As per Intent Market Research, the Organic Milk Market was valued at USD 8.0 billion in 2024-e and will surpass USD 12.5 billion by 2030; growing at a CAGR of 7.7% during 2025 - 2030.

The organic milk market has been growing steadily due to increasing consumer awareness about the health benefits and environmental advantages of organic products. Organic milk is produced without the use of synthetic pesticides, hormones, or antibiotics, making it a preferred choice for health-conscious consumers. As more people shift toward organic diets, the demand for organic milk has surged, supported by growing concerns about food quality and safety. The market is also benefiting from the rising trend of sustainability, as organic farming practices tend to be more environmentally friendly compared to conventional methods.

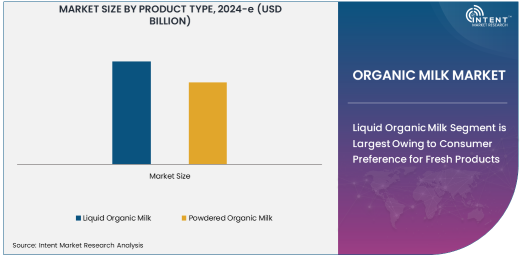

The organic milk market is divided into two main product types: liquid organic milk and powdered organic milk. While liquid organic milk has traditionally been the most popular choice, powdered organic milk is gaining traction due to its extended shelf life and convenience, particularly in regions where fresh milk distribution may be challenging. Additionally, the rise in e-commerce and online retail has further boosted the accessibility of organic milk, allowing consumers in remote areas to easily access high-quality organic products. As the market continues to expand, technological innovations in packaging and preservation are improving product availability and extending the shelf life of organic milk.

Liquid Organic Milk Segment is Largest Owing to Consumer Preference for Fresh Products

The liquid organic milk segment is the largest within the organic milk market, driven by consumer preference for fresh, ready-to-consume dairy products. Liquid organic milk is seen as a more natural and healthier alternative to conventional milk, with many consumers willing to pay a premium for the assurance that the product has been produced without harmful chemicals or additives. The increasing popularity of organic food products, particularly among millennials and health-conscious consumers, has contributed significantly to the growth of the liquid organic milk segment.

The segment is further supported by advancements in the dairy industry that allow for better preservation methods, such as ultra-pasteurization and vacuum sealing, which help to maintain the milk’s freshness and quality. Liquid organic milk is widely available in supermarkets, hypermarkets, and retail stores, making it accessible to a broad consumer base. As demand for organic food continues to rise, the liquid organic milk segment is expected to maintain its dominance in the market, with increased availability and a growing number of product offerings.

Powdered Organic Milk is Fastest Growing Product Type Owing to Convenience and Long Shelf Life

Powdered organic milk is the fastest-growing segment in the organic milk market, driven by its convenience and long shelf life. Powdered milk is easy to store and transport, making it ideal for consumers in regions with limited access to fresh organic milk. This product type also appeals to households that require milk for various applications, such as baking, cooking, and the preparation of baby formula. Additionally, powdered organic milk is becoming increasingly popular in countries where fresh organic milk is not widely available, further boosting its growth.

The extended shelf life of powdered organic milk makes it an attractive option for both consumers and manufacturers. It allows for better inventory management, reduces waste, and ensures that products remain available year-round. As consumers become more aware of the convenience and benefits of powdered milk, the segment is expected to continue experiencing rapid growth. With advancements in processing and packaging technologies, powdered organic milk is becoming more accessible and affordable, supporting its expansion in the global market.

Supermarkets/Hypermarkets Are Largest Distribution Channel Owing to Accessibility and Consumer Trust

Supermarkets and hypermarkets are the largest distribution channel for organic milk, primarily due to their wide reach, convenience, and consumer trust. These retail outlets are the go-to destinations for consumers seeking organic products, including organic milk. Supermarkets and hypermarkets offer a broad range of organic milk options, allowing consumers to choose from various brands, product types, and packaging sizes. The large-scale nature of these stores enables them to offer competitive pricing, attracting a wide range of customers.

Furthermore, supermarkets and hypermarkets are known for their established supply chains, which ensure consistent product availability and reliability. As consumer demand for organic products continues to grow, supermarkets and hypermarkets will remain central to the distribution of organic milk, especially in developed markets where these retail outlets dominate the grocery sector. The convenience of one-stop shopping for organic groceries makes supermarkets and hypermarkets a key player in the distribution of organic milk products.

Online Retailers Are Fastest Growing Distribution Channel Owing to Changing Consumer Shopping Habits

Online retailers are the fastest-growing distribution channel for organic milk, driven by the changing shopping habits of consumers. With the rise of e-commerce platforms and the increasing popularity of online grocery shopping, consumers are increasingly turning to the internet to purchase organic milk and other dairy products. Online retail offers the convenience of shopping from home, access to a wider variety of brands, and often better pricing compared to traditional retail outlets. Additionally, online retailers can reach consumers in remote or underserved regions where organic milk may not be readily available in local stores.

The COVID-19 pandemic accelerated the shift toward online shopping, and many consumers have continued to prefer online platforms for grocery purchases due to convenience and safety concerns. Online retailers also offer subscription-based services, allowing consumers to receive regular deliveries of organic milk and other products, further enhancing the convenience factor. As more people embrace online shopping, the demand for organic milk through this channel is expected to continue growing, making online retailers a key player in the market’s future expansion.

Households Are Largest End-user Segment Owing to Rising Demand for Healthy and Organic Products

Households are the largest end-user segment in the organic milk market, as the demand for organic products grows among health-conscious consumers. Organic milk is seen as a healthier option compared to conventional milk, particularly for families looking to provide the best nutrition for their children and other household members. As awareness about the benefits of organic food increases, households are increasingly choosing organic milk as part of their daily diet, further driving the demand in the market.

The preference for organic products is not limited to just milk, as many households are adopting an overall organic lifestyle, which includes organic vegetables, fruits, and dairy products. This shift in consumer behavior is expected to continue fueling the demand for organic milk, as more families seek to improve their diets and reduce exposure to synthetic chemicals. As the market for organic food expands, households will remain the dominant end-user segment, contributing to sustained growth in the organic milk market.

North America is Largest Region Owing to High Consumer Demand and Strong Distribution Network

North America is the largest regional market for organic milk, driven by high consumer demand for organic products and a well-established distribution network. The United States and Canada are major consumers of organic milk, with a large segment of the population preferring organic food due to health and environmental concerns. The availability of organic milk in major retail outlets, supermarkets, and online platforms further supports the growth of the market in North America. Additionally, North American consumers are more likely to purchase premium organic products, which drives the market for organic milk.

The growing awareness of the benefits of organic food, combined with strong government regulations that promote organic farming practices, has created a favorable environment for the organic milk market in North America. As demand for organic dairy products continues to rise, North America is expected to maintain its leadership position in the global market. With a robust retail infrastructure and an increasingly health-conscious population, the region remains a key driver of growth for the organic milk market.

Leading Companies and Competitive Landscape

The organic milk market is highly competitive, with several key players striving to capture market share by offering high-quality organic products and expanding their distribution networks. Leading companies in the market include Horizon Organic (Danone), Organic Valley, Stonyfield Organic, and Whole Foods Market, which offer a wide range of organic milk products through various distribution channels. These companies focus on maintaining high-quality standards, obtaining certifications, and investing in sustainability initiatives to appeal to environmentally-conscious consumers.

The competitive landscape is marked by ongoing innovation, as companies seek to differentiate their products through packaging, product variety, and convenience. Some companies are also expanding their product lines to include lactose-free organic milk, flavored organic milk, and organic milk alternatives to cater to the diverse needs of consumers. As the market for organic milk continues to grow, companies are increasingly focusing on improving their supply chains, reaching new consumers, and capitalizing on the growing demand for organic dairy products. This competitive environment ensures continuous innovation and expansion in the organic milk market.

Recent Developments:

- In November 2024, Horizon Organic announced the launch of a new line of organic milk with added probiotics for better digestive health.

- In October 2024, Organic Valley expanded its product range with a new organic goat milk variant for broader consumer choice.

- In September 2024, Danone S.A. partnered with local organic farmers to enhance its organic milk supply chain in Europe.

- In August 2024, Stonyfield Organic launched a new packaging initiative to reduce plastic use and improve sustainability.

- In July 2024, Whole Foods Market introduced a line of organic milk sourced from grass-fed cows with no added hormones.

List of Leading Companies:

- Organic Valley

- Horizon Organic

- Stonyfield Organic

- Whole Foods Market

- Danone S.A.

- Nestlé S.A.

- Clover Stornetta Farms

- Aurora Organic Dairy

- The Kroger Co.

- WhiteWave Foods

- Yeo Valley Organic

- Happy Cow Organic

- Emmi Group

- The Gleaner Company Ltd.

- Maple Hill Creamery

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 8.0 billion |

|

Forecasted Value (2030) |

USD 12.5 billion |

|

CAGR (2025 – 2030) |

7.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Organic Milk Market By Product Type (Liquid Organic Milk, Powdered Organic Milk), By Distribution Channel (Supermarkets/Hypermarkets, Online Retailers, Direct Sales), By End-User (Households, Foodservice Providers, Manufacturers) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Organic Valley, Horizon Organic, Stonyfield Organic, Whole Foods Market, Danone S.A., Nestlé S.A., Clover Stornetta Farms, Aurora Organic Dairy, The Kroger Co., WhiteWave Foods, Yeo Valley Organic, Happy Cow Organic, Emmi Group, The Gleaner Company Ltd., Maple Hill Creamery |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Organic Milk Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Liquid Organic Milk |

|

4.1.1. Cow Milk |

|

4.1.2. Goat Milk |

|

4.1.3. Other Organic Liquid Milk |

|

4.2. Powdered Organic Milk |

|

4.2.1. Organic Cow Milk Powder |

|

4.2.2. Organic Goat Milk Powder |

|

4.2.3. Other Organic Milk Powders |

|

5. Organic Milk Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Supermarkets/Hypermarkets |

|

5.2. Online Retailers |

|

5.3. Direct Sales |

|

6. Organic Milk Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Households |

|

6.2. Foodservice Providers |

|

6.3. Manufacturers |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Organic Milk Market, by Product Type |

|

7.2.7. North America Organic Milk Market, by Distribution Channel |

|

7.2.8. North America Organic Milk Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Organic Milk Market, by Product Type |

|

7.2.9.1.2. US Organic Milk Market, by Distribution Channel |

|

7.2.9.1.3. US Organic Milk Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Organic Valley |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Horizon Organic |

|

9.3. Stonyfield Organic |

|

9.4. Whole Foods Market |

|

9.5. Danone S.A. |

|

9.6. Nestlé S.A. |

|

9.7. Clover Stornetta Farms |

|

9.8. Aurora Organic Dairy |

|

9.9. The Kroger Co. |

|

9.10. WhiteWave Foods |

|

9.11. Yeo Valley Organic |

|

9.12. Happy Cow Organic |

|

9.13. Emmi Group |

|

9.14. The Gleaner Company Ltd. |

|

9.15. Maple Hill Creamery |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Organic Milk Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Organic Milk Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Organic Milk Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA