As per Intent Market Research, the Packaging Robots Market was valued at USD 6.3 Billion in 2024-e and will surpass USD 11.4 Billion by 2030; growing at a CAGR of 10.5% during 2025-2030.

The packaging robots market has witnessed significant growth in recent years, driven by advancements in automation technologies and the growing demand for efficiency in packaging processes. These robots are designed to perform tasks such as sorting, packaging, labeling, and palletizing, offering substantial benefits in terms of speed, accuracy, and labor cost savings. As industries strive for greater operational efficiency and precision, robotic solutions have become indispensable in packaging lines across various sectors. The rise in e-commerce and the increasing emphasis on automation in manufacturing have further propelled the adoption of packaging robots.

The market is also benefiting from innovations in robotics, including the integration of artificial intelligence (AI), machine learning, and the development of collaborative robots (cobots), which can work alongside human operators to enhance productivity. Packaging robots are now more adaptable, flexible, and capable of handling a wide range of packaging materials, which allows businesses to meet the increasing demand for faster and more efficient packaging solutions. As industries focus on improving productivity and reducing human error, the packaging robots market is expected to continue its upward trajectory.

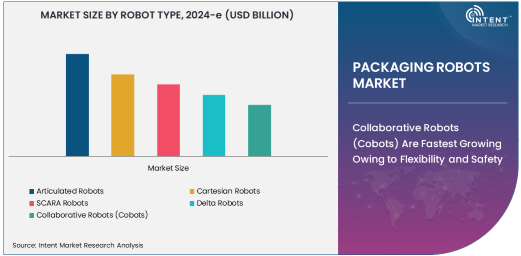

Collaborative Robots (Cobots) Are Fastest Growing Owing to Flexibility and Safety

Collaborative robots (cobots) represent the fastest-growing segment in the packaging robots market, owing to their ability to work alongside human workers in a shared workspace. Cobots are designed to perform repetitive and ergonomically challenging tasks while ensuring safety and minimizing the risk of accidents. This collaborative nature makes cobots highly suitable for packaging tasks where human intervention is still required, such as in food and beverage, pharmaceutical, and e-commerce packaging. Their ease of integration into existing production lines, combined with their relatively low cost and versatility, has made them increasingly popular in industries seeking to improve operational efficiency without fully automating their packaging processes.

The ability of cobots to assist human workers and handle complex tasks such as packing fragile items or sorting products has contributed significantly to their growing adoption. Additionally, cobots are equipped with advanced sensors and AI-driven capabilities, allowing them to adapt to various tasks and environments with minimal reprogramming. These advantages make cobots an attractive choice for companies looking for flexible and cost-effective automation solutions. The growing demand for collaborative robots is expected to continue as businesses strive for smarter, safer, and more efficient packaging operations.

Food & Beverage Industry Is Largest End-User Due to High Packaging Volume

The food and beverage industry is the largest end-user of packaging robots, driven by the need for high-speed and high-volume packaging solutions. The industry requires efficient packaging processes to handle a wide range of products, from beverages to snacks, under strict hygiene and safety standards. Packaging robots help streamline these processes, ensuring fast and accurate packaging while maintaining consistency and quality. The demand for automation in food and beverage packaging is also growing due to labor shortages, regulatory pressures, and the need for higher throughput.

As consumer demand for packaged goods continues to rise, particularly in the processed food sector, packaging robots are increasingly deployed to meet the operational demands of food manufacturers. Automated systems also help improve shelf-life and reduce waste, which are essential factors in the highly competitive food and beverage industry. The ability of packaging robots to handle different types of packaging materials and adapt to changing production needs is contributing to their growing adoption in this sector. As food and beverage companies continue to invest in automation to meet the demands of mass production, packaging robots are expected to remain a critical component of the industry’s packaging operations.

Asia-Pacific Region Is Largest Owing to Manufacturing Hub and Automation Growth

The Asia-Pacific region is the largest market for packaging robots, primarily due to its strong manufacturing base and increasing adoption of automation across various industries. Countries such as China, Japan, South Korea, and India are leading the market, where a significant number of packaging operations are being automated to enhance efficiency and meet the growing demand for packaged goods. The region's dominance in manufacturing, coupled with the rise of e-commerce and retail packaging, has made it a key market for packaging robots.

In addition to the manufacturing sector, the food and beverage industry in the Asia-Pacific region is rapidly adopting robotic packaging solutions to meet the rising demand for packaged food products. The growing trend of automation in industries like pharmaceuticals and electronics is also contributing to the region's leadership in the packaging robots market. With a focus on improving productivity and reducing labor costs, companies in Asia-Pacific are increasingly investing in packaging robots. The region's large-scale industrial base and technological advancements make it the largest market for packaging robots globally.

Leading Companies and Competitive Landscape

The packaging robots market is highly competitive, with several key players focusing on innovation and technological advancements to maintain a competitive edge. Leading companies in the market include ABB Ltd., FANUC Corporation, KUKA AG, Universal Robots, and Yaskawa Electric Corporation. These companies specialize in providing robotic solutions that cater to the unique requirements of packaging applications, offering products that range from articulated and SCARA robots to collaborative robots (cobots).

The competitive landscape is characterized by a growing emphasis on research and development, with companies investing in new technologies such as AI, machine learning, and advanced sensors to enhance the capabilities of packaging robots. Additionally, collaborations and partnerships are becoming increasingly common as companies work to integrate their robotic systems with other automation solutions in packaging lines. As demand for packaging robots continues to grow, companies are also focusing on providing tailored solutions that meet the specific needs of various industries, including food and beverage, pharmaceuticals, and e-commerce packaging. The ongoing trend towards customization and flexibility is expected to drive further competition and innovation in the market.

Recent Developments:

- ABB Ltd. launched a new series of collaborative robots for packaging applications, focusing on improving flexibility and safety for smaller packaging operations.

- FANUC Corporation introduced an advanced articulated robot designed specifically for high-speed, high-precision packaging in the food and beverage sector.

- KUKA AG unveiled a new robotic system for pharmaceutical packaging that combines precision with speed for automated filling and labeling.

- Universal Robots A/S released a collaborative robot designed for packaging small items in e-commerce, improving operational efficiency and reducing packaging time.

- Yaskawa Electric Corporation developed a robotic packaging system that integrates with existing production lines to provide automated packing solutions for the electronics industry.

List of Leading Companies:

- ABB Ltd.

- FANUC Corporation

- KUKA AG

- Yaskawa Electric Corporation

- Kawasaki Heavy Industries, Ltd.

- Universal Robots A/S

- Mitsubishi Electric Corporation

- Denso Wave Inc.

- Rethink Robotics

- Omron Corporation

- Stäubli Robotics

- Rockwell Automation, Inc.

- Schneider Electric SE

- Comau S.p.A.

- Teradyne, Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 6.3 Billion |

|

Forecasted Value (2030) |

USD 11.4 Billion |

|

CAGR (2025 – 2030) |

10.5% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Packaging Robots Market By Robot Type (Articulated Robots, Cartesian Robots, SCARA Robots, Delta Robots, Collaborative Robots), By Application (Food & Beverage Packaging, Pharmaceutical Packaging, Cosmetics Packaging, Consumer Electronics Packaging, E-commerce & Retail Packaging), and By End-User Industry (Food & Beverage, Pharmaceuticals, Cosmetics & Personal Care, Electronics, E-commerce & Retail) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

ABB Ltd., FANUC Corporation, KUKA AG, Yaskawa Electric Corporation, Kawasaki Heavy Industries, Ltd., Universal Robots A/S, Mitsubishi Electric Corporation, Denso Wave Inc., Rethink Robotics, Omron Corporation, Stäubli Robotics, Rockwell Automation, Inc., Schneider Electric SE, Comau S.p.A., Teradyne, Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Packaging Robots Market, by Robot Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Articulated Robots |

|

4.2. Cartesian Robots |

|

4.3. SCARA Robots |

|

4.4. Delta Robots |

|

4.5. Collaborative Robots (Cobots) |

|

5. Packaging Robots Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Food & Beverage Packaging |

|

5.2. Pharmaceutical Packaging |

|

5.3. Cosmetics Packaging |

|

5.4. Consumer Electronics Packaging |

|

5.5. E-commerce & Retail Packaging |

|

5.6. Others |

|

6. Packaging Robots Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Food & Beverage |

|

6.2. Pharmaceuticals |

|

6.3. Cosmetics & Personal Care |

|

6.4. Electronics |

|

6.5. E-commerce & Retail |

|

6.6. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Packaging Robots Market, by Robot Type |

|

7.2.7. North America Packaging Robots Market, by Application |

|

7.2.8. North America Packaging Robots Market, by End-User Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Packaging Robots Market, by Robot Type |

|

7.2.9.1.2. US Packaging Robots Market, by Application |

|

7.2.9.1.3. US Packaging Robots Market, by End-User Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. ABB Ltd. |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. FANUC Corporation |

|

9.3. KUKA AG |

|

9.4. Yaskawa Electric Corporation |

|

9.5. Kawasaki Heavy Industries, Ltd. |

|

9.6. Universal Robots A/S |

|

9.7. Mitsubishi Electric Corporation |

|

9.8. Denso Wave Inc. |

|

9.9. Rethink Robotics |

|

9.10. Omron Corporation |

|

9.11. Stäubli Robotics |

|

9.12. Rockwell Automation, Inc. |

|

9.13. Schneider Electric SE |

|

9.14. Comau S.p.A. |

|

9.15. Teradyne, Inc. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Packaging Robots Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Packaging Robots Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Packaging Robots Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA