetes, and autoimmune disorders has led to a surge in the demand for APIs for the production of biologics and biosimilars. Moreover, the growing trend of outsourcing API manufacturing to contract manufacturing organizations (CMOs) has further accelerated the growth of the APIs segment, as pharmaceutical companies focus on their core competencies while outsourcing production to specialized manufacturers.

Continuous Manufacturing is Fastest Growing Technology Due to Enhanced Efficiency and Flexibility

Continuous manufacturing is the fastest-growing technology within the pharmaceutical manufacturing market, offering significant advantages in terms of efficiency, flexibility, and scalability. Unlike traditional batch manufacturing, where production is done in discrete steps, continuous manufacturing involves the ongoing production of pharmaceuticals in a continuous process. This technology allows for better control over product quality, reduces production time, and minimizes waste, making it an increasingly attractive option for pharmaceutical manufacturers.

Continuous manufacturing is particularly beneficial for the production of complex and high-demand medications, including biologics and personalized therapies. The ability to continuously produce small batches or large quantities of drugs with consistent quality makes it a key technology in the industry. With the increasing pressure to lower drug production costs, improve supply chain efficiency, and meet regulatory requirements, continuous manufacturing is gaining traction as the preferred method for many pharmaceutical companies. This trend is expected to accelerate as more manufacturers adopt this technology to streamline their operations and improve production outcomes.

Pharmaceutical Companies Are Largest End-Use Industry Due to Need for In-House Manufacturing Capabilities

Pharmaceutical companies are the largest end-use industry in the pharmaceutical manufacturing market, owing to their need for in-house manufacturing capabilities to produce their drug products. These companies rely on both traditional and advanced manufacturing methods to produce APIs, FDFs, and biologics that are essential for addressing a wide range of medical conditions. As pharmaceutical companies continue to innovate and expand their product portfolios, they require robust manufacturing processes to scale production while maintaining high standards of quality and compliance with regulatory requirements.

The pharmaceutical industry is increasingly investing in advanced manufacturing technologies, including automation, continuous manufacturing, and advanced process control, to improve efficiency and reduce costs. Moreover, pharmaceutical companies are outsourcing certain manufacturing processes to contract manufacturing organizations (CMOs) to focus on core activities such as research and development (R&D) and marketing. Despite the outsourcing trend, pharmaceutical companies remain the dominant end-users of manufacturing technologies, as they are responsible for the largest share of drug production and distribution worldwide.

North America Is Largest Region Due to Strong Pharmaceutical Manufacturing Infrastructure and Regulatory Environment

North America is the largest region in the pharmaceutical manufacturing market, driven by its well-established pharmaceutical manufacturing infrastructure and stringent regulatory environment. The U.S., in particular, is home to some of the world's largest pharmaceutical companies, research institutions, and contract manufacturing organizations. The presence of major pharmaceutical firms and the rapid adoption of advanced manufacturing technologies contribute to North America's market dominance.

Additionally, North America benefits from a robust healthcare system, significant investments in biotechnology, and a supportive regulatory framework that ensures the safety, efficacy, and quality of pharmaceutical products. The region's emphasis on innovation in drug development, particularly in biologics, personalized medicine, and biosimilars, further strengthens its position in the global pharmaceutical manufacturing market. With the continued growth of pharmaceutical production and innovation in the region, North America is expected to maintain its leadership in this market.

Competitive Landscape and Key Players

The pharmaceutical manufacturing market is highly competitive, with several key players offering a range of manufacturing solutions for API production, finished dosage forms, biologics, and contract manufacturing services. Prominent companies in this market include Pfizer, Novartis, Roche, GlaxoSmithKline, Lonza Group, and Catalent, among others. These companies leverage advanced manufacturing technologies such as automation, continuous manufacturing, and advanced process control to improve operational efficiency, reduce costs, and ensure product quality.

Contract manufacturing organizations (CMOs) such as Samsung Biologics, WuXi AppTec, and Lonza Group are crucial players, providing outsourced manufacturing services to pharmaceutical companies, biotech firms, and generic drug manufacturers. These CMOs play a vital role in enabling pharmaceutical companies to scale production while focusing on drug discovery and development. The competitive landscape is characterized by mergers, acquisitions, and partnerships aimed at expanding manufacturing capabilities and accessing new markets. With the increasing complexity of drug production and a rising demand for personalized and biologic therapies, the pharmaceutical manufacturing market will continue to evolve, presenting new opportunities for innovation and growth.

Recent Developments:

- Pfizer Inc. expanded its biologics manufacturing capacity with the acquisition of a new facility in Europe aimed at increasing the production of vaccines and biologic therapies.

- Novartis International AG implemented continuous manufacturing technology at one of its production sites, increasing efficiency and improving product consistency.

- Bayer AG launched a new biotech manufacturing plant in Asia to cater to the growing demand for biologic drugs and gene therapies in the region.

- Merck & Co., Inc. entered a partnership with a contract manufacturing organization (CMO) to scale up production of its leading cancer immunotherapy treatment.

- GlaxoSmithKline PLC invested in advanced process control systems at its manufacturing facilities to enhance the production of oral and injectable medications.

List of Leading Companies:

- Pfizer Inc.

- Novartis International AG

- Sanofi S.A.

- Bayer AG

- GlaxoSmithKline PLC

- Eli Lilly and Company

- Merck & Co., Inc.

- AbbVie Inc.

- Johnson & Johnson

- Roche Holding AG

- AstraZeneca PLC

- Bristol-Myers Squibb Company

- Teva Pharmaceutical Industries Ltd.

- Amgen Inc.

- Gilead Sciences, Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 912.2 Billion |

|

Forecasted Value (2030) |

USD 1435.6 Billion |

|

CAGR (2025 – 2030) |

7.9% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Global Pharmaceutical Manufacturing Market by Type (Active Pharmaceutical Ingredients (APIs), Finished Dosage Form (FDF), Contract Manufacturing, Biologics Manufacturing), by Technology (Traditional Manufacturing, Continuous Manufacturing, 3D Printing in Pharma, Advanced Process Control, Automation in Manufacturing), by End-Use Industry (Pharmaceutical Companies, Contract Manufacturing Organizations (CMOs), Biotech Companies, Generic Drug Manufacturers, Research & Development (R&D)); Insights & Forecast (2024 – 2030) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Pfizer Inc., Novartis International AG, Sanofi S.A., Bayer AG, GlaxoSmithKline PLC, Eli Lilly and Company, AbbVie Inc., Johnson & Johnson, Roche Holding AG, AstraZeneca PLC, Bristol-Myers Squibb Company, Teva Pharmaceutical Industries Ltd., Gilead Sciences, Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Pharmaceutical Manufacturing Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Active Pharmaceutical Ingredients (APIs) |

|

4.2. Finished Dosage Form (FDF) |

|

4.3. Contract Manufacturing |

|

4.4. Biologics Manufacturing |

|

5. Pharmaceutical Manufacturing Market, by Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Traditional Manufacturing |

|

5.2. Continuous Manufacturing |

|

5.3. 3D Printing in Pharma |

|

5.4. Advanced Process Control |

|

5.5. Automation in Manufacturing |

|

6. Pharmaceutical Manufacturing Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Pharmaceutical Companies |

|

6.2. Contract Manufacturing Organizations (CMOs) |

|

6.3. Biotech Companies |

|

6.4. Generic Drug Manufacturers |

|

6.5. Research & Development (R&D) |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Pharmaceutical Manufacturing Market, by Type |

|

7.2.7. North America Pharmaceutical Manufacturing Market, by Technology |

|

7.2.8. North America Pharmaceutical Manufacturing Market, by End-Use Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Pharmaceutical Manufacturing Market, by Type |

|

7.2.9.1.2. US Pharmaceutical Manufacturing Market, by Technology |

|

7.2.9.1.3. US Pharmaceutical Manufacturing Market, by End-Use Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Pfizer Inc. |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Novartis International AG |

|

9.3. Sanofi S.A. |

|

9.4. Bayer AG |

|

9.5. GlaxoSmithKline PLC |

|

9.6. Eli Lilly and Company |

|

9.7. Merck & Co., Inc. |

|

9.8. AbbVie Inc. |

|

9.9. Johnson & Johnson |

|

9.10. Roche Holding AG |

|

9.11. AstraZeneca PLC |

|

9.12. Bristol-Myers Squibb Company |

|

9.13. Teva Pharmaceutical Industries Ltd. |

|

9.14. Amgen Inc. |

|

9.15. Gilead Sciences, Inc. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Pharmaceutical Manufacturing Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Pharmaceutical Manufacturing Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Pharmaceutical Manufacturing Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA