As per Intent Market Research, the Organ Transplant Immunosuppressant Drugs Market was valued at USD 6.2 Billion in 2024-e and will surpass USD 9.5 Billion by 2030; growing at a CAGR of 7.3% during 2025 - 2030.

The Organ Transplant Immunosuppressant Drugs Market is a critical segment within the healthcare industry, driven by the increasing number of organ transplantation procedures and the need to prevent organ rejection. Immunosuppressant drugs are essential for patients who have undergone organ transplants, as they help suppress the immune system’s natural response, preventing the body from rejecting the transplanted organ. This market is evolving with new drug classes, formulations, and therapies that offer better outcomes for transplant recipients. As the global demand for organ transplants continues to rise, there is a growing need for more effective immunosuppressive treatments to ensure the success of these life-saving procedures.

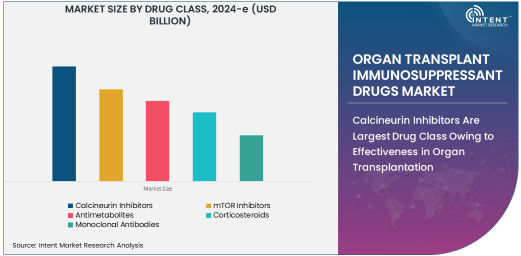

Calcineurin Inhibitors Are Largest Drug Class Owing to Effectiveness in Organ Transplantation

Calcineurin inhibitors, such as tacrolimus and cyclosporine, are the largest drug class in the organ transplant immunosuppressant drugs market. These drugs have been the cornerstone of immunosuppressive therapy for transplant recipients for several decades. They work by inhibiting the activation of T-cells, which play a key role in the body’s immune response against transplanted organs. By reducing T-cell activity, calcineurin inhibitors significantly lower the risk of organ rejection and increase the likelihood of transplant success.

The large market share of calcineurin inhibitors can be attributed to their proven effectiveness in preventing organ rejection, particularly in kidney, liver, and heart transplantation. These drugs are widely used in clinical practice due to their strong track record of success in organ transplantation, making them the most commonly prescribed immunosuppressants. Despite newer classes of immunosuppressants emerging, calcineurin inhibitors continue to dominate the market, largely because of their established efficacy and the extensive clinical experience surrounding their use.

mTOR Inhibitors Are Fastest Growing Drug Class Owing to Enhanced Efficacy and Safety Profile

mTOR inhibitors, including everolimus and sirolimus, represent the fastest growing drug class in the organ transplant immunosuppressant drugs market. These drugs work by inhibiting the mammalian target of rapamycin (mTOR), a protein that regulates cell growth and immune responses. By suppressing mTOR, these drugs help prevent T-cell activation and reduce the risk of organ rejection. mTOR inhibitors are gaining popularity due to their dual benefits of preventing organ rejection while also reducing the risk of certain transplant-related complications, such as cancer and kidney dysfunction.

The growth of mTOR inhibitors is also driven by their improved safety profile, particularly when used in combination with calcineurin inhibitors. These drugs are now being increasingly prescribed for kidney, liver, and heart transplant patients, as they offer a more targeted approach to immunosuppression with potentially fewer long-term side effects. As clinical research continues to highlight their benefits, mTOR inhibitors are expected to see sustained growth in the coming years.

Kidney Transplantation Is Largest Application Owing to High Prevalence of Kidney Disease

Kidney transplantation is the largest application segment in the organ transplant immunosuppressant drugs market, primarily due to the high prevalence of chronic kidney diseases and end-stage renal failure. With over 200,000 kidney transplants performed globally each year, the need for immunosuppressive drugs to prevent organ rejection is critical in this segment. Kidney transplant recipients are often required to use a combination of immunosuppressants, including calcineurin inhibitors and mTOR inhibitors, to ensure long-term organ survival and function.

The high demand for kidney transplants is driven by the rising incidence of kidney diseases, such as diabetes and hypertension, which are major contributors to kidney failure. As the number of patients requiring kidney transplants continues to increase, the demand for effective immunosuppressive therapies also rises. Kidney transplantation remains the most common form of solid organ transplant, cementing its position as the largest application for organ transplant immunosuppressant drugs.

Hospitals Are Largest End-Use Industry Owing to Central Role in Organ Transplant Procedures

Hospitals are the largest end-use industry in the organ transplant immunosuppressant drugs market, as they play a central role in organ transplant procedures and the post-operative care of transplant patients. Hospitals are the primary setting for organ transplantation surgeries, and they are responsible for administering immunosuppressive therapies to transplant recipients. Given the complexity of organ transplant procedures and the critical need for post-transplant care, hospitals rely on a range of immunosuppressant drugs to manage patients’ immune responses and prevent rejection of transplanted organs.

The large hospital market share is driven by the increasing number of transplant surgeries performed globally, along with the need for comprehensive care and medication management for transplant patients. Hospitals also play a vital role in monitoring patients for potential side effects of immunosuppressive drugs, ensuring the success of the transplant, and improving patient outcomes.

North America Is Largest Region Owing to High Organ Transplantation Rates and Healthcare Infrastructure

North America is the largest region in the organ transplant immunosuppressant drugs market, owing to its advanced healthcare infrastructure, high organ transplantation rates, and substantial investments in medical research. The United States, in particular, is a global leader in organ transplantation, with a high number of kidney, liver, heart, and lung transplants performed annually. North America’s well-established healthcare system and access to cutting-edge medical treatments drive the demand for immunosuppressant drugs, as transplant centers and hospitals utilize these medications to ensure the success of organ transplants.

The region’s strong pharmaceutical and biotechnology sectors also contribute to the growth of the organ transplant immunosuppressant drugs market, as new treatments and drug formulations are continuously developed and introduced. With ongoing research and innovation, North America is expected to remain the largest regional market for organ transplant immunosuppressant drugs.

Competitive Landscape and Key Players

The organ transplant immunosuppressant drugs market is highly competitive, with several leading pharmaceutical companies dominating the market. Key players include Novartis, Astellas Pharma, Roche, and Bristol-Myers Squibb, all of which offer a range of immunosuppressive drugs for organ transplant patients. These companies are focused on developing new formulations, improving drug efficacy, and reducing side effects associated with long-term immunosuppressive therapy.

The competitive landscape is characterized by a strong emphasis on research and development, with companies striving to improve drug combinations and patient outcomes. Strategic partnerships between pharmaceutical companies, transplant centers, and research institutions are also common in this market, as they work together to develop more effective immunosuppressive therapies. With the growing demand for organ transplants and the continued focus on improving transplant success rates, leading companies are expected to maintain a strong market presence through innovation and strategic collaborations.

Recent Developments:

- Gujarat Narmada Valley Fertilizers & Chemicals (GNFC) has expanded its white coal production facility to cater to the increasing demand for cleaner fuel in India.

- Thermo Fisher Scientific acquired a leading optogenetics tool manufacturer to enhance its capabilities in the genetic research sector.

- Carl Zeiss AG introduced a new imaging system designed for optogenetic research, offering enhanced resolution and data capture capabilities.

- Merck Group launched an optogenetics kit tailored for neuroscience research, enabling advanced cellular manipulation using light.

- Bluebird Bio, Inc. entered into a partnership with a biotech company to integrate optogenetics into their gene therapy development pipeline for neurological diseases.

List of Leading Companies:

- Novartis International AG

- Roche Holding AG

- Pfizer Inc.

- Merck & Co., Inc.

- Astellas Pharma Inc.

- Bristol-Myers Squibb Company

- AbbVie Inc.

- Eli Lilly and Co.

- AstraZeneca PLC

- Sanofi S.A.

- Gilead Sciences, Inc.

- Teva Pharmaceutical Industries Ltd.

- Mallinckrodt Pharmaceuticals

- Zydus Cadila

- Hikma Pharmaceuticals PLC

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 6.2 Billion |

|

Forecasted Value (2030) |

USD 9.5 Billion |

|

CAGR (2025 – 2030) |

7.3% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Global Organ Transplant Immunosuppressant Drugs Market by Drug Class (Calcineurin Inhibitors, mTOR Inhibitors, Antimetabolites, Corticosteroids, Monoclonal Antibodies), by Application (Kidney Transplantation, Liver Transplantation, Heart Transplantation, Lung Transplantation), by End-Use Industry (Hospitals, Organ Transplantation Centers, Pharmaceutical Companies, Research Institutes) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Novartis International AG, Roche Holding AG, Pfizer Inc., Merck & Co., Inc., Astellas Pharma Inc., Bristol-Myers Squibb Company, Eli Lilly and Co., AstraZeneca PLC, Sanofi S.A., Gilead Sciences, Inc., Teva Pharmaceutical Industries Ltd., Mallinckrodt Pharmaceuticals, Hikma Pharmaceuticals PLC |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Organ Transplant Immunosuppressant Drugs Market, by Drug Class (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Calcineurin Inhibitors |

|

4.2. mTOR Inhibitors |

|

4.3. Antimetabolites |

|

4.4. Corticosteroids |

|

4.5. Monoclonal Antibodies |

|

5. Organ Transplant Immunosuppressant Drugs Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Kidney Transplantation |

|

5.2. Liver Transplantation |

|

5.3. Heart Transplantation |

|

5.4. Lung Transplantation |

|

5.5. Others |

|

6. Organ Transplant Immunosuppressant Drugs Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals |

|

6.2. Organ Transplantation Centers |

|

6.3. Pharmaceutical Companies |

|

6.4. Research Institutes |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Organ Transplant Immunosuppressant Drugs Market, by Drug Class |

|

7.2.7. North America Organ Transplant Immunosuppressant Drugs Market, by Application |

|

7.2.8. North America Organ Transplant Immunosuppressant Drugs Market, by End-Use Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Organ Transplant Immunosuppressant Drugs Market, by Drug Class |

|

7.2.9.1.2. US Organ Transplant Immunosuppressant Drugs Market, by Application |

|

7.2.9.1.3. US Organ Transplant Immunosuppressant Drugs Market, by End-Use Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Novartis International AG |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Roche Holding AG |

|

9.3. Pfizer Inc. |

|

9.4. Merck & Co., Inc. |

|

9.5. Astellas Pharma Inc. |

|

9.6. Bristol-Myers Squibb Company |

|

9.7. AbbVie Inc. |

|

9.8. Eli Lilly and Co. |

|

9.9. AstraZeneca PLC |

|

9.10. Sanofi S.A. |

|

9.11. Gilead Sciences, Inc. |

|

9.12. Teva Pharmaceutical Industries Ltd. |

|

9.13. Mallinckrodt Pharmaceuticals |

|

9.14. Zydus Cadila |

|

9.15. Hikma Pharmaceuticals PLC |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Organ Transplant Immunosuppressant Drugs Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Organ Transplant Immunosuppressant Drugs Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Organ Transplant Immunosuppressant Drugs Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA