As per Intent Market Research, the Orthopedic Regenerative Surgical Products Market was valued at USD 2.4 billion in 2024-e and will surpass USD 4.0 billion by 2030; growing at a CAGR of 9.1% during 2025 - 2030.

The orthopedic regenerative surgical products market is experiencing rapid growth, driven by the increasing demand for advanced surgical solutions that combine regenerative medicine with traditional orthopedic procedures. These products are designed to enhance the body’s natural healing processes, promoting faster recovery and improved outcomes in patients undergoing orthopedic surgeries. Stem cell-based products, platelet-rich plasma (PRP) kits, and growth factor delivery systems are increasingly being used in surgeries such as joint reconstruction, spinal surgeries, and tendon repair. The ability to repair and regenerate damaged tissues with these products offers an innovative approach to treating a wide range of musculoskeletal conditions.

As patients and healthcare providers seek alternatives to traditional surgical procedures, regenerative surgical products have emerged as a promising solution. These products not only enhance the healing process but also reduce the risk of complications, improve recovery time, and increase the likelihood of successful surgery outcomes. With ongoing advancements in regenerative medicine and increased clinical evidence supporting the effectiveness of these products, the orthopedic regenerative surgical products market is poised to expand significantly. The growth is also supported by rising demand for minimally invasive treatments, especially in hospitals, orthopedic clinics, and ambulatory surgical centers.

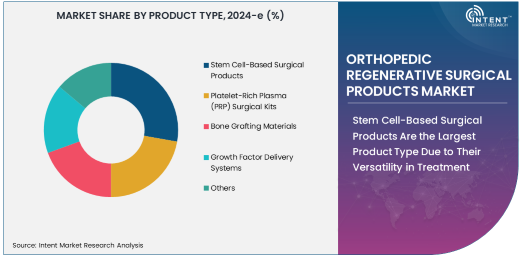

Stem Cell-Based Surgical Products Are the Largest Product Type Due to Their Versatility in Treatment

Stem cell-based surgical products are the largest product type in the orthopedic regenerative surgical products market, owing to their versatility and ability to treat a wide range of orthopedic conditions. These products utilize stem cells, particularly mesenchymal stem cells (MSCs), to promote the regeneration of bone, cartilage, tendon, and ligament tissues. Stem cell-based products are increasingly used in joint reconstruction surgeries, spinal surgeries, and the repair of tendon and ligament injuries, offering significant advantages in terms of tissue healing and regeneration.

The growing preference for stem cell-based surgical products can be attributed to their ability to support the body’s natural healing processes, reducing the need for more invasive procedures. These products not only facilitate the regeneration of damaged tissues but also reduce the likelihood of complications, such as infections or graft rejection, that are common with traditional surgical treatments. As clinical evidence supporting the effectiveness of stem cell therapies continues to grow, the demand for stem cell-based surgical products is expected to increase, solidifying their position as the largest product type in the market.

Platelet-Rich Plasma (PRP) Surgical Kits Are the Fastest Growing Product Type Due to Their Minimally Invasive Nature

Platelet-rich plasma (PRP) surgical kits are the fastest-growing product type in the orthopedic regenerative surgical products market, driven by their minimally invasive nature and effectiveness in promoting healing. PRP therapy involves the injection of a patient’s own concentrated platelets into the surgical site to accelerate tissue regeneration and repair. These surgical kits are widely used in procedures such as tendon and ligament repair, joint reconstruction, and bone fracture healing, providing an effective solution for enhancing recovery without the need for additional surgery.

The rapid growth of PRP surgical kits can be attributed to their simplicity, safety, and the growing preference for less invasive treatments. As a cost-effective and less risky alternative to traditional surgical methods, PRP therapy has gained significant traction in the orthopedic market. The increasing focus on patient-centric care and faster recovery times, coupled with the affordability and ease of administering PRP injections, is expected to fuel the continued growth of PRP surgical kits in the market.

Joint Reconstruction Is the Largest Application Due to the High Incidence of Joint Disorders

Joint reconstruction is the largest application in the orthopedic regenerative surgical products market, primarily due to the high incidence of joint disorders such as osteoarthritis, rheumatoid arthritis, and injuries caused by trauma or sports activities. Joint reconstruction surgeries often require the use of advanced surgical products like stem cell-based therapies, PRP kits, and bone grafting materials to support the regeneration of damaged tissues and restore normal joint function. With the increasing number of people suffering from degenerative joint diseases, especially among the aging population, the demand for joint reconstruction procedures has been on the rise.

Orthopedic surgeons are increasingly turning to regenerative surgical products to improve the outcomes of joint reconstruction surgeries. These products not only enhance tissue healing but also provide long-lasting results by addressing the root causes of joint degeneration. As the number of joint-related surgeries continues to grow globally, joint reconstruction remains the largest application in the orthopedic regenerative surgical products market, with these innovative products playing a critical role in improving patient outcomes.

Hospitals Are the Largest End-User Group Due to Specialized Treatment Options and Advanced Surgical Facilities

Hospitals represent the largest end-user group in the orthopedic regenerative surgical products market, owing to their capacity to offer specialized treatment options and advanced surgical facilities. Hospitals are equipped with state-of-the-art technology and skilled orthopedic surgeons who can perform complex procedures such as joint reconstruction, spinal surgery, and tendon and ligament repair. Additionally, hospitals provide a comprehensive range of care, including pre-operative consultations, advanced imaging techniques, and post-operative rehabilitation, which makes them a key player in the use of regenerative surgical products.

The adoption of regenerative surgical products in hospitals is also driven by the increasing demand for minimally invasive surgeries and faster recovery times. With their ability to provide advanced, effective treatments for musculoskeletal disorders, hospitals are the primary end-users of stem cell-based products, PRP surgical kits, and other regenerative solutions. As regenerative treatments continue to gain acceptance and evidence of their effectiveness grows, hospitals are expected to maintain their leadership role in the orthopedic regenerative surgical products market.

North America Is the Largest Region Due to Advanced Healthcare Infrastructure and High Adoption of Regenerative Technologies

North America is the largest region in the orthopedic regenerative surgical products market, largely due to the region’s advanced healthcare infrastructure, high adoption of regenerative technologies, and well-established medical research facilities. The United States, in particular, is a key market, with a large number of hospitals and orthopedic clinics adopting cutting-edge regenerative treatments such as stem cell-based products and PRP kits. The presence of major players in the regenerative medicine and surgical products industry further strengthens North America’s dominance in the market.

The growing prevalence of musculoskeletal disorders, coupled with the increasing demand for advanced treatment options, has contributed to the expansion of the market in North America. Additionally, favorable reimbursement policies and high healthcare spending in the region have facilitated the adoption of regenerative surgical products. North America’s leadership in medical innovation and its well-developed healthcare system make it the largest region in the orthopedic regenerative surgical products market, with continued growth expected in the coming years.

Competitive Landscape: Leading Companies and Market Dynamics

The orthopedic regenerative surgical products market is highly competitive, with several leading companies at the forefront of developing and commercializing innovative products. Key players in the market include Zimmer Biomet, DePuy Synthes, Medtronic, Arthrex, and Stryker, which offer a range of regenerative surgical products, including stem cell-based products, PRP surgical kits, and bone grafting materials. These companies are heavily investing in research and development to enhance product effectiveness, expand their portfolios, and cater to the increasing demand for regenerative solutions in orthopedic surgeries.

The market is also witnessing the entry of smaller players and startups, focusing on niche applications and specialized regenerative products. Strategic partnerships, mergers, and acquisitions are common in this market, as established companies seek to strengthen their product offerings and market presence. The competitive landscape is further shaped by ongoing innovations, evolving patient needs, and the growing shift toward minimally invasive surgical options. As the market continues to grow, competition is expected to intensify, driving further advancements in orthopedic regenerative surgical products.

Recent Developments:

- In January 2023, Medtronic launched a new stem cell-based surgical product aimed at enhancing bone regeneration after fractures.

- In March 2023, Stryker Corporation expanded its portfolio with a new PRP surgical kit designed for tendon repair procedures.

- In May 2023, Zimmer Biomet Holdings, Inc. received FDA approval for its new biodegradable scaffold system for orthopedic surgeries.

- In July 2023, Smith & Nephew introduced a growth factor delivery system for bone regeneration during joint replacement surgeries.

- In October 2023, Arthrex, Inc. unveiled a new regenerative surgical product line that combines stem cells with 3D bioprinting technology.

List of Leading Companies:

- Medtronic

- Stryker Corporation

- Zimmer Biomet Holdings, Inc.

- Smith & Nephew

- Orthofix International N.V.

- Mediware Information Systems, Inc.

- Biologics, Inc.

- Arthrex, Inc.

- Celgene Corporation

- Vericel Corporation

- DePuy Synthes

- Hawkins Inc.

- Osiris Therapeutics, Inc.

- Mesoblast Limited

- BioMimetic Therapeutics, Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 2.4 billion |

|

Forecasted Value (2030) |

USD 4.0 billion |

|

CAGR (2025 – 2030) |

9.1% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Orthopedic Regenerative Surgical Products Market By Product Type (Stem Cell-Based Surgical Products, Platelet-Rich Plasma (PRP) Surgical Kits, Bone Grafting Materials, Growth Factor Delivery Systems), By Application (Joint Reconstruction, Spinal Surgery, Tendon and Ligament Repair, Bone Fracture Healing), By End-User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Rehabilitation Centers) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Medtronic, Stryker Corporation, Zimmer Biomet Holdings, Inc., Smith & Nephew, Orthofix International N.V., Mediware Information Systems, Inc., Biologics, Inc., Arthrex, Inc., Celgene Corporation, Vericel Corporation, DePuy Synthes, Hawkins Inc., Osiris Therapeutics, Inc., Mesoblast Limited, BioMimetic Therapeutics, Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Orthopedic Regenerative Surgical Products Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Stem Cell-Based Surgical Products |

|

4.2. Platelet-Rich Plasma (PRP) Surgical Kits |

|

4.3. Bone Grafting Materials |

|

4.4. Growth Factor Delivery Systems |

|

4.5. Others |

|

5. Orthopedic Regenerative Surgical Products Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Joint Reconstruction |

|

5.2. Spinal Surgery |

|

5.3. Tendon and Ligament Repair |

|

5.4. Bone Fracture Healing |

|

5.5. Others |

|

6. Orthopedic Regenerative Surgical Products Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals |

|

6.2. Orthopedic Clinics |

|

6.3. Ambulatory Surgical Centers |

|

6.4. Rehabilitation Centers |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Orthopedic Regenerative Surgical Products Market, by Product Type |

|

7.2.7. North America Orthopedic Regenerative Surgical Products Market, by Application |

|

7.2.8. North America Orthopedic Regenerative Surgical Products Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Orthopedic Regenerative Surgical Products Market, by Product Type |

|

7.2.9.1.2. US Orthopedic Regenerative Surgical Products Market, by Application |

|

7.2.9.1.3. US Orthopedic Regenerative Surgical Products Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Medtronic |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Stryker Corporation |

|

9.3. Zimmer Biomet Holdings, Inc. |

|

9.4. Smith & Nephew |

|

9.5. Orthofix International N.V. |

|

9.6. Mediware Information Systems, Inc. |

|

9.7. Biologics, Inc. |

|

9.8. Arthrex, Inc. |

|

9.9. Celgene Corporation |

|

9.10. Vericel Corporation |

|

9.11. DePuy Synthes |

|

9.12. Hawkins Inc. |

|

9.13. Osiris Therapeutics, Inc. |

|

9.14. Mesoblast Limited |

|

9.15. BioMimetic Therapeutics, Inc. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Orthopedic Regenerative Surgical Products Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Orthopedic Regenerative Surgical Products Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Orthopedic Regenerative Surgical Products Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA