As per Intent Market Research, the Packaging Printing Market was valued at USD 23.5 Billion in 2024-e and will surpass USD 35.1 Billion by 2030; growing at a CAGR of 6.9% during 2025-2030.

The packaging printing market plays a pivotal role in the global packaging industry, ensuring that products are visually appealing, informative, and compliant with regulatory requirements. With the growing demand for branded products, effective packaging has become essential for companies looking to differentiate their offerings in competitive markets. Packaging printing is used to apply logos, graphics, product information, and other branding elements to various packaging materials, including plastic, glass, metal, and paper. The market is influenced by factors such as advancements in printing technology, increasing consumer preference for visually appealing packaging, and the rising demand for eco-friendly packaging solutions. As industries continue to evolve, the packaging printing market is expected to grow, driven by innovations in printing techniques that improve quality, speed, and cost-effectiveness.

The market is also being shaped by shifting consumer expectations, with an increased emphasis on sustainability and the growing demand for packaging that is not only functional but also eco-friendly. Digital and flexographic printing, in particular, have gained significant traction due to their ability to produce high-quality prints with minimal environmental impact. Additionally, regulatory changes in industries such as food and beverages, pharmaceuticals, and cosmetics, requiring clear labeling and information, are fueling the demand for packaging printing services.

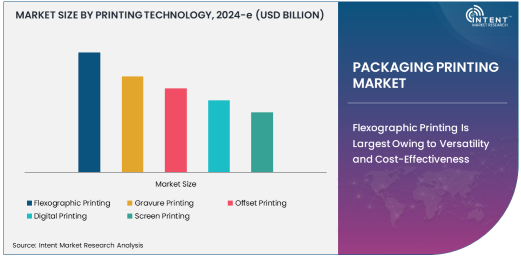

Flexographic Printing Is Largest Owing to Versatility and Cost-Effectiveness

Flexographic printing is the largest segment in the packaging printing market, owing to its versatility and cost-effectiveness. This technology is widely used for printing on a variety of packaging materials, such as plastic films, paper, and corrugated boxes. Flexographic printing’s ability to produce high-quality prints at high speeds makes it particularly attractive for industries with high-volume production requirements, such as food and beverage, consumer goods, and e-commerce packaging. Additionally, flexographic printers are highly adaptable, capable of printing on a wide range of substrates, including flexible packaging materials, which further enhances their appeal in the packaging sector.

The flexibility of flexographic printing allows for the creation of detailed, vibrant designs that meet consumer expectations for aesthetic appeal while also adhering to regulatory requirements. Furthermore, advancements in water-based inks and other eco-friendly solutions have enabled flexographic printing to align with the increasing demand for sustainable packaging. With these innovations, flexographic printing continues to be the dominant printing technology, especially in industries like food and beverage packaging, where cost-effectiveness and high-quality output are critical.

Digital Printing Is Fastest Growing Due to Customization and Short-Run Capability

Digital printing is the fastest-growing segment in the packaging printing market, driven by its ability to offer greater customization and shorter production runs. Unlike traditional printing methods, digital printing allows for on-demand printing, enabling businesses to quickly adapt to market trends, seasonal demands, or specific customer needs. This capability is particularly appealing to industries like cosmetics and pharmaceuticals, where packaging requirements may change frequently, and packaging runs are often smaller. Digital printing also eliminates the need for printing plates, which makes it a more cost-effective option for short-run production and reduces setup times.

As consumer demand for personalized products grows, the ability to create customized packaging with digital printing technology is becoming a key competitive advantage for brands. Additionally, digital printing supports faster turnaround times and lower waste, which aligns with the industry's sustainability goals. With these advantages, digital printing is expected to see continued growth, particularly in niche markets and product categories that require high levels of customization or shorter production runs.

Asia-Pacific Region Is Largest Owing to Expanding Manufacturing Base

The Asia-Pacific region is the largest market for packaging printing, primarily due to the region's expanding manufacturing base and increasing consumer demand. Countries such as China, India, and Japan are leading the market, with a large proportion of packaging printing services being outsourced to meet the needs of various industries, including food and beverage, cosmetics, and pharmaceuticals. Asia-Pacific is home to a significant number of packaging manufacturers that cater to both local and global markets, making it a hub for packaging printing operations.

The region’s rapid urbanization, coupled with a growing middle-class population, has led to a surge in demand for packaged goods, thereby driving the need for high-quality, cost-effective packaging printing solutions. Additionally, with the rise of e-commerce and online retailing in Asia-Pacific, the demand for custom packaging and labeling solutions has increased, further boosting the packaging printing market. The region’s large-scale manufacturing infrastructure, combined with its strong focus on innovation and sustainability, makes it the largest market for packaging printing globally.

Leading Companies and Competitive Landscape

The packaging printing market is competitive, with several prominent companies dominating the landscape. Key players in this market include HP Inc., Quad/Graphics, Mondi Group, Fujifilm Holdings Corporation, and Koenig & Bauer. These companies focus on technological innovations, product development, and sustainability to cater to the growing demand for high-quality and environmentally friendly packaging solutions. Leading players are investing in advanced printing technologies, such as digital and flexographic printing, to offer better performance and meet the evolving needs of their clients across various industries.

The competitive landscape of the packaging printing market is shaped by factors such as technological advancements, cost efficiency, and environmental sustainability. Companies are increasingly adopting digital printing to address the growing trend for customized packaging and shorter print runs. As sustainability becomes a focal point, many players are also investing in eco-friendly ink technologies and energy-efficient equipment. The market remains dynamic, with established companies and new entrants competing to capture market share in a highly fragmented industry.

Recent Developments:

- HP Inc. launched a new digital printing technology aimed at enhancing the efficiency and sustainability of packaging for the food and beverage sector.

- Kodak Printing Solutions introduced a next-generation flexographic printing system for packaging applications, offering improved ink transfer and color accuracy.

- Canon Inc. unveiled an innovative digital printing solution for packaging, focusing on cost-effective, high-quality printing for small businesses.

- Fujifilm Holdings Corporation expanded its gravure printing offerings for the pharmaceutical industry, ensuring high-quality, compliant packaging materials.

- Bobst Group S.A. developed a new hybrid printing technology combining digital and flexographic printing, aimed at improving production efficiency in the packaging sector.

List of Leading Companies:

- HP Inc.

- Xerox Corporation

- Canon Inc.

- Heidelberger Druckmaschinen AG

- Koenig & Bauer AG

- Fujifilm Holdings Corporation

- Ricoh Company, Ltd.

- Bobst Group S.A.

- Kodak Printing Solutions

- Sappi Limited

- UPM-Kymmene Corporation

- Wipf AG

- Windmöller & Hölscher

- Gallus Group

- Manroland Goss

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 23.5 Billion |

|

Forecasted Value (2030) |

USD 35.1 Billion |

|

CAGR (2025 – 2030) |

6.9% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Packaging Printing Market By Printing Technology (Flexographic Printing, Gravure Printing, Offset Printing, Digital Printing, Screen Printing), By Application (Food & Beverage Packaging, Cosmetics Packaging, Pharmaceutical Packaging, Consumer Electronics Packaging), and By End-User Industry (Food & Beverage, Pharmaceuticals, Cosmetics & Personal Care, Electronics) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

HP Inc., Xerox Corporation, Canon Inc., Heidelberger Druckmaschinen AG, Koenig & Bauer AG, Fujifilm Holdings Corporation, Ricoh Company, Ltd., Bobst Group S.A., Kodak Printing Solutions, Sappi Limited, UPM-Kymmene Corporation, Wipf AG, Windmöller & Hölscher, Gallus Group, Manroland Goss |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Packaging Printing Market, by Printing Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Flexographic Printing |

|

4.2. Gravure Printing |

|

4.3. Offset Printing |

|

4.4. Digital Printing |

|

4.5. Screen Printing |

|

5. Packaging Printing Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Food & Beverage Packaging |

|

5.2. Cosmetics Packaging |

|

5.3. Pharmaceutical Packaging |

|

5.4. Consumer Electronics Packaging |

|

5.5. Others |

|

6. Packaging Printing Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Food & Beverage |

|

6.2. Pharmaceuticals |

|

6.3. Cosmetics & Personal Care |

|

6.4. Electronics |

|

6.5. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Packaging Printing Market, by Printing Technology |

|

7.2.7. North America Packaging Printing Market, by Application |

|

7.2.8. North America Packaging Printing Market, by End-User Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Packaging Printing Market, by Printing Technology |

|

7.2.9.1.2. US Packaging Printing Market, by Application |

|

7.2.9.1.3. US Packaging Printing Market, by End-User Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. HP Inc. |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Xerox Corporation |

|

9.3. Canon Inc. |

|

9.4. Heidelberger Druckmaschinen AG |

|

9.5. Koenig & Bauer AG |

|

9.6. Fujifilm Holdings Corporation |

|

9.7. Ricoh Company, Ltd. |

|

9.8. Bobst Group S.A. |

|

9.9. Kodak Printing Solutions |

|

9.10. Sappi Limited |

|

9.11. UPM-Kymmene Corporation |

|

9.12. Wipf AG |

|

9.13. Windmöller & Hölscher |

|

9.14. Gallus Group |

|

9.15. Manroland Goss |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Packaging Printing Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Packaging Printing Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Packaging Printing Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA