As per Intent Market Research, the Overhead Console Market was valued at USD 4.5 Billion in 2024-e and will surpass USD 7.7 Billion by 2030; growing at a CAGR of 9.3% during 2025-2030.

The overhead console market is poised for steady growth, driven by the increasing demand for advanced automotive features that enhance driver and passenger convenience. Overhead consoles, typically located on the ceiling of a vehicle, house a range of functions including lighting, climate controls, and storage compartments, as well as sensors for various in-vehicle technologies. The market is evolving with new technological integrations such as smart features, wireless charging, and ambient lighting. With automakers focusing on enhancing the in-cabin experience, overhead consoles are becoming an essential element in both traditional and electric vehicles, offering consumers increased functionality and comfort.

As the automotive industry continues to evolve, particularly with the rise of electric vehicles (EVs) and a focus on integrating more advanced technologies into vehicles, the overhead console market is expected to witness significant growth. Automotive OEMs and aftermarket players are actively exploring new designs and materials to meet consumer demand for innovation. In addition, the growing trend of personalizing vehicle interiors, particularly among high-end consumers, is expected to push the market further toward more sophisticated and feature-rich overhead console solutions.

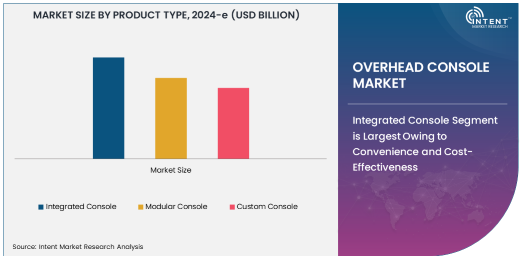

Integrated Console Segment is Largest Owing to Convenience and Cost-Effectiveness

The integrated console segment holds the largest share in the overhead console market, driven by its ability to combine multiple functions into a single, cohesive unit. Integrated consoles offer a convenient and cost-effective solution for automakers looking to maximize vehicle space and streamline design while offering essential features like lighting, climate controls, and storage. These consoles are typically easier to install and maintain due to their simpler design, making them a popular choice for both passenger and commercial vehicles.

Automakers prefer integrated consoles as they help reduce complexity, enhance the vehicle's overall aesthetic, and provide a seamless user experience. The cost-effectiveness of this design also makes it a preferred choice for mass-market vehicles. With the demand for functional and space-efficient interiors, integrated consoles are likely to remain dominant in the market, particularly in vehicles where affordability and practicality are top priorities. As manufacturers continue to innovate and enhance these consoles with integrated technologies such as smart displays and voice control, the demand for integrated consoles is expected to further increase.

Electric Vehicles Segment is Fastest Growing Owing to Technological Advancements and Increasing EV Adoption

The electric vehicles (EVs) segment is the fastest-growing within the overhead console market, driven by the rapid adoption of electric cars and advancements in EV-specific technology. Overhead consoles in EVs are becoming increasingly sophisticated, offering advanced features like touchscreens, integrated climate control systems, and wireless charging pads. These features are in line with the evolving consumer preference for high-tech and eco-friendly vehicles, making EVs an attractive choice for environmentally conscious buyers who also seek modern in-car technologies.

As electric vehicles continue to penetrate the automotive market, the demand for overhead consoles with integrated features is expected to grow. EV manufacturers are integrating these consoles to not only improve comfort but also to maximize energy efficiency by incorporating features such as energy-saving lighting and controls. The continued shift towards electric mobility, driven by government regulations and incentives, is likely to boost the demand for advanced overhead consoles, making this segment the fastest growing in the market.

Plastic Material Segment Dominates Due to Lightweight and Cost-Effective Benefits

The plastic material segment dominates the overhead console market due to its lightweight nature, cost-effectiveness, and ease of molding into complex shapes. Plastic consoles offer a combination of durability, flexibility, and affordability, which makes them a preferred choice for both automotive OEMs and aftermarket suppliers. These advantages have made plastic the material of choice for overhead consoles, particularly in mass-market vehicles where affordability is key.

In addition to its low cost, plastic is versatile and can be easily customized in terms of color, texture, and design, making it a popular choice among manufacturers looking to create attractive and functional interiors. The lightweight nature of plastic also contributes to improved fuel efficiency, which is increasingly important in the automotive industry. With advancements in materials science, manufacturers are incorporating more durable and sustainable types of plastics, further cementing plastic as the dominant material in the overhead console market.

Automotive OEMs Segment is Largest End-User Due to OEM Demand for Advanced Features

The automotive OEMs segment is the largest end-user in the overhead console market, driven by the demand for innovative and feature-rich overhead consoles in new vehicle models. Original Equipment Manufacturers (OEMs) are increasingly focusing on providing enhanced in-cabin experiences, and overhead consoles are a key component in achieving this goal. These consoles are designed to offer consumers easy access to essential features like climate control, lighting, and storage, making them an integral part of modern vehicles.

OEMs are investing in the development of overhead consoles with advanced features, such as touch-sensitive controls, integrated communication systems, and ambient lighting, in response to growing consumer expectations for enhanced vehicle interiors. The rising preference for electric and hybrid vehicles has further amplified the demand for sophisticated overhead consoles that integrate with the vehicle’s energy-efficient systems. As automotive OEMs continue to prioritize innovation and consumer comfort, this segment is expected to remain the dominant end-user in the overhead console market.

Asia Pacific is Fastest Growing Region Owing to Increasing Automotive Production and EV Adoption

The Asia Pacific region is the fastest-growing in the overhead console market, driven by the region's rapidly expanding automotive industry, increased vehicle production, and rising adoption of electric vehicles (EVs). Countries like China, Japan, South Korea, and India are leading the charge in terms of both traditional vehicle manufacturing and the production of electric vehicles. The growing emphasis on advanced automotive technologies and in-car features in the region has created strong demand for overhead consoles, particularly those with integrated technology and energy-efficient features.

In addition, Asia Pacific is home to several automotive OEMs and suppliers, which contributes to the region's growth in the overhead console market. The region's strong manufacturing capabilities and growing middle-class population also play a significant role in increasing vehicle demand, further boosting the need for overhead consoles. As consumer preferences evolve toward high-tech and eco-friendly vehicles, the Asia Pacific region is expected to continue leading in terms of growth in the overhead console market.

Competitive Landscape and Key Players

The overhead console market is competitive, with several key players focusing on technological innovation and design to meet the growing demand for advanced automotive features. Leading companies in the market include Lear Corporation, Faurecia, Continental AG, and Valeo, which are known for their expertise in automotive interiors and advanced electronic systems. These companies are continuously developing new products, such as modular consoles, customized designs, and integrated smart features to enhance the driving experience.

The competitive landscape is also shaped by partnerships between automotive OEMs and console suppliers, aimed at co-developing advanced features and meeting the evolving demands of consumers. Additionally, as the market continues to grow, companies are focusing on expanding their product portfolios to include more sustainable materials, such as bio-based plastics, in response to the increasing demand for eco-friendly solutions. As technology continues to advance, players in the overhead console market must adapt to the changing needs of both automakers and consumers to remain competitive.

Recent Developments:

- Continental AG launched a new modular overhead console design that improves the integration of infotainment and lighting systems.

- Valeo SA introduced a new lightweight overhead console for electric vehicles to reduce vehicle weight and improve energy efficiency.

- Denso Corporation expanded its overhead console portfolio to include advanced features like gesture control for automotive applications.

- Magna International announced the development of a smart overhead console with built-in sensors to monitor passenger activity.

- Aptiv PLC unveiled a customizable overhead console with enhanced connectivity features for next-generation vehicles.

List of Leading Companies:

- Continental AG

- Valeo SA

- Denso Corporation

- Faurecia

- ZF Friedrichshafen AG

- Magna International

- Lear Corporation

- Johnson Controls International

- Aptiv PLC

- Panasonic Corporation

- Delphi Technologies

- Visteon Corporation

- BorgWarner

- Hyundai Mobis

- Yanfeng Automotive Interiors

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 4.5 Billion |

|

Forecasted Value (2030) |

USD 7.7 Billion |

|

CAGR (2025 – 2030) |

9.3% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Overhead Console Market By Product Type (Integrated Console, Modular Console, Custom Console), By Material (Plastic, Metal), By Application (Passenger Vehicles, Commercial Vehicles, Electric Vehicles), and By End-Use Industry (Automotive OEMs, Aftermarket) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Continental AG, Valeo SA, Denso Corporation, Faurecia, ZF Friedrichshafen AG, Magna International, Lear Corporation, Johnson Controls International, Aptiv PLC, Panasonic Corporation, Delphi Technologies, Visteon Corporation, BorgWarner, Hyundai Mobis, Yanfeng Automotive Interiors |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Overhead Console Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Integrated Console |

|

4.2. Modular Console |

|

4.3. Custom Console |

|

5. Overhead Console Market, by Material (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Plastic |

|

5.2. Metal |

|

5.3. Others |

|

6. Overhead Console Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Passenger Vehicles |

|

6.2. Commercial Vehicles |

|

6.3. Electric Vehicles |

|

6.4. Others |

|

7. Overhead Console Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Automotive OEMs |

|

7.2. Aftermarket |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Overhead Console Market, by Product Type |

|

8.2.7. North America Overhead Console Market, by Material |

|

8.2.8. North America Overhead Console Market, by Application |

|

8.2.9. North America Overhead Console Market, by End-Use Industry |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Overhead Console Market, by Product Type |

|

8.2.10.1.2. US Overhead Console Market, by Material |

|

8.2.10.1.3. US Overhead Console Market, by Application |

|

8.2.10.1.4. US Overhead Console Market, by End-Use Industry |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Continental AG |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Valeo SA |

|

10.3. Denso Corporation |

|

10.4. Faurecia |

|

10.5. ZF Friedrichshafen AG |

|

10.6. Magna International |

|

10.7. Lear Corporation |

|

10.8. Johnson Controls International |

|

10.9. Aptiv PLC |

|

10.10. Panasonic Corporation |

|

10.11. Delphi Technologies |

|

10.12. Visteon Corporation |

|

10.13. BorgWarner |

|

10.14. Hyundai Mobis |

|

10.15. Yanfeng Automotive Interiors |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Overhead Console Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Overhead Console Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Overhead Console Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA