As per Intent Market Research, the Overhead Conductor Market was valued at USD 9.5 Billion in 2024-e and will surpass USD 15.3 Billion by 2030; growing at a CAGR of 8.2% during 2025-2030.

The overhead conductor market is a key component of the power transmission and distribution industry, as it ensures the reliable transfer of electrical power across vast distances. Overhead conductors are crucial for transmitting electricity from power plants to substations and ultimately to end-users. With increasing demand for energy across the globe, there is a growing need for efficient, durable, and cost-effective conductors. These conductors are vital in both urban and rural power grids, as they provide an efficient means of carrying high-voltage power with minimal loss over long distances. Technological advancements in conductor materials and construction have enhanced performance, making overhead conductors an essential part of modern power infrastructure.

The demand for high-quality and efficient conductors is further driven by the need to upgrade and expand existing power grids to accommodate growing energy consumption and the integration of renewable energy sources. The global push for smart grids, renewable energy integration, and energy efficiency has led to a rising interest in advanced conductor technologies. As these factors continue to shape the market, the overhead conductor market is poised for growth, with emerging regions investing heavily in infrastructure development and energy sustainability.

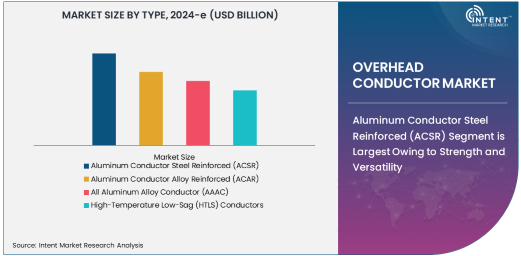

Aluminum Conductor Steel Reinforced (ACSR) Segment is Largest Owing to Strength and Versatility

The Aluminum Conductor Steel Reinforced (ACSR) segment is the largest in the overhead conductor market, owing to its strength, versatility, and cost-effectiveness. ACSR conductors are widely used for power transmission over long distances due to their ability to handle high tensile strength and their relatively lightweight construction. The conductor’s design, which combines aluminum for electrical conductivity and steel for mechanical strength, provides an optimal balance of conductivity and durability, making it ideal for harsh environmental conditions.

ACSR conductors are commonly deployed in long-range power transmission systems, especially in regions with difficult terrain, where their ability to withstand mechanical stresses is crucial. Their cost-effectiveness and ease of installation have made them the preferred choice for utilities and energy companies worldwide. As a result, the ACSR segment continues to dominate the overhead conductor market, supported by their reliable performance in both transmission and distribution networks.

Power Transmission is Largest Application Segment Due to Expanding Energy Needs

The power transmission application segment is the largest in the overhead conductor market, driven by the increasing demand for energy worldwide. As global energy consumption rises, there is a growing need for efficient power transmission systems that can deliver electricity from power plants to distant locations. Overhead conductors are a key component of these systems, as they offer a practical and reliable means of transporting high-voltage electricity over long distances with minimal loss.

Power transmission networks are being expanded and modernized in many parts of the world, particularly in emerging economies where rapid urbanization and industrialization are driving electricity demand. The transition to renewable energy sources such as wind and solar is also contributing to the expansion of power transmission networks, as electricity from these sources often needs to be transmitted over long distances to reach consumers. As a result, the power transmission application continues to be the largest and most critical segment within the overhead conductor market.

Utilities Are Largest End-User Industry Due to Widespread Demand for Grid Expansion

The utilities industry is the largest end-user segment for overhead conductors, as the global push for grid modernization and expansion is driving substantial demand for new conductor systems. Utilities are responsible for ensuring the safe and efficient transmission and distribution of electricity, which involves maintaining and upgrading existing infrastructure while also expanding capacity to meet rising demand. Overhead conductors are a fundamental part of this infrastructure, and utilities rely on them to ensure uninterrupted power supply, especially in areas with growing populations and industrial development.

As the need for reliable and sustainable power increases, utilities are investing heavily in modernizing their grids to accommodate new energy sources and meet environmental goals. The expansion of smart grids, which incorporate advanced technologies to monitor and manage electricity distribution, is further driving the demand for overhead conductors. The utilities sector is expected to continue to be the dominant end-user industry in the overhead conductor market, as governments and companies invest in improving energy infrastructure and expanding grid networks.

Asia-Pacific is Fastest Growing Region Due to Infrastructure Development and Urbanization

The Asia-Pacific (APAC) region is the fastest-growing market for overhead conductors, driven by rapid infrastructure development and urbanization. Countries like China, India, and Southeast Asian nations are investing heavily in expanding and modernizing their power grids to accommodate increasing energy demand due to population growth, industrialization, and urbanization. The adoption of renewable energy sources is also a key factor in the expansion of power transmission networks in the region, further fueling the demand for high-performance overhead conductors.

In addition to grid expansion, the APAC region is experiencing a rise in smart grid adoption and the modernization of energy infrastructure, which includes the use of advanced conductors such as HTLS. As these countries continue to urbanize and develop their energy sectors, the demand for overhead conductors is expected to increase, making the APAC region the fastest-growing market globally. The region’s emphasis on energy efficiency and sustainability will also contribute to the growing adoption of advanced conductor technologies.

Leading Companies and Competitive Landscape

The overhead conductor market is highly competitive, with key players focusing on innovation, product development, and strategic partnerships to gain market share. Leading companies in the market include Prysmian Group, Nexans, Southwire Company, General Cable, and Sumitomo Electric. These companies offer a broad range of conductor solutions for power transmission and distribution, including ACSR, HTLS, and other advanced conductor technologies.

The competitive landscape is characterized by technological advancements, with companies focusing on developing high-performance materials that can withstand extreme conditions and enhance energy efficiency. Additionally, players are expanding their product portfolios to cater to the growing demand for renewable energy integration and smart grid technologies. As the market continues to evolve, companies are also focusing on expanding their geographic presence, particularly in emerging markets where the demand for grid infrastructure is rising rapidly.

Recent Developments:

- In December 2024, Prysmian Group launched an advanced HTLS conductor for high-efficiency power transmission.

- In November 2024, Southwire Company, LLC secured a contract to supply overhead conductors for a major transmission project in North America.

- In October 2024, Sterlite Power introduced a new line of ACSR conductors for enhanced grid stability.

- In September 2024, General Cable Corporation expanded its production capacity for AAAC conductors to meet growing demand.

- In August 2024, Nexans S.A. completed a significant installation of overhead power lines in Asia-Pacific for an urban infrastructure project.

List of Leading Companies:

- Southwire Company, LLC

- General Cable Corporation

- Nexans S.A.

- Sterlite Power

- Prysmian Group

- LS Cable & System Ltd.

- Sumitomo Electric Industries, Ltd.

- The Furukawa Electric Co., Ltd.

- Midal Cables Ltd.

- KEI Industries Limited

- Taihan Electric Wire Co., Ltd.

- J-Power Systems Corporation

- ZTT International Limited

- Hangzhou Cable Co., Ltd.

- Fujikura Ltd.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 9.5 Billion |

|

Forecasted Value (2030) |

USD 15.3 Billion |

|

CAGR (2025 – 2030) |

8.2% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Overhead Conductor Market by Type (Aluminum Conductor Steel Reinforced (ACSR), Aluminum Conductor Alloy Reinforced (ACAR), All Aluminum Alloy Conductor (AAAC), High-Temperature Low-Sag (HTLS) Conductors), Application (Power Transmission, Power Distribution), End-User Industry (Utilities, Industrial Applications, Residential Applications) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Southwire Company, LLC, General Cable Corporation, Nexans S.A., Sterlite Power, Prysmian Group, LS Cable & System Ltd., Sumitomo Electric Industries, Ltd., The Furukawa Electric Co., Ltd., Midal Cables Ltd., KEI Industries Limited, Taihan Electric Wire Co., Ltd., J-Power Systems Corporation, ZTT International Limited, Hangzhou Cable Co., Ltd., Fujikura Ltd. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Overhead Conductor Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Aluminum Conductor Steel Reinforced (ACSR) |

|

4.2. Aluminum Conductor Alloy Reinforced (ACAR) |

|

4.3. All Aluminum Alloy Conductor (AAAC) |

|

4.4. High-Temperature Low-Sag (HTLS) Conductors |

|

5. Overhead Conductor Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Power Transmission |

|

5.2. Power Distribution |

|

6. Overhead Conductor Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Utilities |

|

6.2. Industrial Applications |

|

6.3. Residential Applications |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Overhead Conductor Market, by Type |

|

7.2.7. North America Overhead Conductor Market, by Application |

|

7.2.8. North America Overhead Conductor Market, by End-User Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Overhead Conductor Market, by Type |

|

7.2.9.1.2. US Overhead Conductor Market, by Application |

|

7.2.9.1.3. US Overhead Conductor Market, by End-User Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Southwire Company, LLC |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. General Cable Corporation |

|

9.3. Nexans S.A. |

|

9.4. Sterlite Power |

|

9.5. Prysmian Group |

|

9.6. LS Cable & System Ltd. |

|

9.7. Sumitomo Electric Industries, Ltd. |

|

9.8. The Furukawa Electric Co., Ltd. |

|

9.9. Midal Cables Ltd. |

|

9.10. KEI Industries Limited |

|

9.11. Taihan Electric Wire Co., Ltd. |

|

9.12. J-Power Systems Corporation |

|

9.13. ZTT International Limited |

|

9.14. Hangzhou Cable Co., Ltd. |

|

9.15. Fujikura Ltd. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Overhead Conductor Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Overhead Conductor Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Overhead Conductor Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA