As per Intent Market Research, the Orthopedics Power Tools Market was valued at USD 1.6 billion in 2024-e and will surpass USD 2.0 billion by 2030; growing at a CAGR of 4.0% during 2025 - 2030.

The orthopedic power tools market is witnessing significant growth driven by technological advancements and the increasing demand for precision in orthopedic surgeries. These tools, which include drills, saw blades, and surgical motors, are essential for performing various complex procedures such as joint replacement, spinal surgeries, and trauma care. The demand for these tools is primarily fueled by the need for faster, more efficient surgeries that minimize patient recovery time and reduce complications. Additionally, advancements in the design and functionality of power tools are enhancing the quality of orthopedic surgeries, leading to their widespread adoption in surgical centers globally.

The global increase in orthopedic conditions, such as joint disorders, bone fractures, and degenerative diseases, is further driving the growth of the orthopedic power tools market. With an aging population more susceptible to these conditions and an increasing number of trauma cases, the market is expected to continue growing. Furthermore, the development of new technologies, such as battery-operated power tools and enhanced motor designs, is providing orthopedic surgeons with more versatile and efficient solutions for their surgical procedures.

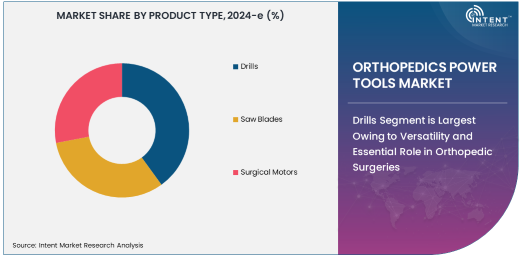

Drills Segment is Largest Owing to Versatility and Essential Role in Orthopedic Surgeries

The drills segment is the largest within the orthopedic power tools market, owing to the essential role these tools play in a wide range of orthopedic surgeries. Drills are commonly used for bone preparation, including drilling holes for screws and other fixation devices. Their versatility makes them indispensable in surgeries involving joint replacements, spinal procedures, and trauma care. The ability to perform precise and controlled drilling is vital to ensuring proper alignment and fixation of bones, which significantly influences the success of the surgery and recovery time.

Advancements in drill technology, including the development of lightweight, ergonomic designs and improved motor efficiency, have further contributed to their dominance in the market. Drills are now equipped with enhanced control features, reducing the risk of errors during surgery and improving patient outcomes. This level of precision and the broad range of applications make drills the most widely used power tool in orthopedic surgeries, solidifying their position as the largest product type segment in the market.

Battery-operated Power Tools Are Fastest Growing Owing to Portability and Convenience

Battery-operated power tools are the fastest-growing segment in the orthopedic power tools market, driven by their portability, convenience, and improved performance. These tools offer the flexibility of being used in various surgical settings, from operating rooms to ambulatory surgical centers, without the need for constant power sources or heavy cables. The advancement of battery technology has significantly improved the performance and lifespan of these tools, providing surgeons with reliable, lightweight options for orthopedic procedures.

Battery-operated power tools are particularly popular in minimally invasive surgeries and mobile surgical environments where convenience and ease of use are critical. The continued improvement of battery efficiency and charge retention, combined with lightweight designs, makes these tools an increasingly attractive choice for orthopedic surgeons. As more surgical centers look for portable, high-performance tools, the adoption of battery-operated devices is rapidly increasing, driving the growth of this segment.

Joint Replacement Surgery Segment is Largest Owing to High Demand for Procedures

The joint replacement surgery segment is the largest application segment in the orthopedic power tools market, driven by the increasing prevalence of joint-related disorders such as osteoarthritis and rheumatoid arthritis. As the global population ages, the demand for joint replacement surgeries, especially hip and knee replacements, is expected to rise significantly. Orthopedic power tools are essential in these procedures for precise bone preparation, cutting, and fixing of implants, ensuring the success of the surgery and enhancing patient recovery.

The rising number of joint replacement surgeries across both developed and emerging markets is expected to continue fueling demand for orthopedic power tools. Surgeons rely on these tools to perform procedures with accuracy and efficiency, which improves surgical outcomes and reduces complications. With technological advancements leading to more refined and specialized tools for joint replacement surgeries, this segment will continue to hold a substantial share in the orthopedic power tools market.

Hospitals Are Largest End-user Owing to High Volume of Surgeries

Hospitals represent the largest end-user segment for orthopedic power tools, primarily due to the high volume of surgeries conducted within these healthcare facilities. Hospitals typically have well-established orthopedic departments with the resources and expertise required to perform complex orthopedic surgeries such as joint replacements, spinal surgeries, and trauma care. The availability of advanced power tools is critical in ensuring efficient, high-quality surgeries, making them indispensable in hospital settings.

Additionally, hospitals have the infrastructure to support the integration of advanced power tools, which are necessary for the growing number of orthopedic procedures. With a significant increase in the aging population and a higher incidence of musculoskeletal disorders, hospitals are expected to continue being the largest end-users of orthopedic power tools. The demand for high-performance, reliable tools to meet the needs of these surgeries further solidifies hospitals' position as the dominant end-user segment in the market.

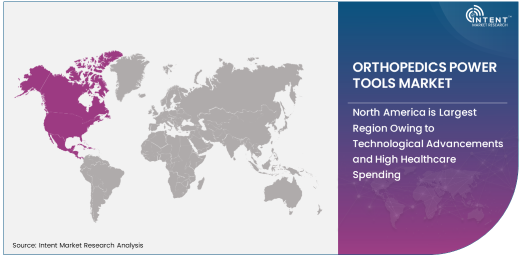

North America is Largest Region Owing to Technological Advancements and High Healthcare Spending

North America leads the orthopedic power tools market, owing to its advanced healthcare infrastructure, high healthcare spending, and early adoption of innovative technologies. The region is home to many of the world's leading orthopedic hospitals and surgical centers, which consistently integrate the latest orthopedic power tools into their operations. Additionally, the presence of prominent manufacturers and distributors of orthopedic tools in North America, particularly in the United States, has fueled market growth. The U.S. in particular accounts for a significant share of the market due to its advanced medical technologies, robust healthcare system, and a large patient population requiring orthopedic surgeries.

In addition, North America benefits from a high prevalence of orthopedic conditions such as arthritis and musculoskeletal disorders, leading to a growing demand for joint replacements and other orthopedic surgeries. The region’s focus on improving patient outcomes through the adoption of cutting-edge surgical tools contributes to the continued dominance of North America in the orthopedic power tools market. As a result, North America is expected to maintain its leadership position in the market for the foreseeable future.

Leading Companies and Competitive Landscape

The orthopedic power tools market is highly competitive, with several key players striving to maintain market leadership through continuous innovation and strategic partnerships. Leading companies such as Stryker Corporation, DePuy Synthes (Johnson & Johnson), Zimmer Biomet, and Medtronic dominate the market, offering a broad range of power tools, including drills, saw blades, and surgical motors. These companies have established strong global brands and extensive distribution networks, making their products widely available in hospitals, surgical centers, and trauma care facilities worldwide.

The competitive landscape is characterized by ongoing research and development efforts to create more efficient, lightweight, and ergonomic tools. Companies are also focusing on developing battery-operated and wireless tools to enhance portability and ease of use. As the demand for minimally invasive surgeries continues to rise, the market is witnessing increasing competition, with both established companies and new entrants striving to introduce innovative products. Strategic collaborations, mergers, and acquisitions are also common as companies aim to strengthen their product offerings and expand their reach in emerging markets, further intensifying competition in the orthopedic power tools market.

Recent Developments:

- In November 2023, Medtronic PLC launched a new battery-operated orthopedic drill for minimally invasive surgeries.

- In December 2023, Zimmer Biomet announced the release of a next-gen reciprocating saw for trauma surgeries.

- In January 2024, Stryker Corporation acquired a startup specializing in lightweight orthopedic power tools for improved ergonomics.

- In February 2024, Smith & Nephew introduced a wireless orthopedic motor system for joint replacement surgeries.

- In March 2024, Arthrex, Inc. expanded its orthopedic power tool line with the addition of a new oscillating saw for spinal surgeries.

List of Leading Companies:

- Stryker Corporation

- Zimmer Biomet

- DePuy Synthes (Johnson & Johnson)

- Medtronic PLC

- Smith & Nephew

- B. Braun Melsungen AG

- CONMED Corporation

- Mölnlycke Health Care

- MicroAire Surgical Instruments

- Arthrex, Inc.

- Smith & Nephew

- Wright Medical Group

- Aesculap Inc.

- Star Surgical

- Integra LifeSciences Holdings Corporation

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.6 billion |

|

Forecasted Value (2030) |

USD 2.0 billion |

|

CAGR (2025 – 2030) |

4.0% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Orthopedics Power Tools Market By Product Type (Drills, Saw Blades, Surgical Motors), By Application (Joint Replacement Surgery, Spinal Surgery, Trauma Surgery), By Technology (Electric Power Tools, Pneumatic Power Tools, Battery-operated Power Tools), By End-User (Hospitals, Ambulatory Surgical Centers, Trauma Centers) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Stryker Corporation, Zimmer Biomet, DePuy Synthes (Johnson & Johnson), Medtronic PLC, Smith & Nephew, B. Braun Melsungen AG, CONMED Corporation, Mölnlycke Health Care, MicroAire Surgical Instruments, Arthrex, Inc., Smith & Nephew, Wright Medical Group, Aesculap Inc., Star Surgical, Integra LifeSciences Holdings Corporation |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Orthopedics Power Tools Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Drills |

|

4.1.1. Corded |

|

4.1.2. Cordless |

|

4.2. Saw Blades |

|

4.2.1. Oscillating Saw |

|

4.2.2. Reciprocating Saw |

|

4.3. Surgical Motors |

|

4.3.1. Pneumatic Motors |

|

4.3.2. Electric Motors |

|

5. Orthopedics Power Tools Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Joint Replacement Surgery |

|

5.2. Spinal Surgery |

|

5.3. Trauma Surgery |

|

6. Orthopedics Power Tools Market, by Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Electric Power Tools |

|

6.2. Pneumatic Power Tools |

|

6.3. Battery-operated Power Tools |

|

7. Orthopedics Power Tools Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Hospitals |

|

7.2. Ambulatory Surgical Centers |

|

7.3. Trauma Centers |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Orthopedics Power Tools Market, by Product Type |

|

8.2.7. North America Orthopedics Power Tools Market, by Application |

|

8.2.8. North America Orthopedics Power Tools Market, by Technology |

|

8.2.9. By Country |

|

8.2.9.1. US |

|

8.2.9.1.1. US Orthopedics Power Tools Market, by Product Type |

|

8.2.9.1.2. US Orthopedics Power Tools Market, by Application |

|

8.2.9.1.3. US Orthopedics Power Tools Market, by Technology |

|

8.2.9.2. Canada |

|

8.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Stryker Corporation |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Zimmer Biomet |

|

10.3. DePuy Synthes (Johnson & Johnson) |

|

10.4. Medtronic PLC |

|

10.5. Smith & Nephew |

|

10.6. B. Braun Melsungen AG |

|

10.7. CONMED Corporation |

|

10.8. Mölnlycke Health Care |

|

10.9. MicroAire Surgical Instruments |

|

10.10. Arthrex, Inc. |

|

10.11. Smith & Nephew |

|

10.12. Wright Medical Group |

|

10.13. Aesculap Inc. |

|

10.14. Star Surgical |

|

10.15. Integra LifeSciences Holdings Corporation |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Orthopedics Power Tools Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Orthopedics Power Tools Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Orthopedics Power Tools Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA