As per Intent Market Research, the Packaging Automation Market was valued at USD 24.5 Billion in 2024-e and will surpass USD 38.3 Billion by 2030; growing at a CAGR of 7.7% during 2025-2030.

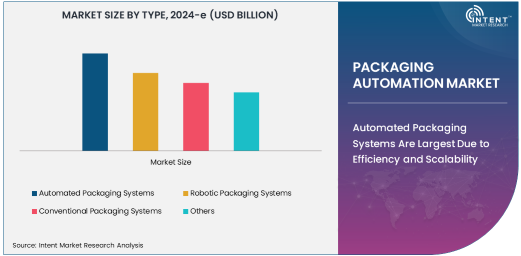

Automated Packaging Systems Are Largest Due to Efficiency and Scalability

The packaging automation market is expanding rapidly as businesses across industries seek to improve efficiency, reduce operational costs, and enhance product consistency. Among the various types of packaging automation systems, automated packaging systems are the largest due to their ability to streamline the entire packaging process. These systems include machines that handle various tasks such as filling, sealing, labeling, and wrapping, all with minimal human intervention. Their widespread adoption is largely driven by their ability to increase production rates, reduce errors, and optimize resources in manufacturing processes.

Automated packaging systems also offer scalability, allowing businesses to easily adjust their production capacity based on demand fluctuations. The increasing focus on improving operational efficiency, particularly in industries like food and beverage, pharmaceuticals, and consumer goods, is further propelling the growth of automated packaging systems. As companies continue to look for ways to enhance productivity and maintain high levels of quality control, the demand for automated packaging solutions is expected to continue to grow, making it the largest segment within the packaging automation market.

Robotic Packaging Systems Are Fastest Growing Due to Flexibility and Advanced Capabilities

Robotic packaging systems represent the fastest growing segment in the packaging automation market, driven by their flexibility and advanced capabilities. These systems are increasingly being deployed to handle tasks such as product handling, sorting, and packaging, all while ensuring precise, high-speed operations. Robotic systems can adapt to different packaging formats and sizes, making them particularly valuable in industries where product diversity and variability are high, such as food and beverage, consumer goods, and electronics.

One of the primary advantages of robotic packaging systems is their ability to work collaboratively with human operators in collaborative robots (cobots) environments, which increases both productivity and worker safety. Moreover, advances in artificial intelligence (AI) and machine learning are enabling robots to perform more complex tasks with greater accuracy and efficiency, further accelerating their adoption. As industries continue to prioritize automation for improved flexibility, scalability, and cost efficiency, robotic packaging systems are set to remain the fastest growing segment within the packaging automation market.

Food & Beverage End-User Industry Is Largest Due to High Demand for Packaging Efficiency

The food and beverage industry is the largest end-user of packaging automation systems, accounting for a significant portion of the market share. This industry’s need for fast, reliable, and consistent packaging solutions has driven the widespread adoption of automated packaging systems. These systems ensure that food products are packaged quickly, efficiently, and in compliance with safety regulations, while also maintaining high levels of quality control. With rising consumer demand for convenience, there is a growing focus on packaging that preserves the freshness and quality of food products.

In addition to operational efficiency, packaging automation in the food and beverage sector helps meet the growing demand for personalized and sustainable packaging solutions. Automation enables companies to improve production speeds and lower costs, which is crucial in this highly competitive market. As consumer trends continue to push for faster delivery times and better product presentation, the food and beverage industry will continue to lead the way in adopting packaging automation technologies.

Asia-Pacific Is Fastest Growing Region Due to Industrial Expansion and Cost Efficiency Demands

The Asia-Pacific region is the fastest growing in the packaging automation market, driven by rapid industrial expansion and the increasing demand for cost-effective production solutions. As manufacturing industries in countries like China, India, and Japan continue to scale, the need for automated packaging solutions to improve efficiency and productivity has grown significantly. Automation systems, including robotic and automated packaging systems, are increasingly seen as key enablers of growth in this region.

The region's fast adoption of automation technologies is also being driven by labor shortages, rising labor costs, and a strong push for enhanced production speeds. Furthermore, as the food and beverage, pharmaceutical, and consumer goods sectors continue to expand in Asia-Pacific, the demand for high-speed, high-quality packaging solutions grows. These factors combined position the Asia-Pacific region as the fastest growing market for packaging automation.

Leading Companies and Competitive Landscape

The packaging automation market is highly competitive, with key players such as KUKA AG, ABB Ltd., FANUC Corporation, and Mitsubishi Electric Corporation dominating the landscape. These companies are focused on developing advanced robotic and automated systems that meet the growing demand for efficiency, flexibility, and cost-effectiveness in packaging operations.

Competition in this market is driven by technological innovation, with companies continuously investing in research and development to enhance the capabilities of their packaging automation systems. Strategic partnerships, acquisitions, and expanding service offerings are common strategies employed by market leaders to strengthen their position. Additionally, as industries place a greater emphasis on sustainability, packaging automation companies are focusing on providing solutions that not only optimize packaging processes but also reduce environmental impact. As the demand for packaging automation continues to rise, these leading players are well-positioned to capture a significant share of the growing market.

Recent Developments:

- ABB Ltd. launched a new robotic packaging system designed to improve efficiency in packaging lines across industries such as food and pharmaceuticals.

- Siemens AG introduced an advanced automated packaging solution that integrates artificial intelligence to optimize packaging processes in the automotive sector.

- FANUC Corporation unveiled a high-speed robotic packaging system aimed at enhancing packaging performance and reducing product damage in the consumer goods market.

- Schneider Electric developed a new range of packaging automation technologies that reduce energy consumption and improve the sustainability of packaging lines.

- Tetra Pak International S.A. expanded its automated packaging solutions with a focus on improving sustainability and reducing material waste in the food and beverage industry.

List of Leading Companies:

- ABB Ltd.

- Rockwell Automation, Inc.

- Siemens AG

- Krones AG

- FANUC Corporation

- Mitsubishi Electric Corporation

- Schneider Electric

- Bosch Packaging Technology

- Sidel Group

- Comau S.p.A.

- Beckhoff Automation

- Tetra Pak International S.A.

- Mettler Toledo

- OMRON Corporation

- ProMach, Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 24.5 Billion |

|

Forecasted Value (2030) |

USD 38.3 Billion |

|

CAGR (2025 – 2030) |

7.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Packaging Automation Market By Type (Automated Packaging Systems, Robotic Packaging Systems, Conventional Packaging Systems), By Application (Filling, Sealing, Labeling, Wrapping), and By End-User Industry (Food & Beverage, Pharmaceutical, Consumer Goods, Electronics, Automotive) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

ABB Ltd., Rockwell Automation, Inc., Siemens AG, Krones AG, FANUC Corporation, Mitsubishi Electric Corporation, Schneider Electric, Bosch Packaging Technology, Sidel Group, Comau S.p.A., Beckhoff Automation, Tetra Pak International S.A., Mettler Toledo, OMRON Corporation, ProMach, Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Packaging Automation Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Automated Packaging Systems |

|

4.2. Robotic Packaging Systems |

|

4.3. Conventional Packaging Systems |

|

4.4. Others |

|

5. Packaging Automation Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Filling |

|

5.2. Sealing |

|

5.3. Labeling |

|

5.4. Wrapping |

|

5.5. Others |

|

6. Packaging Automation Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Food & Beverage |

|

6.2. Pharmaceutical |

|

6.3. Consumer Goods |

|

6.4. Electronics |

|

6.5. Automotive |

|

6.6. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Packaging Automation Market, by Type |

|

7.2.7. North America Packaging Automation Market, by Application |

|

7.2.8. North America Packaging Automation Market, by End-User Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Packaging Automation Market, by Type |

|

7.2.9.1.2. US Packaging Automation Market, by Application |

|

7.2.9.1.3. US Packaging Automation Market, by End-User Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. ABB Ltd. |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Rockwell Automation, Inc. |

|

9.3. Siemens AG |

|

9.4. Krones AG |

|

9.5. FANUC Corporation |

|

9.6. Mitsubishi Electric Corporation |

|

9.7. Schneider Electric |

|

9.8. Bosch Packaging Technology |

|

9.9. Sidel Group |

|

9.10. Comau S.p.A. |

|

9.11. Beckhoff Automation |

|

9.12. Tetra Pak International S.A. |

|

9.13. Mettler Toledo |

|

9.14. OMRON Corporation |

|

9.15. ProMach, Inc. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Packaging Automation Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Packaging Automation Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Packaging Automation Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA