As per Intent Market Research, the OSS and BSS Market was valued at USD 32.4 Billion in 2024-e and will surpass USD 56.7 Billion by 2030; growing at a CAGR of 8.3% during 2025-2030.

The OSS (Operations Support Systems) and BSS (Business Support Systems) market is a critical component of the telecom and IT industries, as it facilitates the management of business operations, customer relations, and network infrastructures. The market has evolved significantly with the growing demand for enhanced customer experiences, operational efficiency, and automation. Service providers are increasingly looking for robust solutions to streamline operations, improve service delivery, and optimize revenue management. The adoption of cloud technologies, the need for scalable systems, and the growing complexity of telecom networks are driving the demand for advanced OSS and BSS solutions. As a result, this market is expected to witness continued growth, driven by the increasing focus on digital transformation and automation within industries such as telecommunications, banking, and retail.

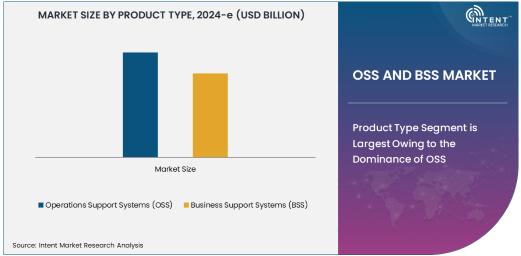

Product Type Segment is Largest Owing to the Dominance of OSS

The product type segment in the OSS and BSS market is predominantly driven by the strong demand for Operations Support Systems (OSS). OSS are integral to managing and optimizing network infrastructure, ensuring that telecommunications networks run smoothly and efficiently. They provide capabilities such as network monitoring, fault management, configuration management, and performance management. As telecom operators focus on enhancing network performance and reducing operational costs, the role of OSS solutions becomes even more critical. The market for OSS is particularly robust in regions with highly developed telecom sectors, where operators are investing in advanced solutions to support network automation and the integration of next-generation technologies like 5G.

Moreover, the transition to 5G networks is expected to further accelerate the adoption of OSS solutions. The increasing complexity of managing large-scale, high-performance networks has driven telecom operators to adopt more sophisticated OSS platforms that allow for real-time monitoring, automated troubleshooting, and predictive analytics. As the demand for such network management solutions grows, OSS will continue to dominate the product type segment within the broader OSS and BSS market.

Deployment Type Segment is Fastest Growing Owing to Cloud-Based Solutions

The cloud-based deployment type segment is the fastest growing in the OSS and BSS market, fueled by the numerous advantages offered by cloud technologies, such as scalability, flexibility, and cost efficiency. Cloud-based solutions enable telecom operators to shift from on-premise infrastructure to more dynamic, cloud-native platforms. These platforms allow for faster service deployment, easier upgrades, and reduced operational costs. Furthermore, cloud-based solutions provide enhanced security, data backup, and disaster recovery features, which are essential for businesses dealing with sensitive customer data and high-volume transactions.

The rapid growth of cloud adoption is also linked to the rise of digital transformation initiatives across industries. Companies are increasingly choosing cloud-based OSS and BSS solutions to enable greater agility and better customer engagement. With cloud-based platforms, service providers can streamline operations, manage large-scale networks more efficiently, and deliver seamless customer experiences. As businesses across different sectors look for scalable and efficient systems, the cloud-based deployment model is positioned to remain the fastest growing segment in the OSS and BSS market.

End-User Segment is Largest Owing to Telecommunications Service Providers

Telecommunications service providers are the largest end-users of OSS and BSS solutions, owing to their critical need to manage vast, complex networks and ensure smooth operations. Telecom operators rely heavily on OSS and BSS to handle everything from network provisioning to billing and customer relationship management. As telecom networks become more sophisticated, especially with the integration of 5G technologies, the demand for advanced OSS and BSS solutions to monitor, manage, and optimize these networks increases significantly. The need for improved network performance, fault detection, and faster service delivery is driving telecom providers to adopt cutting-edge solutions that can streamline operations and reduce downtime.

Telecom providers are also increasingly focusing on delivering personalized services to their customers, which requires more advanced customer experience management tools. OSS and BSS play a critical role in enabling telecom operators to offer a unified and seamless customer experience. As the telecom sector continues to expand, particularly in emerging markets, telecommunications service providers will remain the dominant end-user in the OSS and BSS market, propelling further growth in the sector.

Component Segment is Largest Owing to the Growing Demand for Software

In the component segment of the OSS and BSS market, software is the largest subsegment, driven by the increasing demand for comprehensive, all-in-one platforms that can manage both business and operational processes. The growing complexity of telecom networks, along with the need for integrated solutions that can handle billing, revenue management, fraud detection, and network optimization, has led to a surge in software adoption. Telecom providers are seeking solutions that can seamlessly integrate with their existing systems while providing real-time analytics and reporting to enhance decision-making.

The increasing reliance on software-driven solutions has also been fueled by advancements in AI and machine learning, which are being embedded into OSS and BSS platforms to enable predictive analytics and automation. These software solutions are designed to reduce the operational burden on telecom operators by automating routine tasks, detecting anomalies, and providing deeper insights into network performance and customer behavior. As software continues to play a central role in optimizing business and network operations, it will remain the largest subsegment in the OSS and BSS market.

Application Segment is Fastest Growing Owing to Network Management

The network management application segment is the fastest growing in the OSS and BSS market, largely due to the increased need for advanced tools to monitor and manage next-generation networks. With the advent of 5G, the complexity of managing telecom networks has grown exponentially, requiring more sophisticated systems that can handle high volumes of data, ensure network reliability, and optimize performance in real-time. Network management solutions enable telecom operators to oversee network traffic, detect faults, and manage network configurations with greater precision, ensuring a smooth and uninterrupted service for users.

The growing demand for high-quality, always-on network services, coupled with the need for enhanced performance in areas such as 5G, IoT, and cloud applications, has made network management a priority for telecom operators. The adoption of AI-driven network management solutions is expected to continue growing as it allows for proactive issue resolution, predictive maintenance, and greater efficiency. As a result, network management will remain the fastest growing application segment within the OSS and BSS market.

Region Segment is Largest in North America Owing to Advanced Telecom Infrastructure

North America is the largest region in the OSS and BSS market, driven by the presence of established telecom operators and advanced infrastructure in the United States and Canada. The region is home to several leading telecom service providers, such as AT&T, Verizon, and T-Mobile, all of which rely heavily on OSS and BSS solutions to manage their extensive networks and improve customer engagement. The widespread adoption of 5G technology and the ongoing investment in network modernization further fuel the demand for sophisticated OSS and BSS platforms in the region.

North America’s strong emphasis on technological innovation and digital transformation is also contributing to the growth of the OSS and BSS market. Telecom operators in this region are early adopters of cloud-based solutions and advanced analytics tools, which has placed North America at the forefront of OSS and BSS adoption. With a robust telecom ecosystem and continued advancements in network infrastructure, North America will remain the largest region for OSS and BSS solutions.

Leading Companies and Competitive Landscape

The OSS and BSS market is highly competitive, with a diverse range of players vying for market share. Leading companies in the market include Ericsson, Nokia, Amdocs, Oracle, and Huawei, all of which offer comprehensive solutions to manage network operations, customer relations, and revenue generation. These companies are investing heavily in research and development to enhance their product offerings and integrate next-generation technologies such as AI, machine learning, and cloud computing into their OSS and BSS platforms.

The competitive landscape is also marked by strategic partnerships, mergers, and acquisitions as companies look to expand their capabilities and improve their service offerings. For instance, partnerships between telecom operators and software vendors are increasingly common, as operators seek integrated solutions to streamline operations and enhance customer experiences. Additionally, the growth of cloud-based deployments has opened the door for smaller, specialized players to enter the market, creating an increasingly fragmented competitive environment.

Recent Developments:

- Ericsson launched a new cloud-native BSS platform, aimed at enabling telecom operators to improve customer experience and reduce operational costs through advanced automation and analytics.

- Amdocs signed a strategic partnership with a major telecom operator in Europe to provide end-to-end OSS/BSS solutions, focused on optimizing service delivery and accelerating digital transformation.

- Oracle unveiled a new AI-powered customer care solution within its BSS portfolio, designed to streamline customer service interactions and improve service delivery efficiency.

- Netcracker Technology was awarded a contract with a leading telecom operator in Asia to deploy a cloud-based BSS solution to enhance billing, customer experience, and analytics capabilities.

- IBM announced the acquisition of a cloud-based automation software company to enhance its OSS/BSS offerings, with the goal of providing telecom operators with greater operational flexibility and automation.

List of Leading Companies:

- Ericsson

- Huawei Technologies

- Nokia Networks

- Oracle Corporation

- Amdocs

- IBM Corporation

- Cisco Systems

- ZTE Corporation

- Tata Consultancy Services (TCS)

- Accenture

- Comarch

- Netcracker Technology

- Tech Mahindra

- Infosys

- Hewlett Packard Enterprise (HPE)XXXXX

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 32.4 Billion |

|

Forecasted Value (2030) |

USD 56.7 Billion |

|

CAGR (2025 – 2030) |

8.3% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

OSS and BSS Market By Product Type (Operations Support Systems, Business Support Systems), By Deployment Type (On-Premise, Cloud-Based, Hybrid), By End-User (Telecommunications Service Providers, IT & Technology Companies, Government & Public Sector, Media & Entertainment, Banking, Financial Services, and Insurance, Retail), By Component (Software, Services), By Application (Network Management, Customer Experience Management, Billing & Revenue Management, Order Management, Fraud Detection, Analytics & Reporting), and By Region |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Ericsson, Huawei Technologies, Nokia Networks, Oracle Corporation, Amdocs, IBM Corporation, Cisco Systems, ZTE Corporation, Tata Consultancy Services (TCS), Accenture, Comarch, Netcracker Technology, Tech Mahindra, Infosys, Hewlett Packard Enterprise (HPE) |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. OSS and BSS Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Operations Support Systems (OSS) |

|

4.2. Business Support Systems (BSS) |

|

5. OSS and BSS Market, by Deployment Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. On-Premise |

|

5.2. Cloud-Based |

|

5.3. Hybrid |

|

6. OSS and BSS Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Telecommunications Service Providers |

|

6.2. IT & Technology Companies |

|

6.3. Government & Public Sector |

|

6.4. Media & Entertainment |

|

6.5. Banking, Financial Services, and Insurance (BFSI) |

|

6.6. Retail |

|

7. OSS and BSS Market, by Component (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Software |

|

7.2. Services (Consulting, Integration, Managed Services) |

|

8. OSS and BSS Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Network Management |

|

8.2. Customer Experience Management |

|

8.3. Billing & Revenue Management |

|

8.4. Order Management |

|

8.5. Fraud Detection |

|

8.6. Analytics & Reporting |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America OSS and BSS Market, by Product Type |

|

9.2.7. North America OSS and BSS Market, by Deployment Type |

|

9.2.8. North America OSS and BSS Market, by End-User |

|

9.2.9. North America OSS and BSS Market, by Component |

|

9.2.10. North America OSS and BSS Market, by Application |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US OSS and BSS Market, by Product Type |

|

9.2.11.1.2. US OSS and BSS Market, by Deployment Type |

|

9.2.11.1.3. US OSS and BSS Market, by End-User |

|

9.2.11.1.4. US OSS and BSS Market, by Component |

|

9.2.11.1.5. US OSS and BSS Market, by Application |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. Ericsson |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Huawei Technologies |

|

11.3. Nokia Networks |

|

11.4. Oracle Corporation |

|

11.5. Amdocs |

|

11.6. IBM Corporation |

|

11.7. Cisco Systems |

|

11.8. ZTE Corporation |

|

11.9. Tata Consultancy Services (TCS) |

|

11.10. Accenture |

|

11.11. Comarch |

|

11.12. Netcracker Technology |

|

11.13. Tech Mahindra |

|

11.14. Infosys |

|

11.15. Hewlett Packard Enterprise (HPE) |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the OSS and BSS Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the OSS and BSS Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the OSS and BSS Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA