As per Intent Market Research, the Organic Baby Food Market was valued at USD 10.5 Billion in 2024-e and will surpass USD 21.0 Billion by 2030; growing at a CAGR of 12.1% during 2025-2030.

The organic baby food market is experiencing significant growth, driven by an increasing awareness among parents regarding the health and safety of their children. As concerns over chemical additives, pesticides, and genetically modified organisms (GMOs) grow, parents are opting for organic alternatives to ensure that their babies receive the highest-quality nutrition from the start. Organic baby foods are perceived as healthier and safer for infants and toddlers, as they contain fewer artificial ingredients, preservatives, and harmful chemicals. This shift towards organic products has led to a steady rise in demand for organic baby food, with parents becoming more discerning about the food their children consume.

Additionally, the rising trend of health-conscious eating, alongside increased disposable incomes, has contributed to the growth of the organic baby food market. Parents today are more focused on providing their children with nutritious, wholesome meals that promote healthy growth and development. This has led to an expanding product range in the market, including organic baby cereals, snacks, and meals. The availability of organic baby food through various distribution channels, such as online retailers and supermarkets, has further contributed to the market's growth, as it provides greater convenience for parents in selecting and purchasing these products.

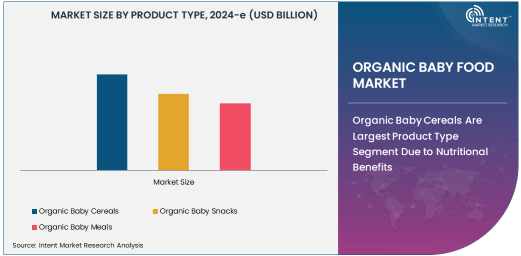

Organic Baby Cereals Are Largest Product Type Segment Due to Nutritional Benefits

Organic baby cereals dominate the organic baby food market, owing to their nutritional benefits and the convenience they offer to parents. Baby cereals, especially those made from organic grains, provide essential nutrients such as iron, vitamins, and minerals, which are crucial for the healthy growth and development of infants. These cereals are often fortified with additional nutrients like DHA, which is essential for brain development. Organic baby cereals are typically free from artificial sweeteners, preservatives, and pesticides, making them a preferred choice for health-conscious parents.

As infants begin transitioning to solid foods, baby cereals serve as an easy-to-digest and highly nutritious option. The convenience of preparing organic baby cereals, often requiring only the addition of water or milk, makes them a staple in many households. With a growing focus on infant nutrition and safety, organic baby cereals continue to be the largest segment, accounting for a significant portion of the market share, and are expected to see sustained growth as more parents opt for healthier options for their babies.

Powdered Form Is Fastest Growing Due to Portability and Convenience

The powdered form of organic baby food is the fastest-growing segment, driven by its portability, ease of storage, and convenience. Powdered organic baby food, which often includes baby cereals and meal options, is highly popular among parents who are looking for quick and hassle-free meal preparation. With a busy lifestyle, parents appreciate the ability to prepare organic meals for their babies with minimal effort—simply mixing the powdered product with water or milk.

The powdered form is ideal for on-the-go parents, as it is lightweight, easy to store, and can be prepared anytime, anywhere. Moreover, powdered baby foods typically have a longer shelf life compared to ready-to-eat options, making them more appealing for households with limited storage space. As more parents prioritize convenience in meal preparation, the powdered form of organic baby food is seeing rapid adoption, positioning it as the fastest-growing form segment in the market.

Online Retailers Are Largest Distribution Channel Segment Due to Ease of Access and Convenience

Online retailers are the largest distribution channel for organic baby food, driven by the growing preference for e-commerce shopping, especially among tech-savvy and busy parents. Online platforms provide a convenient way for parents to browse and purchase organic baby food from a wide variety of brands and product types. The ability to compare prices, read reviews, and access detailed product information makes online shopping particularly attractive for parents who want to make informed decisions.

Additionally, online shopping offers the convenience of home delivery, which is especially valuable for parents who may have limited time to visit physical stores. The ongoing rise in online shopping, coupled with the availability of subscription-based services and the convenience of purchasing from home, has made online retailers the dominant distribution channel for organic baby food. As e-commerce continues to expand globally, online retailers are expected to remain the largest segment in the market, catering to the growing demand for organic baby food products.

Infants (0-12 Months) Are Largest End-User Segment Due to Nutritional Focus

The infants (0-12 months) end-user segment is the largest in the organic baby food market, driven by the critical need for proper nutrition during the early stages of development. Infancy is a time when babies require a high level of nutrients to support growth, immune function, and brain development. Organic baby food products, particularly those designed for infants, are formulated to meet these nutritional needs while being gentle on babies' digestive systems.

As parents become increasingly concerned about the potential health risks associated with non-organic baby food, they are turning to organic alternatives to ensure that their infants receive safe and nutritious meals. Organic baby cereals, snacks, and meals are especially popular in this segment, as they provide essential vitamins, minerals, and other nutrients critical for the healthy development of infants. This growing awareness of infant health and safety will continue to drive the demand for organic baby food products for infants, solidifying the segment’s dominance in the market.

Asia-Pacific is Fastest Growing Region Due to Rising Birth Rates and Health Consciousness

The Asia-Pacific (APAC) region is the fastest-growing market for organic baby food, driven by rising birth rates, increasing disposable income, and growing health consciousness among parents. Countries such as China, India, and Japan are seeing a surge in demand for organic baby food, as middle-class families are becoming more aware of the benefits of organic products and are willing to spend more on the health of their children. The rapid urbanization and shift towards modern lifestyles in these countries have contributed to the increasing preference for organic food options, as parents seek high-quality, safe, and nutritious foods for their babies.

The rise of e-commerce platforms in the region has also made organic baby food more accessible to a larger audience, particularly in urban areas. As the demand for healthier food options grows, APAC is expected to remain the fastest-growing region in the organic baby food market, driven by factors such as improved living standards, increasing awareness of child nutrition, and the adoption of Western-style consumption habits.

Leading Companies and Competitive Landscape

The organic baby food market is highly competitive, with several leading players offering a range of organic food products to meet the growing demand from health-conscious parents. Prominent companies in the market include Nestlé S.A., Danone S.A., Hain Celestial Group, Earth's Best Organic, and Beech-Nut Nutrition Corporation. These companies have established strong brand recognition and a wide distribution network to cater to the global demand for organic baby food.

To stay competitive, companies are focusing on product innovation, expanding their organic product offerings, and strengthening their presence in key markets, particularly in the Asia-Pacific and North American regions. In addition, partnerships with e-commerce platforms and retailers are enabling these companies to expand their reach and improve accessibility for consumers. The market is also witnessing an increasing focus on clean-label products, where companies are emphasizing transparency, offering organic certifications, and marketing their products as free from artificial additives and preservatives. As the organic baby food market continues to expand, companies are likely to adopt further strategies such as product diversification, sustainability initiatives, and regional expansion to stay ahead of the competition.

Recent Developments:

- In December 2024, Gerber announced the launch of a new line of organic baby snacks made from 100% organic fruits and vegetables.

- In November 2024, Danone expanded its organic baby food offerings with a new range of dairy-free products for toddlers.

- In October 2024, Hain Celestial introduced a new line of organic baby meals in convenient pouch packaging, aiming to improve portability for parents.

- In September 2024, Plum Organics partnered with a leading retailer to expand the availability of their organic baby food range in North America.

- In August 2024, Happy Family Organics launched an innovative line of organic snacks designed for infants transitioning to solid foods.

List of Leading Companies:

- Nestlé S.A.

- Danone S.A.

- Hain Celestial Group, Inc.

- Gerber Products Company (Nestlé)

- Earth's Best (Hain Celestial Group)

- Happy Family Organics

- Bellamy's Organic

- Plum Organics (Campbell Soup Company)

- Baby's Only Organic

- Sprout Organic Foods

- Organix Brands Ltd.

- The Kraft Heinz Company

- Amara Organic Foods

- Nature’s One, Inc.

- Yumi Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 10.5 Billion |

|

Forecasted Value (2030) |

USD 21.0 Billion |

|

CAGR (2025 – 2030) |

12.1% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Organic Baby Food Market by Product Type (Organic Baby Cereals, Organic Baby Snacks, Organic Baby Meals), Form (Ready to Eat, Powdered, Pouches), Distribution Channel (Online Retailers, Supermarkets & Hypermarkets, Convenience Stores), End-User (Infants 0-12 months, Toddlers 1-3 years) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Nestlé S.A., Danone S.A., Hain Celestial Group, Inc., Gerber Products Company (Nestlé), Earth's Best (Hain Celestial Group), Happy Family Organics, Bellamy's Organic, Plum Organics (Campbell Soup Company), Baby's Only Organic, Sprout Organic Foods, Organix Brands Ltd., The Kraft Heinz Company, Amara Organic Foods, Nature’s One, Inc., Yumi Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Organic Baby Food Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Organic Baby Cereals |

|

4.2. Organic Baby Snacks |

|

4.3. Organic Baby Meals |

|

5. Organic Baby Food Market, by Form (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Ready to Eat |

|

5.2. Powdered |

|

5.3. Pouches |

|

6. Organic Baby Food Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Online Retailers |

|

6.2. Supermarkets & Hypermarkets |

|

6.3. Convenience Stores |

|

7. Organic Baby Food Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Infants (0-12 months) |

|

7.2. Toddlers (1-3 years) |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Organic Baby Food Market, by Product Type |

|

8.2.7. North America Organic Baby Food Market, by Form |

|

8.2.8. North America Organic Baby Food Market, by Distribution Channel |

|

8.2.9. North America Organic Baby Food Market, by End-User |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Organic Baby Food Market, by Product Type |

|

8.2.10.1.2. US Organic Baby Food Market, by Form |

|

8.2.10.1.3. US Organic Baby Food Market, by Distribution Channel |

|

8.2.10.1.4. US Organic Baby Food Market, by End-User |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Nestlé S.A. |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Danone S.A. |

|

10.3. Hain Celestial Group, Inc. |

|

10.4. Gerber Products Company (Nestlé) |

|

10.5. Earth's Best (Hain Celestial Group) |

|

10.6. Happy Family Organics |

|

10.7. Bellamy's Organic |

|

10.8. Plum Organics (Campbell Soup Company) |

|

10.9. Baby's Only Organic |

|

10.10. Sprout Organic Foods |

|

10.11. Organix Brands Ltd. |

|

10.12. The Kraft Heinz Company |

|

10.13. Amara Organic Foods |

|

10.14. Nature’s One, Inc. |

|

10.15. Yumi Inc. |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Organic Baby Food Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Organic Baby Food Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Organic Baby Food Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA