As per Intent Market Research, the Orchestration Tools Market was valued at USD 5.9 Billion in 2024-e and will surpass USD 14.4 Billion by 2030; growing at a CAGR of 15.9% during 2025-2030.

The orchestration tools market is expanding rapidly, driven by the increasing complexity of business operations and the need for organizations to streamline their processes and improve efficiency. Orchestration tools enable businesses to automate and manage workflows, data processes, infrastructure, and security, ensuring that various systems and applications work in harmony. These tools are pivotal in enhancing productivity, reducing manual interventions, and ensuring smoother business operations. As industries become more digitized and rely on cloud-based solutions, orchestration tools play a key role in optimizing workflows, managing IT infrastructure, and ensuring seamless integration of diverse technologies across business units.

The market is segmented by tool types, deployment modes, organization sizes, and end-user industries, allowing businesses to tailor orchestration solutions according to their specific needs. The rise of cloud adoption, the shift towards DevOps practices, and the increasing demand for data-driven decision-making have accelerated the demand for orchestration tools. These tools are especially critical in industries such as IT & telecom, BFSI, retail, and healthcare, where seamless integration and automation are vital for operational success. As organizations seek to improve their agility, security, and data management, the orchestration tools market is poised for continued growth and innovation.

Cloud Orchestration Tools are Fastest Growing Owing to Increased Cloud Adoption

Among the various types of orchestration tools, cloud orchestration tools are the fastest-growing segment, primarily driven by the growing adoption of cloud computing and the need for businesses to manage complex cloud environments efficiently. Cloud orchestration involves automating the management and coordination of cloud services, enabling businesses to provision resources, scale applications, and manage multiple cloud services seamlessly. This automation of tasks such as resource allocation, load balancing, and data management helps organizations optimize their cloud operations and ensure better performance across cloud platforms.

With the increasing reliance on multi-cloud and hybrid-cloud environments, cloud orchestration tools are becoming indispensable for businesses to manage their cloud infrastructure effectively. These tools enable businesses to automate processes, improve resource utilization, and reduce the operational costs associated with managing complex cloud environments. The demand for cloud orchestration tools is particularly high in industries such as IT & telecom, where cloud computing is fundamental to delivering scalable and agile services. As cloud adoption continues to accelerate, the market for cloud orchestration tools is expected to maintain its rapid growth trajectory.

Large Enterprises are Largest Adopters of Orchestration Tools Owing to Complex Operations

In terms of organization size, large enterprises are the largest adopters of orchestration tools, driven by their need to manage complex and large-scale operations. Large organizations often have a wide range of systems, applications, and workflows across various departments, and orchestration tools are essential to ensure that all these components work together efficiently. The ability to automate processes, reduce manual interventions, and improve operational efficiency is crucial for large enterprises to maintain competitiveness and meet the demands of a dynamic business environment.

Additionally, large enterprises typically have more significant IT infrastructure and are more likely to implement integrated orchestration solutions across different functions, such as IT management, security, and data. These businesses often rely on orchestration tools to manage their complex workflows, maintain security, and ensure that their infrastructure is operating optimally. As the need for automation and streamlined operations grows, large enterprises will continue to drive the demand for orchestration tools across various industries, including IT & telecom, manufacturing, and healthcare.

IT & Telecom Industry is Largest End-User Owing to Need for Automation and Service Delivery Optimization

The IT & telecom industry is the largest end-user of orchestration tools due to its critical need for automation, resource management, and service delivery optimization. IT service providers and telecom companies face the challenge of managing complex networks, infrastructure, and customer demands. Orchestration tools help these companies automate and optimize their service delivery processes, improve network management, and streamline customer support operations. The growing demand for scalable and efficient services, particularly in areas like cloud computing, 5G, and network virtualization, has made orchestration tools a key component of their operations.

Moreover, with the increasing complexity of IT systems, including multi-cloud environments and hybrid networks, orchestration tools enable telecom providers to manage and automate operations seamlessly. These tools help telecom companies improve network efficiency, reduce downtime, and ensure better performance across their infrastructure. As the IT & telecom industry continues to evolve and embrace digital transformation, orchestration tools will remain integral in helping companies meet the growing demands of automation and service delivery.

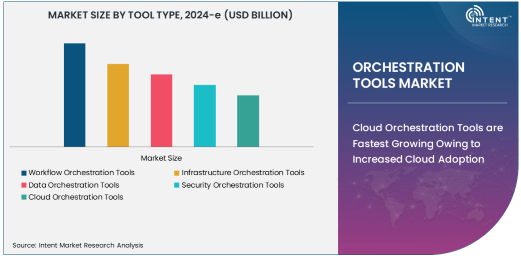

Workflow Orchestration Tools are Largest Application Owing to Central Role in Business Process Automation

In the application segment, workflow orchestration tools are the largest, as they play a central role in automating and managing business processes across organizations. Workflow orchestration tools enable businesses to streamline repetitive tasks, coordinate workflows across departments, and ensure that all tasks are completed on time and in the correct sequence. These tools help businesses eliminate manual errors, improve efficiency, and enhance overall operational effectiveness, making them essential for industries ranging from manufacturing to healthcare.

The demand for workflow orchestration tools is particularly high in sectors like retail, e-commerce, and healthcare, where businesses rely on efficient coordination of various functions such as inventory management, order processing, and patient care. By automating these workflows, organizations can improve their operational agility and responsiveness. As businesses continue to focus on enhancing productivity and minimizing operational bottlenecks, workflow orchestration tools will remain a dominant application in the orchestration tools market.

Asia Pacific is Fastest Growing Region Owing to Digital Transformation and Cloud Adoption

The Asia Pacific region is the fastest-growing market for orchestration tools, driven by rapid digital transformation and the increasing adoption of cloud technologies. Countries like China, India, Japan, and Southeast Asian nations are investing heavily in cloud infrastructure, automation technologies, and digital services, creating a strong demand for orchestration tools. As businesses in these regions look to optimize their operations, reduce costs, and improve service delivery, the adoption of orchestration tools is accelerating.

Additionally, the growing emphasis on automation, particularly in IT & telecom, manufacturing, and retail, is further fueling market growth in the region. The rise of smart cities, IoT applications, and cloud-based services is pushing businesses to adopt orchestration solutions to manage their growing networks and infrastructure. As Asia Pacific continues to experience rapid economic growth and technological advancements, the demand for orchestration tools is expected to remain robust, making the region a key driver of the global market.

Leading Companies and Competitive Landscape

Leading companies in the orchestration tools market include IBM Corporation, Microsoft Corporation, Oracle Corporation, Cisco Systems, and VMware Inc. These companies provide a wide range of orchestration solutions tailored to various industries, with offerings spanning cloud orchestration, workflow automation, infrastructure management, and security orchestration. Their products are designed to help businesses optimize their operations, enhance service delivery, and improve security by integrating multiple systems and applications.

The competitive landscape in the orchestration tools market is marked by the presence of both established players and new entrants. Companies are increasingly focusing on developing cloud-native orchestration solutions and integrating advanced technologies such as AI, machine learning, and automation to differentiate themselves in the market. Additionally, mergers and acquisitions, along with strategic partnerships, are common as companies seek to expand their product portfolios and increase their market share. As the demand for orchestration tools grows, innovation will remain a key factor for success in this highly competitive market.

Recent Developments:

- In December 2024, Microsoft launched an AI-enhanced orchestration platform for hybrid cloud environments.

- In November 2024, VMware introduced an updated orchestration tool for containerized applications.

- In October 2024, Red Hat announced the integration of its Ansible Automation Platform with major cloud providers.

- In September 2024, Google Cloud enhanced its orchestration capabilities with new Kubernetes-native tools.

- In August 2024, AWS released a multi-cloud orchestration solution to improve hybrid cloud deployments.

List of Leading Companies:

- Red Hat, Inc.

- Microsoft Corporation

- VMware, Inc.

- IBM Corporation

- Oracle Corporation

- BMC Software, Inc.

- Chef Software

- ServiceNow

- Cisco Systems, Inc.

- CloudBees, Inc.

- Broadcom Inc. (CA Technologies)

- Google LLC (Google Cloud)

- AWS (Amazon Web Services)

- Dell Technologies

- Puppet, Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 5.9 Billion |

|

Forecasted Value (2030) |

USD 14.4 Billion |

|

CAGR (2025 – 2030) |

15.9% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Orchestration Tools Market by Tool Type (Workflow Orchestration, Infrastructure Orchestration, Data Orchestration, Security Orchestration, Cloud Orchestration), Deployment Mode (On-Premise, Cloud-Based), Organization Size (Small & Medium Enterprises - SMEs, Large Enterprises), End-User Industry (IT & Telecom, BFSI, Retail & E-commerce, Healthcare & Life Sciences, Manufacturing, Government) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Red Hat, Inc., Microsoft Corporation, VMware, Inc., IBM Corporation, Oracle Corporation, BMC Software, Inc., Chef Software, ServiceNow, Cisco Systems, Inc., CloudBees, Inc., Broadcom Inc. (CA Technologies), Google LLC (Google Cloud), AWS (Amazon Web Services), Dell Technologies, Puppet, Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Orchestration Tools Market, by Tool Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Workflow Orchestration Tools |

|

4.2. Infrastructure Orchestration Tools |

|

4.3. Data Orchestration Tools |

|

4.4. Security Orchestration Tools |

|

4.5. Cloud Orchestration Tools |

|

5. Orchestration Tools Market, by Deployment Mode (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. On-Premise |

|

5.2. Cloud-Based |

|

6. Orchestration Tools Market, by Organization Size (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Small & Medium Enterprises (SMEs) |

|

6.2. Large Enterprises |

|

7. Orchestration Tools Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. IT & Telecom |

|

7.2. BFSI |

|

7.3. Retail & E-commerce |

|

7.4. Healthcare & Life Sciences |

|

7.5. Manufacturing |

|

7.6. Government |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Orchestration Tools Market, by Tool Type |

|

8.2.7. North America Orchestration Tools Market, by Deployment Mode |

|

8.2.8. North America Orchestration Tools Market, by Organization Size |

|

8.2.9. North America Orchestration Tools Market, by End-User Industry |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Orchestration Tools Market, by Tool Type |

|

8.2.10.1.2. US Orchestration Tools Market, by Deployment Mode |

|

8.2.10.1.3. US Orchestration Tools Market, by Organization Size |

|

8.2.10.1.4. US Orchestration Tools Market, by End-User Industry |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Red Hat, Inc. |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Microsoft Corporation |

|

10.3. VMware, Inc. |

|

10.4. IBM Corporation |

|

10.5. Oracle Corporation |

|

10.6. BMC Software, Inc. |

|

10.7. Chef Software |

|

10.8. ServiceNow |

|

10.9. Cisco Systems, Inc. |

|

10.10. CloudBees, Inc. |

|

10.11. Broadcom Inc. (CA Technologies) |

|

10.12. Google LLC (Google Cloud) |

|

10.13. AWS (Amazon Web Services) |

|

10.14. Dell Technologies |

|

10.15. Puppet, Inc. |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Orchestration Tools Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Orchestration Tools Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Orchestration Tools Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA