As per Intent Market Research, the Organ Transplant Market was valued at USD 18.9 Billion in 2024-e and will surpass USD 34.7 Billion by 2030; growing at a CAGR of 10.7% during 2025 - 2030.

The organ transplant market is a crucial segment of the healthcare industry, driven by the rising incidence of organ failure and the increasing demand for life-saving transplants. The market includes various organ types such as kidneys, livers, hearts, lungs, and other organs that are required for transplant procedures. These transplants are vital for patients suffering from end-stage organ failure or severe organ dysfunction. Organ transplantation not only saves lives but also improves the quality of life for patients. With advancements in medical technology and a growing focus on organ preservation and transport, the organ transplant market is expanding, offering innovative solutions for better transplant outcomes. The market is poised to grow as more efficient and reliable transplant techniques, immunosuppressive therapies, and preservation methods continue to evolve.

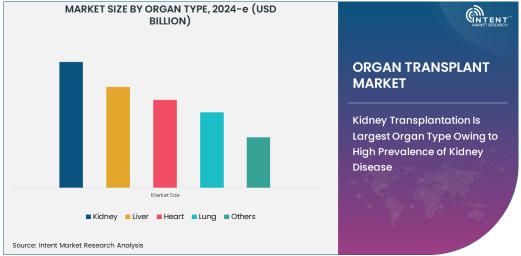

Kidney Transplantation Is Largest Organ Type Owing to High Prevalence of Kidney Disease

Kidney transplantation is the largest organ type in the organ transplant market, primarily due to the high prevalence of chronic kidney diseases (CKD) and end-stage renal disease (ESRD). Kidney failure, often caused by conditions such as diabetes, hypertension, and genetic disorders, is a major health issue globally. Kidney transplants offer the best long-term solution for patients with kidney failure, making kidney transplantation the most common and widely performed organ transplant worldwide.

The growing number of patients requiring kidney transplants is driving the demand for both donor organs and transplant-related services. In addition, the availability of organ donors remains a significant challenge, highlighting the importance of organ preservation and transportation technologies to ensure that kidneys reach transplant recipients in optimal condition. As the global incidence of kidney disease continues to rise, kidney transplantation will maintain its position as the largest organ type in the transplant market.

Allogeneic Transplants Are Largest Type of Transplantation Owing to Widespread Use

Allogeneic transplants, where organs are donated by a different individual, are the largest type of transplantation in the organ transplant market. Allogeneic transplants are the standard practice for most solid organ transplants, including kidney, liver, heart, and lung transplants. The high prevalence of organ failure and the need for suitable donor organs make allogeneic transplants essential in the treatment of end-stage organ diseases.

Allogeneic transplantation is widely used in clinical settings because it offers the best chance of saving lives and improving the quality of life for patients with terminal organ failure. While autologous transplants (where the donor and recipient are the same person) have their place, particularly in areas like stem cell therapy, they are less common for solid organ transplants. The larger number of allogeneic transplants conducted each year positions this segment as the largest in the organ transplant market.

Organ Transport Is Largest Application Owing to Essential Role in Organ Viability

The organ transport application is the largest segment within the organ transplant market, owing to its essential role in maintaining the viability and functionality of donor organs. After an organ is procured from a donor, it must be transported to the transplant center, often over long distances, within a specific time frame to ensure it remains suitable for transplantation. Efficient organ transport systems are crucial for organ preservation and for ensuring successful transplant outcomes.

As the number of organ transplants increases globally, the need for reliable and efficient transport solutions becomes even more critical. Advanced technologies in organ preservation and transport, including cold storage and machine perfusion systems, are being developed to ensure the safe and effective movement of organs from donor to recipient. This growing emphasis on organ transport makes it the largest application segment in the organ transplant market.

Hospitals Are Largest End-Use Industry Owing to Central Role in Organ Transplant Procedures

Hospitals are the largest end-use industry in the organ transplant market, as they play a central role in performing organ transplants and providing post-operative care. Hospitals are the primary settings for transplant surgeries, where advanced medical technologies and experienced transplant teams are essential for successful outcomes. In addition to performing the transplants, hospitals are also responsible for administering immunosuppressive therapies and managing the overall health of transplant recipients.

The increasing number of transplant surgeries performed in hospitals, coupled with ongoing research and development aimed at improving transplant success rates, ensures that hospitals remain the dominant end-user of organ transplant services and technologies. As the demand for organ transplants rises, hospitals are at the forefront of adopting new techniques in organ preservation, transport, and recovery, further driving the growth of this segment.

North America Is Largest Region Owing to Advanced Healthcare Infrastructure and High Transplantation Rates

North America is the largest region in the organ transplant market, primarily due to its advanced healthcare infrastructure, high rates of organ transplantation, and strong focus on organ donor programs. The United States, in particular, has a well-established system for organ procurement and transplantation, with numerous transplant centers and hospitals performing high numbers of kidney, liver, heart, and lung transplants annually. Additionally, North America benefits from significant investments in medical research and the development of advanced technologies in organ preservation, transport, and recovery.

As the region continues to lead in organ transplant procedures, North America remains the largest market for organ transplant products and services. The growing aging population, increasing rates of chronic diseases, and ongoing improvements in transplantation technologies will contribute to the sustained growth of the organ transplant market in North America.

Competitive Landscape and Key Players

The organ transplant market is competitive, with several key players leading the development and provision of organ transplantation solutions. Companies such as Organ Recovery Systems, TransMedics, XVIVO, and Paragonix Technologies are at the forefront of providing advanced technologies for organ preservation, transport, and recovery. These companies specialize in solutions that improve organ viability, reduce ischemic injury, and enhance transplant outcomes.

The competitive landscape is marked by a focus on product innovation, strategic partnerships with hospitals and transplant centers, and ongoing research to improve organ transplantation success rates. Additionally, the market is seeing increased collaboration between pharmaceutical companies, research institutes, and organ transplant centers to develop new treatments and technologies for organ transplantation. As the demand for organ transplants continues to grow, leading companies are poised to maintain a strong presence in the market by continually advancing their offerings and responding to the evolving needs of healthcare providers.

Recent Developments:

- TransMedics, Inc. launched a new organ care system for lung transplantation that significantly improves post-transplant outcomes.

- Paragonix Technologies expanded its liver transplant device portfolio, receiving approval for a new preservation system to extend organ viability.

- Organ Recovery Systems, Inc. entered a partnership with a leading transplant center to enhance organ recovery with advanced preservation techniques.

- LifeNet Health introduced an innovative organ transport system that reduces organ preservation times and improves transplant success rates.

- Medtronic PLC announced the acquisition of a company specializing in organ preservation technologies, strengthening its position in the transplant market

List of Leading Companies:

- Organ Recovery Systems, Inc.

- TransMedics, Inc.

- Paragonix Technologies

- XVIVO Perfusion AB

- LifeNet Health

- Stryker Corporation

- Baxter International Inc.

- Medtronic PLC

- Abbott Laboratories

- BioLife Solutions, Inc.

- Organ Transport Systems

- Hesperis S.A.

- Siemens Healthineers

- Thermo Fisher Scientific Inc.

- OCS Medical Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 18.9 Billion |

|

Forecasted Value (2030) |

USD 34.7 Billion |

|

CAGR (2025 – 2030) |

10.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Global Organ Transplant Market by Organ Type (Kidney, Liver, Heart, Lung), by Type of Transplantation (Allogeneic Transplants, Autologous Transplants), by End-Use Industry (Hospitals, Organ Transplantation Centers, Research Institutes), by Application (Organ Transport, Organ Preservation, Organ Recovery) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Organ Recovery Systems, Inc., TransMedics, Inc., Paragonix Technologies, XVIVO Perfusion AB, LifeNet Health, Stryker Corporation, Medtronic PLC, Abbott Laboratories, BioLife Solutions, Inc., Organ Transport Systems, Hesperis S.A., Siemens Healthineers, OCS Medical Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Organ Transplant Market, by Organ Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Kidney |

|

4.2. Liver |

|

4.3. Heart |

|

4.4. Lung |

|

4.5. Others |

|

5. Organ Transplant Market, by Type of Transplantation (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Allogeneic Transplants |

|

5.2. Autologous Transplants |

|

6. Organ Transplant Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals |

|

6.2. Organ Transplantation Centers |

|

6.3. Research Institutes |

|

7. Organ Transplant Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Organ Transport |

|

7.2. Organ Preservation |

|

7.3. Organ Recovery |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Organ Transplant Market, by Organ Type |

|

8.2.7. North America Organ Transplant Market, by Type of Transplantation |

|

8.2.8. North America Organ Transplant Market, by End-Use Industry |

|

8.2.9. North America Organ Transplant Market, by Application |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Organ Transplant Market, by Organ Type |

|

8.2.10.1.2. US Organ Transplant Market, by Type of Transplantation |

|

8.2.10.1.3. US Organ Transplant Market, by End-Use Industry |

|

8.2.10.1.4. US Organ Transplant Market, by Application |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Organ Recovery Systems, Inc. |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. TransMedics, Inc. |

|

10.3. Paragonix Technologies |

|

10.4. XVIVO Perfusion AB |

|

10.5. LifeNet Health |

|

10.6. Stryker Corporation |

|

10.7. Baxter International Inc. |

|

10.8. Medtronic PLC |

|

10.9. Abbott Laboratories |

|

10.10. BioLife Solutions, Inc. |

|

10.11. Organ Transport Systems |

|

10.12. Hesperis S.A. |

|

10.13. Siemens Healthineers |

|

10.14. Thermo Fisher Scientific Inc. |

|

10.15. OCS Medical Inc. |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Organ Transplant Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Organ Transplant Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Organ Transplant Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA