As per Intent Market Research, the Osteonecrosis Treatment Market was valued at USD 267.2 billion in 2024-e and will surpass USD 398.5 billion by 2030; growing at a CAGR of 6.9% during 2025 - 2030.

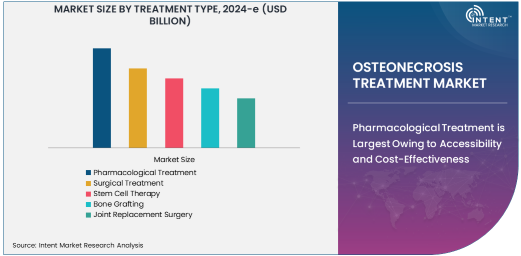

The osteonecrosis treatment market has witnessed significant advancements, particularly in the treatment options available for the condition. Among the various treatment types, pharmacological treatment is the largest sub-segment. Pharmacological interventions are often the first line of treatment for osteonecrosis patients, primarily due to their accessibility, affordability, and effectiveness in managing early-stage symptoms. These treatments typically involve the use of non-steroidal anti-inflammatory drugs (NSAIDs), bisphosphonates, and anticoagulants to manage pain, inflammation, and slow disease progression. The ability to manage the symptoms of osteonecrosis without invasive procedures makes pharmacological treatment a preferred option for many patients.

Pharmacological Treatment is Largest Owing to Accessibility and Cost-Effectiveness

The osteonecrosis treatment market has witnessed significant advancements, particularly in the treatment options available for the condition. Among the various treatment types, pharmacological treatment is the largest sub-segment. Pharmacological interventions are often the first line of treatment for osteonecrosis patients, primarily due to their accessibility, affordability, and effectiveness in managing early-stage symptoms. These treatments typically involve the use of non-steroidal anti-inflammatory drugs (NSAIDs), bisphosphonates, and anticoagulants to manage pain, inflammation, and slow disease progression. The ability to manage the symptoms of osteonecrosis without invasive procedures makes pharmacological treatment a preferred option for many patients.

The demand for pharmacological treatment is particularly notable in regions with a high volume of early-stage osteonecrosis cases, where it serves as an effective means of controlling the disease before more invasive options are required. This treatment type’s role in providing immediate relief and its relatively low cost compared to surgical procedures are key factors contributing to its prominence. As a result, pharmacological treatment remains a foundational part of osteonecrosis management, especially in settings where access to advanced surgical options may be limited.

Femoral Head Osteonecrosis is Largest Due to Prevalence and Impact

Femoral head osteonecrosis (FHO) is the largest sub-segment within the osteonecrosis disease category, driven by its higher prevalence and the severity of its impact. FHO typically occurs when the blood supply to the femoral head is disrupted, leading to bone death and joint collapse. This form of osteonecrosis is most commonly associated with hip joint issues and is often linked to risk factors such as alcohol consumption, corticosteroid use, and trauma. The severity of FHO and its ability to rapidly progress if untreated have made it a focus of research and treatment development, leading to a larger market share.

The treatment of femoral head osteonecrosis often requires surgical intervention, including joint replacement or core decompression, contributing to the dominance of this disease type in the market. The increasing number of hip joint disorders and the aging population, particularly in developed regions, are further driving the demand for effective treatments for femoral head osteonecrosis. As the condition is often diagnosed at a late stage, the need for more advanced therapies, including joint replacement, continues to grow, solidifying femoral head osteonecrosis as the largest sub-segment in this market.

Hospitals Hold the Largest Share Due to Comprehensive Treatment Needs

In the osteonecrosis treatment market, hospitals represent the largest sub-segment among end-users. Hospitals are equipped with the necessary infrastructure, advanced diagnostic tools, and specialized teams to handle severe cases of osteonecrosis, particularly those requiring surgical intervention or complex pharmacological treatment regimens. Given the need for emergency care and the management of advanced disease stages, hospitals are the primary setting for patients with osteonecrosis to receive treatment. Furthermore, the wide range of treatment options available, including joint replacements, stem cell therapy, and other advanced surgical procedures, further contributes to the dominance of hospitals in this segment.

The ability of hospitals to provide comprehensive care for osteonecrosis patients, including diagnostics, surgeries, and post-operative rehabilitation, makes them the preferred choice for patients with moderate to severe osteonecrosis. Hospitals also benefit from the steady demand for specialized orthopedic surgeons and rehabilitation professionals, ensuring that they remain at the forefront of osteonecrosis treatment. As the condition often requires multi-disciplinary care, hospitals continue to attract a large portion of the treatment market.

North America is the Largest Region Due to Advanced Healthcare Infrastructure and High Prevalence

North America holds the largest market share in the osteonecrosis treatment market, driven by its advanced healthcare infrastructure, high prevalence of risk factors, and significant awareness of the disease. The region’s healthcare system, characterized by cutting-edge medical technologies and a high standard of care, ensures that treatments for osteonecrosis are readily available and accessible. In addition, the aging population in North America, combined with lifestyle factors such as high alcohol consumption and corticosteroid use, has led to an increase in the number of osteonecrosis cases, further amplifying the demand for treatment options.

The presence of well-established hospitals, orthopedic clinics, and specialized healthcare providers in North America contributes significantly to the region’s market dominance. With ongoing investments in healthcare, as well as favorable reimbursement policies for advanced treatments like joint replacement surgery and stem cell therapy, North America remains the largest and most lucrative market for osteonecrosis treatments globally. This position is expected to maintain its lead as the region continues to focus on improving the quality of healthcare and addressing the growing burden of musculoskeletal disorders.

Competitive Landscape: Leading Companies and Market Dynamics

The osteonecrosis treatment market is highly competitive, with several key players dominating the landscape. Companies such as Zimmer Biomet, Stryker Corporation, and DePuy Synthes (Johnson & Johnson) are among the leaders, focusing on expanding their portfolios with innovative solutions for osteonecrosis treatment. These companies leverage their strong R&D capabilities to introduce new products, such as advanced bone grafting materials and minimally invasive surgical tools, which are driving market growth. Additionally, Medtronic and Smith & Nephew are also prominent players, with a focus on enhancing their offerings through acquisitions, partnerships, and collaborations with medical institutions.

The competitive landscape is characterized by ongoing product development, with leading companies investing in cutting-edge technologies like stem cell therapy and regenerative medicine to address the complex needs of osteonecrosis patients. The market dynamics are influenced by the increasing demand for minimally invasive treatments, improved surgical outcomes, and enhanced post-operative care. As patient outcomes become the central focus, competition is intensifying among companies that can offer not only effective treatments but also comprehensive care packages that include rehabilitation and long-term management solutions. The landscape is also shaped by regulatory developments, as companies must navigate complex approval processes to introduce new therapies and surgical devices.

Recent Developments:

- Zimmer Biomet announced a partnership with a regenerative medicine company to develop new treatments for osteonecrosis using stem cell technology in December 2024.

- Medtronic launched a new minimally invasive device for joint replacement surgery aimed at improving recovery times for osteonecrosis patients in November 2024.

- Stryker Corporation completed the acquisition of a leading orthopedic biomaterial company to enhance their osteonecrosis treatment portfolio in October 2024.

- DePuy Synthes (Johnson & Johnson) received FDA approval for a new bone grafting material to treat femoral head osteonecrosis in September 2024.

- Orthofix International N.V. introduced a new biologic product designed to promote bone regeneration in osteonecrosis patients in August 2024.

List of Leading Companies:

- Zimmer Biomet

- Stryker Corporation

- DePuy Synthes (Johnson & Johnson)

- Medtronic

- Smith & Nephew

- Harman Medical

- Medi-Tech International

- Orthofix International N.V.

- Bioventus

- Arthrex Inc.

- NuVasive

- B. Braun Melsungen AG

- Wright Medical Group N.V.

- Conmed Corporation

- Integra LifeSciences

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 267.2 Billion |

|

Forecasted Value (2030) |

USD 398.5 Billion |

|

CAGR (2025 – 2030) |

6.9% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Osteonecrosis Treatment Market By Treatment Type (Pharmacological Treatment, Surgical Treatment, Stem Cell Therapy, Bone Grafting, Joint Replacement Surgery), By Disease Type (Femoral Head Osteonecrosis, Knee Osteonecrosis, Shoulder Osteonecrosis, Ankle Osteonecrosis, Elbow Osteonecrosis), By End-User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Rehabilitation Centers) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Zimmer Biomet, Stryker Corporation, DePuy Synthes (Johnson & Johnson), Medtronic, Smith & Nephew, Harman Medical, Medi-Tech International, Orthofix International N.V., Bioventus, Arthrex Inc., NuVasive, B. Braun Melsungen AG, Wright Medical Group N.V., Conmed Corporation, Integra LifeSciences |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Osteonecrosis Treatment Market, by Treatment Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Pharmacological Treatment |

|

4.2. Surgical Treatment |

|

4.3. Stem Cell Therapy |

|

4.4. Bone Grafting |

|

4.5. Joint Replacement Surgery |

|

5. Osteonecrosis Treatment Market, by Disease Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Femoral Head Osteonecrosis |

|

5.2. Knee Osteonecrosis |

|

5.3. Shoulder Osteonecrosis |

|

5.4. Ankle Osteonecrosis |

|

5.5. Elbow Osteonecrosis |

|

6. Osteonecrosis Treatment Market, by End-User (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Hospitals |

|

6.2. Orthopedic Clinics |

|

6.3. Ambulatory Surgical Centers |

|

6.4. Rehabilitation Centers |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Osteonecrosis Treatment Market, by Treatment Type |

|

7.2.7. North America Osteonecrosis Treatment Market, by Disease Type |

|

7.2.8. North America Osteonecrosis Treatment Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Osteonecrosis Treatment Market, by Treatment Type |

|

7.2.9.1.2. US Osteonecrosis Treatment Market, by Disease Type |

|

7.2.9.1.3. US Osteonecrosis Treatment Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Zimmer Biomet |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Stryker Corporation |

|

9.3. DePuy Synthes (Johnson & Johnson) |

|

9.4. Medtronic |

|

9.5. Smith & Nephew |

|

9.6. Harman Medical |

|

9.7. Medi-Tech International |

|

9.8. Orthofix International N.V. |

|

9.9. Bioventus |

|

9.10. Arthrex Inc. |

|

9.11. NuVasive |

|

9.12. B. Braun Melsungen AG |

|

9.13. Wright Medical Group N.V. |

|

9.14. Conmed Corporation |

|

9.15. Integra LifeSciences |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Osteonecrosis Treatment Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Osteonecrosis Treatment Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Osteonecrosis Treatment Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA